|

|

02-07-2015, 08:36 PM

02-07-2015, 08:36 PM

|

#21

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: May 2009

Posts: 9,343

|

My allocation currently is 40% investment grade preferred stocks which yield between 6-7%, 40% index funds, and 20% cash CD and IBonds. If rates go up and drop the preferred's I will buy more with my cash. I still contribute monthly to my investments as I do not have enough assets to live comfortably on if my pension system blew up.

Sent from my iPad using Tapatalk

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

02-08-2015, 04:10 AM

|

#22

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,193

|

Quote: Quote:

Originally Posted by audreyh1

Kitces et. al showed that starting retirement with 30% stocks but thereafter increasing the stock % gradually over decades until it reaches 60% or 70% can improve portfolio survival, especially in the first 15 years when you mostly spend down the fixed income and let the stocks ride. But leaving it at 30% is not as good for portfolio survival in face of inflation, as a 50/50 approach +/- 10%. This Kitces approach is called the rising glide path.

|

same here , we reduced down to about 38% equities and will increase 2 % a year going forward. with markets at new highs just as i am retiring the odds of a downturn just as i start retirement are pretty good.

|

|

|

|

|

02-08-2015, 04:39 AM

|

#23

|

|

Recycles dryer sheets

Join Date: Mar 2010

Location: Poway, CA

Posts: 441

|

In 2008 after the recession/ downturn, we ran Matlab simulations to try to understand how we could have done better as we lost three or four hundred thousand dollars in that crash. I concluded that gradually getting down to 40% stocks and the rest bonds as ER approaches was a good strategy to avoid heavy losses like we experienced. We used a Vanguard total stock fund and a Vanguard total bond fund in the simulations and included reinvesting the dividends. I also allowed for the possibility of investing a few % more in stocks during downturns of 10 - 15% or more which I did twice in the last 6 years. I expect this recipe to provide much less volatility the a 60% stock approach would, but have a return of only about 5.8%. This return is acceptable to us and is the price we pay for reduced volatility. We plan to use 3 - 4% safe withdrawal rate until ss then cut back to 2 - 3%. We're 57 and hope to ER in two years.

Sent from my Nexus 4 using Early Retirement Forum mobile app

|

|

|

|

|

02-08-2015, 06:07 AM

|

#24

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,145

|

Quote:

Originally Posted by ejman

I've kept my AA at a nominal 50/50 (10% band) since ER'd 12 years ago (currently 64). Although re balancing was an infrequent occurrence with the wide band I use I'm contemplating letting equities "ride" since the equity funds are primarily in my taxable account and I don't want to create taxable events as my rebalancing seems to be usually in the direction of selling equities to buy bonds.

If historical patterns hold the equities % would naturally increase over the years but the research you mentioned gives a measure of comfort in allowing this to happen.

|

In their study, if you started with a higher equity allocation like 50/50 or 60/40 there was no increased survival benefit to the glide path approach. It wasn't worse. Just didn't make any difference. The payoff is when a retiree starts quite low.

__________________

Retired since summer 1999.

|

|

|

|

|

02-08-2015, 06:12 AM

|

#25

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,193

|

with one qualification .

the difference is if the retirement kicks off badly the rising glide path has performed better than going in at your full allocation.

once you have a good upturn early on you are good to go with a full allocation. the rising glide path is really only to protect you early on if you feel you need it or if you are very conservatively invested. the more conservative you are the greater the rising glide path helps. .

being i am retiring now and earning estimates have been lowered by 36% for this year there is a good chance i will be caught in a downturn if that turns out to be the case.

|

|

|

|

|

02-08-2015, 06:23 AM

|

#26

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2012

Location: Texas

Posts: 3,024

|

Quote:

Originally Posted by photoguy

I can't see Ferri advocating 30s/70b for an early retiree....

|

I don't think Ferri is making a case for 30/70 as a definitive final answer for all retirees. He says it should be a "starting point" for a discussion about AA for the average retiree; just as 60/40 should be the starting point for the average accumulator. His last paragraph says that adjustments up or down from those starting points is "...fully understandable and acceptable after a thorough assessment of safety needs, income, longevity and estate planning considerations in retirement."

