ncbill

Thinks s/he gets paid by the post

Thanks for your input, have learnt from your prior posts.

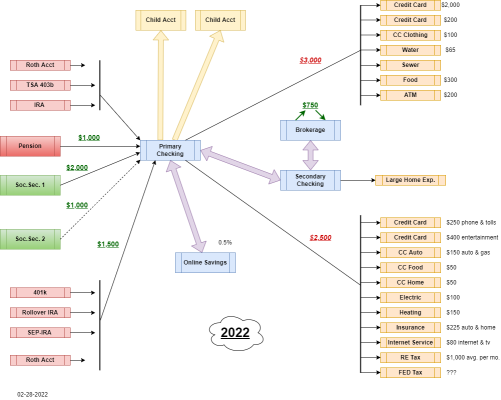

Gifting at present each year -

-$30k from our taxable to our unmarried 29 yr old son (MBA), transfer some to his Vanguard Account & some to him in cash

-$30k to our daughter (She & her husband are MDs) some in cash, but mostly to her kids (our grandkid's) 529 plans.

We paid for our kids education & they did not have any students loan. So far they have not asked us for any money, although they do know we have millions worth in investments. Hopefully they do not start expecting or depending on us. We will leave the kitty to them when we pass

Making baby steps from the Fidelity Donor Advised Fund -

1)Last yr to a Scholarship at the State Uni., our kids graduated from

2)Started a pledged Endowed Scholarship at a local Community College

3)Local Temple, few other causes here & education of poor (501c) in India.

Will look up Perkins "Die with Zero",

Thankyou

IIRC, annual gift limit has increased to $16k/person for 2022.