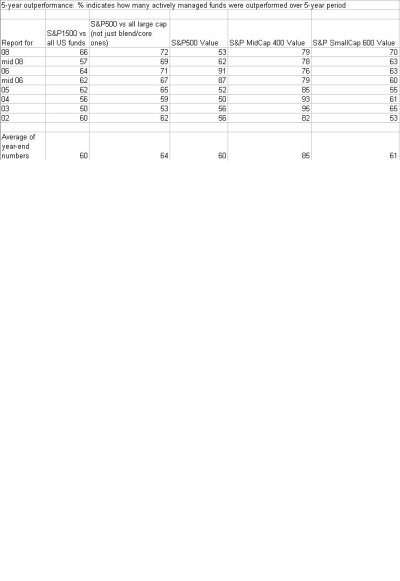

Second, you definitely can not do comparisons now based on stats from before you invested. So only comparison periods of less than three years are relevant in this case.

Why not? Fund performance does not depend on whether I have the money in it or not.

I'll rephrase. You can not do comparisons now based on stats from before you invested, unless your comparisons also include all the other funds you did not invest in. We already know if you include all the funds, index funds will beat the majority, but by no means all of the funds in existence.

Let me try some examples to hopefully make this clearer. Suppose (totally made up numbers), that $100 invested in fund A had balances over the last 10 years of:

$100,$110,$121,$132,$143,$155,$170,$190,$260,$150.

Suppose fund B had values of

$100,$105,$110,$115,$119,$110,$110,$130,$135,$140

Now suppose based on that wonderful historic record, three years ago you invested in fund A at $170, instead of in fund B at $110. Today you evaluate your investments, and decide that because fund A still has the better 10 year performance record, you were a genius to invest in fund A instead of fund B. Even though fund A lost you money, and fund B would have made you money! Since A still has the better ten year record, you say I know the research says B should be better over the long term, but I picked A which has still beat B over the long term, so I'm sticking with A.

Does that example make the problem clearer?

Using the classic coin-toss as the basis for an example, suppose you have a large room full of people tossing coins, and a bunch of machines also tossing coins. After seven tosses you arrive and are offered betting choices. You can bet your money splitting it between any of the coin tossers. You will win or lose based on how many heads they toss. If you bet money on a tosser caught cheating you lose all your bet. You will also need to pay each tosser part of your bet. Thankfully the tossers must disclose how much you will need to pay. You notice all the machines charge you less than any of the humans, usually something around 0.2% of your bet. The humans have lots of different fees that don't seem to make much sense, but are always higher than the machine tossers charge. A guy named Vanguard seems to be the cheapest human asking around 0.5%. There are also some advisers around the room who have been watching the tosses closely, and say for an additional fee they will invest your money for you with only those tossers with tossing skill. You notice that some of those advisers charge a lower or even no fee for this service, but seem to only pick tossers who charge the highest fees, and share some of that fee with the adviser.

Happily there are terminals in the room that allow you to not just place bets, but also to see the toss history and fees charged by every tosser. So you decide to ignore the advisers.

You have read that the smart way to invest is to just bet on the machine tossers, but lots of the humans have perfect tossing records, while the machines are closer to average. You decide to select only those humans who have so far tossed perfect heads, and who charge below average fees for a human. You split your bet between a number of these humans. After three tosses, you compare the 10 toss history of your choices, all of whom had 7 heads when you picked them, with the 10 toss history of the machines, most of which had already tossed some tails before you entered the room. Your choices have definitely not kept up their perfect tossing records since you placed your bets, but they still have better 10 toss histories than most of the machines, even if they do charge higher fees. So you think you will stick with them, except for that tosser who was replaced by a substitute tosser.

While you are waiting for the next toss, you post about your betting experience here. I try to convince you that on an after fees basis, I think you would do better to bet on the machines.