Interestingly, by the time I was a year or two from retirement, I had shifted to 30/70 under the same rationale Ferri mentions in the article:

Quote:

|

There is no economic reason for a person to take more investment risk than necessary once theyve accumulated enough money for retirement. The focus should be on the minimum amount of risk needed to achieve an income required in retirement.

|

However, after reading extensively on the subject (including this forum), and experimenting with various inflation and longevity assumptions in my retirement spreadsheets, I concluded that, as a 52 year-old retiree, I needed considerably more equity. In addition, we have some significant unknowns about LTC, both for my in-laws near term and ourselves longer term. It's not unreasonable to conjure up a worst-case scenario (inflation, longevity, LTC) where 30/70 failed miserably.

And as I said earlier in the thread, we have a substantial portion of expenses covered by two pensions (one non-COLA) and rental income. I generally consider the real estate as part of my equity allocation, although it has characteristics of fixed income as well. Either way, counting the PV of pensions as bond-equivalents results in ~50/50 overall, excluding cash reserves. I'm very comfortable with that balance of return and volatility for this stage of ER, and considering the circumstances, I don't think Ferri would object either.

__________________

Retired at 52 in July 2013. On to better things...

AA: 85/15 WR: 2.7% SI: 2 pensions, SS later

|

|

|

|

|

02-08-2015, 06:25 AM

|

#27

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,145

|

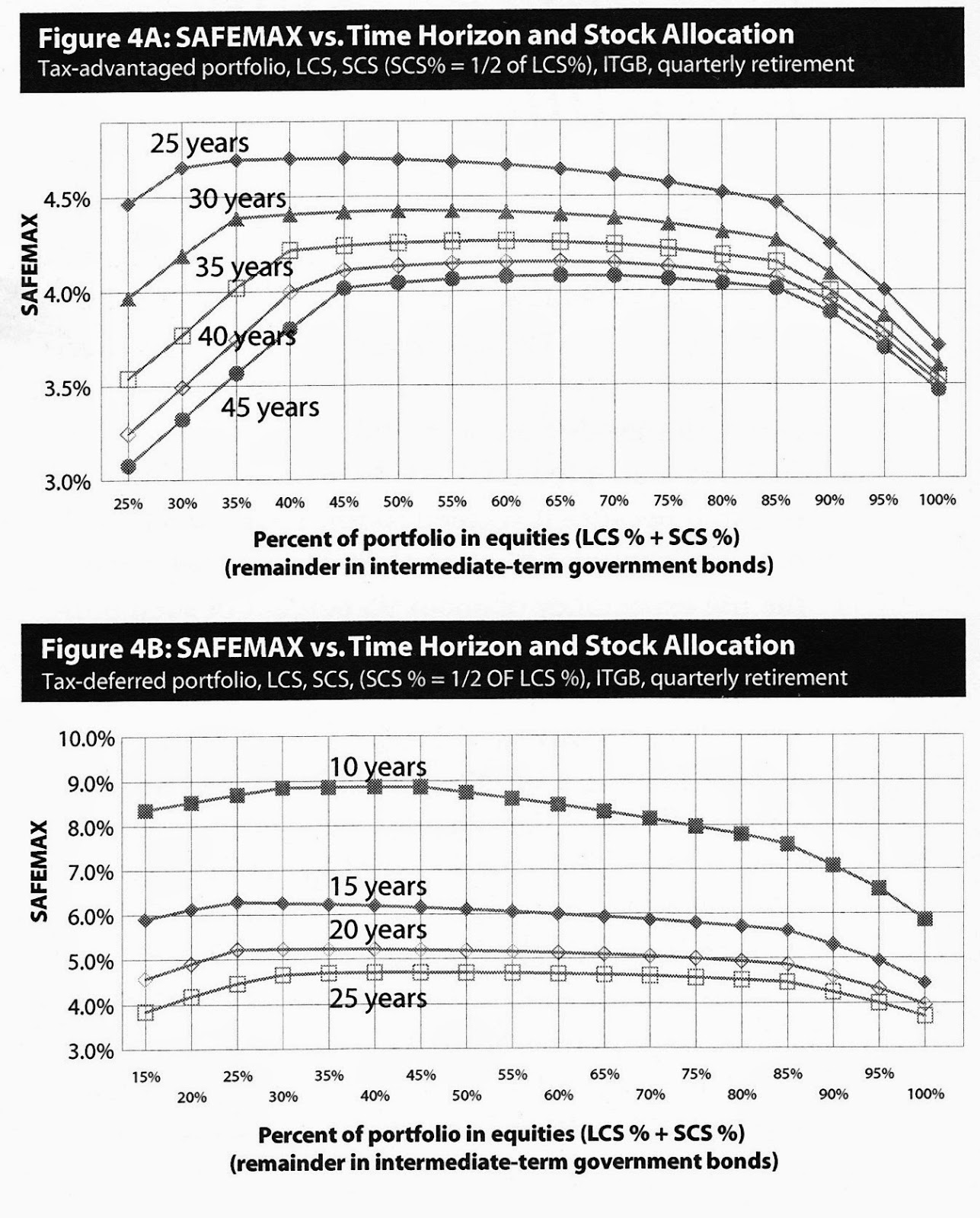

For those looking at allocations to stick with in retirement (not the rising glide path case), you should be aware of graphs like the first one below that show when equity allocation drops below 45% what you can safely withdraw over a long period drops too.

This was in one of Bengen's books according to the referring article.

__________________

Retired since summer 1999.

|

|

|

|

|

02-08-2015, 06:31 AM

|

#28

|

|

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Join Date: Jun 2002

Location: Texas: No Country for Old Men

Posts: 50,021

|

^ What audrey1 said.

