gcgang

Thinks s/he gets paid by the post

- Joined

- Sep 16, 2012

- Messages

- 1,571

Asset Allocation Website

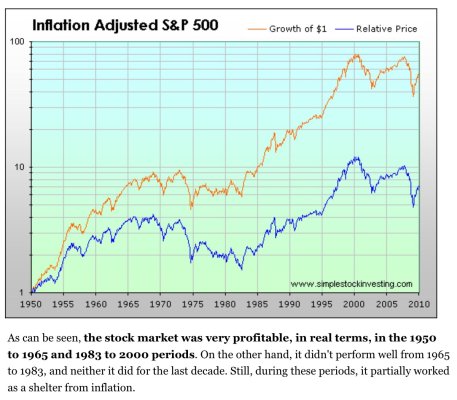

Above is a link to Research Affiliates (Rob Arnott) outlook for asset class returns for the next decade, and it ain't pretty. Excep for EM stuff, looking at pretty close to 0% real returns.

You could dismiss this as discredited market timing, but that's not what they're doing. Like Gross' New Normal, GMOs Asset Class expected returns, all of these look at where we are now - Now being ultra low interest rates and high equity valuations.

For example, historical bond returns have been around 5%. But you can correlate historical ten year bond returns with what the 10 year rate was at the inception of the 10 year period. Today 10 year TNote is what, about 1.5%?

While historical things like Monte Carlo or Firecalc are meant to stress test our situation, none really use today's valuations as a starting point. US markets really don't have much history that's helpful. Maybe Japan of the last 25 years would be a better comparison.

Hopefully they are really not after me, I'm just paranoid.

Above is a link to Research Affiliates (Rob Arnott) outlook for asset class returns for the next decade, and it ain't pretty. Excep for EM stuff, looking at pretty close to 0% real returns.

You could dismiss this as discredited market timing, but that's not what they're doing. Like Gross' New Normal, GMOs Asset Class expected returns, all of these look at where we are now - Now being ultra low interest rates and high equity valuations.

For example, historical bond returns have been around 5%. But you can correlate historical ten year bond returns with what the 10 year rate was at the inception of the 10 year period. Today 10 year TNote is what, about 1.5%?

While historical things like Monte Carlo or Firecalc are meant to stress test our situation, none really use today's valuations as a starting point. US markets really don't have much history that's helpful. Maybe Japan of the last 25 years would be a better comparison.

Hopefully they are really not after me, I'm just paranoid.

Last edited: