I’m surprised no one mentioned that the general 60/40 or 50/50 AA has always been mentioned as the proven method to moderate total value and loss of shares in a bear market. Sales are of bonds during that time, which are less affected or grow during that period, allowing purchase of the depressed equities during the downtown or as the source of income from sale. Sale of equities resumes when the market recovers. ....

Very nice post, let me expand on a few small points...

I think bonds weren't mentioned much because this was a debate about relative performance of high-div stocks versus the broader market. I did a few of those charts with a 50-50 AA, and it didn't really change the story, both sides were affected about the same, so I didn't bother to maybe 'muddy the waters'.

But I agree totally, bonds will be there to sell on a downturn, stocks will be preserved.

...I can see the allure of Divs for income for anyone that has less stomach for volatility. The generally predicted income allows less monitoring of total portfolio value and any decision making, at a cost of lower total value growth and the subsequent loss of income through the sales of that growth. Most people are not comfortable making the decisions of what to sell and what to keep. While ERD sees it as marginally more effort, many see as monumentally more effort. ...

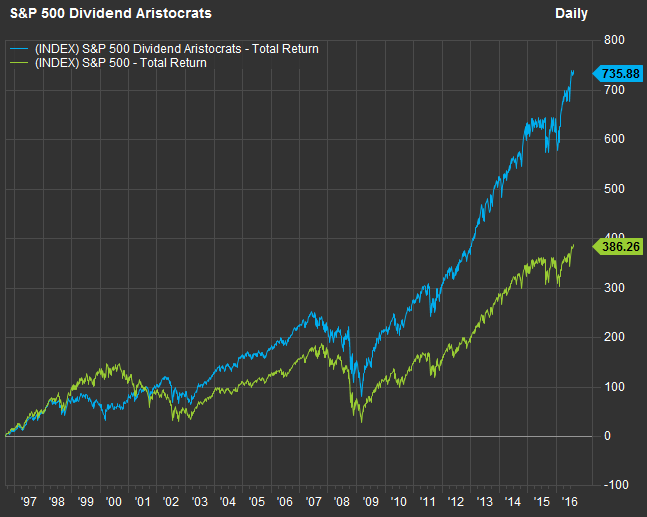

Except the charts we've posted do not show that the high-divs have significantly less volatility.

True, what I describe as marginally more effort (a once-per-year sale decision), some may see as a big deal. But I think that is a very small number of people, and there are alternatives. And it also seems that most of the pro-div people here are selecting individual stocks, monitoring some parameters and selling and buying based on the outlook for future div flow. That must be far more work than an annual sale based on desired withdraw minus div withdraws.

... I know that I have a hard time grasping that the economy and associated Stock Market bears any relevance in comparison from 1900 to 1980 and then from 1990 to present. The information Age has changed that paradigm forever.

While the future may well be different from the past, I see no reason to assume any one approach would be better than another in this unknown future. While true, it doesn't seem relevant to an analysis of div-payers versus broad market.

Bruce,

Some have more time than others to argue the finer points of dividend investing. And it's pretty much a dogma fight, IMO. ...

I honestly don't want to belabor this, but I just can't let that comment stand. The definition of dogma is to accept/defend something in the absence of evidence, or when the evidence is contrary to the belief. Those of us saying there isn't any big advantage to div-payers have presented evidence. The only evidence we have from the div-payer crowd is with a self-selected group of stocks, and that isn't meaningful unless there is some objective, rule-based process for selecting those stocks - one that can be duplicated by an investor w/o too much effort. So WADR, it isn't a "dogma fight", it is dogma on one side, evidence on the other.

Time to review some of the OP (with emphasis):

I've read several thread comments about investing in stocks that provide consistent dividends. The commenters often mention withdrawing the dividend payouts as an annual income stream.

These comments usually involve listing some of the best dividend paying stocks.

I prefer to avoid purchasing individual stocks. Are there mutual funds that focus on dividend paying stocks? .....

- As long as I'm bringing this topic up, is this a good idea?

Well, the charts say that the div-paying funds/ETFs don't act much different from a broad-index fund. So probably no big deal to do it or not do it, but I don't think I could label it a "good idea", just an alternative.

edit/add: I see the OP has not posted since this question. I wonder if they got anything from this?

-ERD50

")