Here's a chart from FIRECalc illustrating the same allocation information. Go lower than 40 - 45% in equities and the 30 year success rate drops off significantly.

__________________

Numbers is hard

|

|

|

|

|

02-08-2015, 06:33 AM

|

#29

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,193

|

quote:

There is no economic reason for a person to take more investment risk than necessary once they’ve accumulated enough money for retirement. The focus should be on the minimum amount of risk needed to achieve an income required in retirement.

--------------------------------------------------------------------------------------

i am a big believer in that quote . many have pensions and for them the pay check never really stops.

they are generally in a different group when talking about the above quote.

they are still in their accumulation stage pretty much if all they need are some slight withdrawals or the withdrawals are really fun money.

for many they are not investing for themselves and their homemade income stream , many are really investing for heirs and not so much themselves and their income.

my goal now is not to grow poorer and i want more downside protection than upside potential.

|

|

|

|

|

02-08-2015, 06:34 AM

|

#30

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,193

|

Quote:

Originally Posted by REWahoo

^ What audrey1 said.

Here's a chart from FIRECalc illustrating the same allocation information. Go lower than 40 - 45% in equities and the 30 year success rate drops off significantly.

|

the updated trinity combined with monte carlo simulations had concluded anything above 35% would be pretty successful especially at 3.50%.

30 years, withdrawal 4% inflation-adjusted (no fees):

Considering all allocations, the best success probability is 87%.

That 87% success probability is achieved at any allocation that is at least 60% stocks.

An 86% success probability is achieved with stocks allocation 40% or 50%.

Reduce withdrawal to 3.5% inflation-adjusted (no fees):

Considering all allocations, the best success probability is 92%.

That 92% success probability is achieved at any allocation from 20% stocks to 80% stocks.

Reduce withdrawal to 3% inflation-adjusted (no fees):

Considering all allocations, the best success probability is 98%.

That 98% success probability is achieved only with 0% stocks.

