Gone4Good

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Sep 9, 2005

- Messages

- 5,381

I doubt that it adds even 1% to the number... but since this is a WAG... I could be wrong...

It's easy to make things up that corroborate our existing opinions. It's harder (but not much) to actually look up the data to see how our opinions stand up against reality.

From 2008 to 2010 "Human Resource" spending increased form 13% of GDP to 17% of GDP, accounting for nearly all of the increase in spending. That includes a $250B increase (1.7% of GDP) for "income security" payments alone.

Do we want to control cost or contain it and slow it's rate of growth? I think the latter. Health care reform provides a foundation to enable that by reducing the need for cost shifting and enabling IPAB to manage reimbursements, among other measures. It is new so there can't be a precedent.WHEN was the LAST time a govt program CONTROLLED costs? There is no precedent that ObamaCare will control costs, take a look at Medcaid/Medciare and SS for examples...........

The same corollary can be made for the income side... we have lower income because of the crisis... and when the one get 'fixed' the other gets 'fixed'.... problem is that the spending does not go down to 'pre Obama' levels... but income does go up to the previous amount...

The fiscal commission's weakest recommendations are in health care, but that is a reflection of the complexity and magnitude of the challenge and is not a shortcoming of the commission.

MichaelB;999519 said:Currently there is only one serious initiative to contain healthcare costs which is the legislation passed last year.

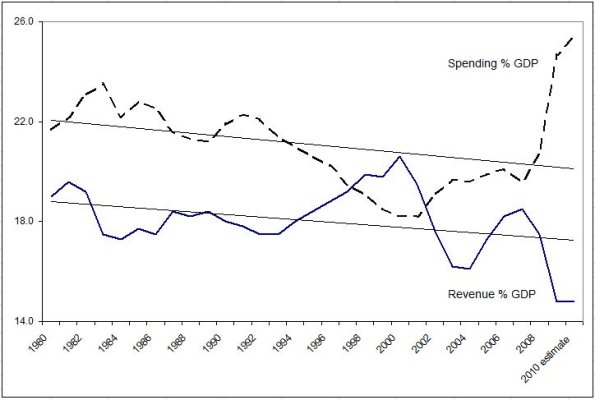

Yup. In recent years federal revenue collapsed because of the recession. But you may also notice that even at the peak of the housing bubble in 2007 revenues were far below those of the Clinton era. So much for "dynamic analysis" that always suggests tax cuts pay for themselves.

With respect to future spending, you'll find that the majority of increased future spending is coming from Social Security and Medicare. Curtailing and paying for their growth is mostly what the deficit commission is about.

Agreed that SS and Medicare are the big boogeymen... but I would also add Defense in there... we need to get it down to 15% or less of the budget... heck, even 10% would be great and also keep us as the biggest spender of defense in the world...

I did not agree with the Bush tax cuts... and to tell the truth I would not vote to keep them... I think there would be pain to a lot of people during a downturn, but we need to start doing something now...

You must have a pretty big mortgage to be savings $600 per month in taxes... heck, my mortgage payment is not much more than that...

A question that I would have is why should the rest of the taxpayers subsidize your big house and your kidsI am not trying to single you out specifically, but that is what is happening with these deductions and credits.

Agreed. But too often it depends on what state and Congressional district fighter planes are built in or where military bases are located.Our defense budget should be based on actual needs (current) and perceived threats (future).

It already is! "Actual needs" (of important contributors) and "perceived threats" (to re-election of various lawmakers)Our defense budget should be based on actual needs (current) and perceived threats (future).

Our defense budget should be based on actual needs (current) and perceived threats (future).

It already is! "Actual needs" (of important contributors) and "perceived threats" (to re-election of various lawmakers)

Agreed but it should be PAID FOR (not borrowed).

If the threats are important and serious enough to defend against then it's important enough to ask the citizens to pay for their defense.

WHEN was the LAST time a govt program CONTROLLED costs? There is no precedent that ObamaCare will control costs, take a look at Medcaid/Medciare and SS for examples...........

You must have a pretty big mortgage to be savings $600 per month in taxes... heck, my mortgage payment is not much more than that...

A question that I would have is why should the rest of the taxpayers subsidize your big house and your kids

I would agree that the mortgage interest deduction can't be immediately 100% repealed because of the impact it would have on the housing market. This is also a concern with the "fair tax" or national sales tax (or VAT) that some are floating -- it also eliminates the mortgage interest deduction 100% in one fell swoop and could really tank the housing market at a time when it's already searching for bottom.That tax cut would make whatever mortgage crisis we have now 10X worse.

Won't the "Death Panels" save us money by pulling the plug on grandma?

Won't the "Death Panels" save us money by pulling the plug on grandma?

I'm sure any changes would be phased in, so you'd retain the taxpayer subsidy of your mortgage interest for a period of years, probably a decade or more. But, there's no doubt this would depress home prices for expensive houses and for homes in vacation areas (due to the targeting of deductions for second homes).My point was without that extra $600, our house would become about 40-50% of net pay, which is too tight IMO- we would be better off (quality of life) by walking away and renting that reducing savings or some other savings technique if the tax break was removed. That tax cut would make whatever mortgage crisis we have now 10X worse.

I would agree that the mortgage interest deduction can't be immediately 100% repealed because of the impact it would have on the housing market. This is also a concern with the "fair tax" or national sales tax (or VAT) that some are floating -- it also eliminates the mortgage interest deduction 100% in one fell swoop and could really tank the housing market at a time when it's already searching for bottom.

However, I see no reason why you can't (a) grandfather the deduction for mortgages that are already in place AND (b) reduce the deduction by (say) 5-10% a year for 10-20 years for all new mortgages in that time frame. That would allow an orderly unwinding of the deduction so it wouldn't have an immediate and devastating impact on home values.

That tax cut would make whatever mortgage crisis we have now 10X worse.