A 97% success probability is achieved with any allocation from 20% stocks to 80% stocks.

|

|

|

|

|

02-08-2015, 06:45 AM

|

#31

|

|

Administrator

Join Date: Jan 2008

Location: Chicagoland

Posts: 40,724

|

I find it surprising Mr. Ferri did not mention withdrawal rate or portfolio survivability in an essay about asset allocation for retirees. Perhaps he expects returns for the equity portion will be high.

|

|

|

|

02-08-2015, 07:04 AM

|

#32

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,193

|

the origonal studies looked at 1926 to 1996. that was only 41 retirement time frames.

as of 2009 we now have 55 retirement time frames and looks at retirement dates from 1926 to 1980.

surprisingly there are still only 2 failure periods , 1965 and 1966.

the flaw is that the really bad years for the markets showed up in the later years of the retirement time frame of the more recent look.. that only has a very small effect at that point.

a newer retire reting more recently like the y2k retiree would have those bad return years early on creating very different results when their numbers are finally in.

|

|

|

|

|

02-08-2015, 10:30 AM

|

#33

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2007

Posts: 1,214

|

Quote:

|

There is no economic reason for a person to take more investment risk than necessary once theyve accumulated enough money for retirement. The focus should be on the minimum amount of risk needed to achieve an income required in retirement.

|

There are 2 big problems with this statement.

The first is that he implicitly equates volatility to risk.

It isn't. Volatility is not risk.

The second is that he completely ignores inflation risk. Well, a risk is still a risk even if you ignore it.

On average, stocks will float up with inflation. But bonds do not.

You will get the par amount when they mature, but the buying power will be lower. And if you sell them before they mature, then the value will float up and down just like stock prices go up and down -- so what have you accomplished?

|

|

|

|

|

02-08-2015, 02:48 PM

|

#34

|

|

Recycles dryer sheets

Join Date: Jan 2013

Posts: 162

|

While many on this forum have had the discipline to ride out significant equity fluctations, lots of people outside of this forum have not. Mr. Ferri is just presenting that a 30/70 portfolio should produce a solid return that is less likely to result in panic selling, so it's something to consider. If one can enjoy life at those spending levels, than why not avoid possible stomach churning volatility? It's similiar to Bernstein's advice that if you've already won the game, why keep playing?

|

|

|

|

|

02-08-2015, 03:05 PM

|

#35

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,145

|

Quote:

Originally Posted by enjoyinglife102

While many on this forum have had the discipline to ride out significant equity fluctations, lots of people outside of this forum have not. Mr. Ferri is just presenting that a 30/70 portfolio should produce a solid return that is less likely to result in panic selling, so it's something to consider. If one can enjoy life at those spending levels, than why not avoid possible stomach churning volatility? It's similiar to Bernstein's advice that if you've already won the game, why keep playing?

|

Ultimately the long retirement issue is inflation.

If you can amass a large enough portfolio that your withdrawal is small enough such that your portfolio survives. But this can requires a larger portfolio so it may mean working more years to reach that goal. That might be a significant trade off. Looking at the above chart for a 40 year survival you would need a 14% larger portfolio if you wanted 30% equity allocation instead of 40%.

Otherwise you're just ignoring the long-term risk to reduce the short-term volatility.

Bernsteins "won the game" approach also ignores the effects of inflation long-term. In his case, he has the "won the game" piece in cash and short-term fixed income for 25x needs. And only then can you put amounts above that in equities. Well a 100% bond portfolio only supports a 3.33% withdrawal rate for 30 years compared to a more balanced approach supporting 4.25% or better. That requires a larger portfolio to support the less volatile approach and enjoy the same standard of living - 28% larger. And the longer the survival time frame, the worse the divergence. It may mean the difference between retiring early and not.

If someone has 20 or 25 years or less to be retired, I don't see a problem with sticking with 30% equities. But early retirees need portfolios to last 35 to 40 years or more.

__________________

Retired since summer 1999.

|

|

|

|

|

02-08-2015, 03:31 PM

|

#36

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,193

|

Quote:

Originally Posted by rayvt

There are 2 big problems with this statement.

The first is that he implicitly equates volatility to risk.

It isn't. Volatility is not risk.

The second is that he completely ignores inflation risk. Well, a risk is still a risk even if you ignore it.

On average, stocks will float up with inflation. But bonds do not.

You will get the par amount when they mature, but the buying power will be lower. And if you sell them before they mature, then the value will float up and down just like stock prices go up and down -- so what have you accomplished?

|

the problem with risk vs volatility is volatility is only volatility until you run out of time. then it becomes risk.

if we have not recovered by the time you need to refill spending money then the risk of selling at a loss becomes very real.

if anyone ever told me back in 2000 that the balance on my equities portion would barely be up 1.77% a year real return on average 15 years later with dividends reinvested i would have thought they were nuts.

|

|

|

|

|

02-08-2015, 03:37 PM

|

#37

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,193

|

Quote:

Originally Posted by audreyh1

Ultimately the long retirement issue is inflation.

If you can amass a large enough portfolio that your withdrawal is small enough such that your portfolio survives. But this can requires a larger portfolio so it may mean working more years to reach that goal. That might be a significant trade off. Looking at the above chart for a 40 year survival you would need a 14% larger portfolio if you wanted 30% equity allocation instead of 40%.

Otherwise you're just ignoring the long-term risk to reduce the short-term volatility.

Bernsteins "won the game" approach also ignores the effects of inflation long-term. In his case, he has the "won the game" piece in cash and short-term fixed income for 25x needs. And only then can you put amounts above that in equities. Well a 100% bond portfolio only supports a 3.33% withdrawal rate for 30 years compared to a more balanced approach supporting 4.25% or better. That requires a larger portfolio to support the less volatile approach and enjoy the same standard of living - 28% larger. And the longer the survival time frame, the worse the divergence. It may mean the difference between retiring early and not.

If someone has 20 or 25 years or less to be retired, I don't see a problem with sticking with 30% equities. But early retirees need portfolios to last 35 to 40 years or more.

|

more and more studies are showing retirees need a whole lot less inflation adjusting than we think or are told.

the drop off in spending from 70 to 80 is so large that what you stop doing and buying more than offsets any inflation increases on what you continue to spend on..

we pick up again after 80- because of healthcare costs and gifting but over all inflation adjusting is no where near what we predict.

|

|

|

|

|

02-08-2015, 04:41 PM

|

#38

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: May 2004

Location: SW Ohio

Posts: 14,404

|

Yes, now that Mr Ferri has been advising clients for awhile, it's possible he has gotten the same "bug" that afflicted Dr Bernstein: They know what the math and the historical records say, but they have also seen how their clients actually behaved. So, perhaps they are giving advice that matches that behavior, not what would (theoretically) be best.

I'd prefer the advice to be free of embedded behavioral considerations, instead put those in the "notes, warnings, and cautions" that go along with the numbers.

A cynic would say that Dr Bernstein and Mr Ferri are just trying to minimize adverse reactions from their clients, thereby putting their own "comfort" ahead of objectivity. And, as a bonus, recommending that clients invest more conservatively means they'll have lower expected returns and may need to save more. Mr Ferri is compensated, at least in part, according to the size of his clients portfolios.

Quote:

Originally Posted by mathjak107

more and more studies are showing retirees need a whole lot less inflation adjusting than we think or are told.

|

A thousand people = a thousand scenarios. I can do a better job of estimating how I might want to live when I'm 75 than if I just use the "averages."

|

|

|

|

|

02-08-2015, 04:46 PM

|

#39

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2009

Posts: 1,578

|

Quote:

Originally Posted by samclem

Yes, now that Mr Ferri has been advising clients for awhile, it's possible he has gotten the same "bug" that afflicted Dr Bernstein: They know what the math and the historical records say, but they have also seen how their clients actually behaved. So, perhaps they are giving advice that matches that behavior, not what would (theoretically) be best.

I'd prefer the advice to be free of embedded behavioral considerations, instead put those in the "notes, warnings, and cautions" that go along with the numbers.

A cynic would say that Dr Bernstein and Mr Ferri are just trying to minimize adverse reactions from their clients, thereby putting their own "comfort" ahead of objectivity. And, as a bonus, recommending that clients invest more conservatively means they'll have lower expected returns and may need to save more. Mr Ferri is compensated, at least in part, according to the size of his clients portfolios. |

I thought if that too, but then I thought that a higher stock/bond ratio would be in the best interest of the advisor since the portfolio should grow more so the AUM would be more with time. Also some portfolio managers do charge a different fee (less) for the bond portion than the stock portion.

Sent from my iPad using Early Retirement Forum

|

|

|

|

56 year old early retiree from San Diego

|

04-23-2015, 10:30 AM

|

#40

|

|

Confused about dryer sheets

Join Date: Mar 2014

Posts: 1

|

56 year old early retiree from San Diego

Hi,

I'm interested in hearing feedback on the analyses shown below (see link to entire article, along with excerpt). As a 56 year old early retiree currently invested 40 stocks / 40% bonds / 20% cash/CDs (to allow breathing room for fluctuations in markets and possible investment in additional rental property), I'm wondering if going even more conservative (to 20 - 30% stock) for the first 5 years is a prudent decision. Thoughts?

Asset Allocation for Early Retirees | Hull Financial Planning

I created a market and inflation simulation to see if this couple could make it to age 95 without running out of money. I used historical market returns for stocks, ranging from an annual loss of 44.2% to an annual gain of 56.8% and a median return of 10.5%, and for corporate bonds, ranging from a minimum annual gain of 2.5% to a maximum annual gain of 15.2% with a median gain of 5.2%, to determine this couples returns over time. Each year, the simulation picked a random return for stocks and bonds as well as choosing a random amount inflation, ranging from 10.5% deflation to 18% inflation with a median inflation of 2.8%.

I ran the simulation 10,000 times to see how often our couple had money at age 95.

They had a positive net worth at age 95 89.4% of the time. 50% of the time, they had more than $32.5 million, and 50% of the time, they had less than that amount.

When I construct model scenarios, I usually like to aim for a 90% or higher success rate. This is right on the borderline, but if this couple was a client of mine, Id give them the go-ahead with a few warning signs to look out for.

However, recent research by Dr. Wade Pfau, CFA shows that youre most vulnerable to poor market performance in the first few years of retirement. His research was limited to 30 years of earning income and 30 years of retirement, but in that research, he showed that returns in the first year of retirement explained more than 14% of the final outcome for those retirees. Since the risk is mainly poor market performance in those first few years of retirement bad years compounded with withdrawals when the total amount of money that the retirees have is expected to be at its lowest I decided to tweak the strategy to determine if I could improve on this couples outcome.

Instead of using the 110 age asset allocation strategy that would lead to the couple being invested 70% in stocks the first year of retirement, I had them only 20% invested in stocks and 80% invested in corporate bonds for the first five years of their retirement. The results?

This time, they had money left over 93.4% of the time, and their median net worth was $30.6 million. A shift lower by about $2 million to get well into the safety zone is a tradeoff that Id be willing to make.

If 5 years is good, then 10 years should be better, right?

Yes and no.

The couple had money left over 94.6% of the time a much smaller increase in safety. They also had a median net worth of $28.4 million. They paid more for a smaller increase in the cushion.

This makes sense intuitively, as, aside from investing completely in annuities, its nearly impossible to gain complete safety when investing in the market. Additionally, the longer that the couple is so heavily invested in bonds, the more likely it is that inflation could catch them.

The counterintuitive approach that Dr. Pfau advocates for the first few years of retirement for people in their sixties seems to hold true for early retirees as well: shift into more conservative investments for a few years and then shift back into more aggressive investing. Theres a balance in asset allocation in retirement between being too conservative and having your portfolio decimated by inflation and being too aggressive and having unfortunate downturns in the market just as you retire destroy the value of your portfolio. Based on my analysis, portfolio protection in the first few years of early retirement seems to be a prudent approach in improving the chances of having your money outlast you.

Is this surprising information? What do you think? If you go conservative early in retirement, will you have the fortitude to dial the risk back up in a few years? Lets talk about it in the comments below!

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode