lawman

Thinks s/he gets paid by the post

Thanks guys...I have work to do...

Does a Roth conversion open a new Roth IRA or can I just add to my old Roth?

So just to be clear, withdrawals from a Roth IRA does NOT count towards IRMAA penalty...Correct?

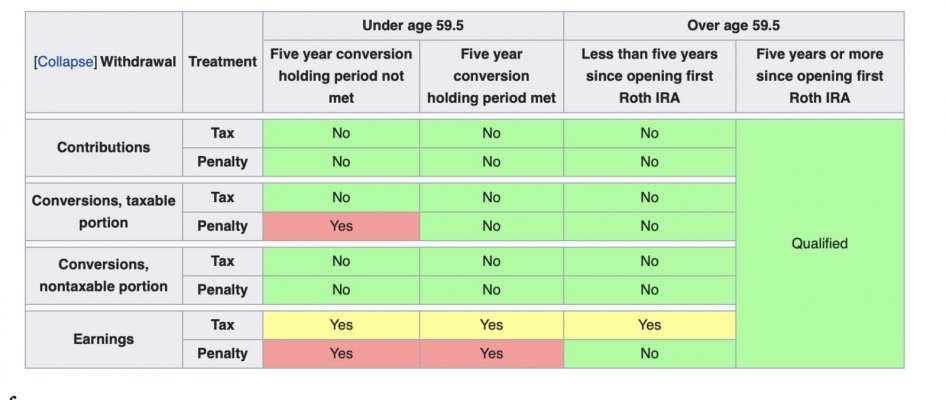

The only thing I get confused about is the 5 year rule after you are already 59 1/2. I think you can withdraw contributions tax free, but you have to wait 5 years before you withdraw earnings within the account tax free. I guess they just go by balance? Don’t know.

Does a Roth conversion open a new Roth IRA or can I just add to my old Roth?

If your old Roth is older than 5 years, you can forget about any 5 year rule. Even if you open a new Roth and put the money in it, o ruse the old Roth.

And if you are over 59.5.

I am under 59.5 and my oldest Roth is over 5 years old. However, I must still track the 5 year rule related to conversions.

Hey, don't give Congress any ideas...

Trust me. They've already thought of this.

Yea, adding "tax free" income like Roth withdrawals to MAGI calculations would be a sneaky/great way to increase stealth taxes* like IRMAA, SS taxation levels, and NIIT. They already add back "tax exempt" items like muni bond interest, so not a big leap.

*a term from retirement guru Bob Carlson.

IRMAA isn’t a tax, it’s a reduction of a subsidy.

IRMAA calculation is derived from IRS Form 1040, you know, a tax return. And the amount is based on your tax return MAGI and your tax filing status - single, MFJ, MSF. You can kid yourself all you want but it is part of our tax system - the very definition of a stealth tax. It is unfortunate that Congress has entwined health care with the income tax system, but it is a fact.

BubbaChris, clearing the 2nd to 3rd IRMAA hurdle by $1 would have increased a Medicare premium by $1,460/person for 2022. For a married couple that would be $2900+. In my opinion that is something to avoid.lawman,

Two lines of thoughts: first, congratulations on wanting to do your homework now to minimize your IMRAA impact later. I don’t begrudge you that at all.

Second, when I last evaluated 2022 IRMAA tiers for MFJ, the jump in costs into the second tier were roughly $1,500. Which was also roughly a 1% increase in effective tax rate. But it’s also a rounding error for dining out costs for many people at that income level. So is that $1,500 worth the work to avoid it?

Best regards,

Chris

BubbaChris, clearing the 2nd to 3rd IRMAA hurdle by $1 would have increased a Medicare premium by $1,460/person for 2022. For a married couple that would be $2900+. In my opinion that is something to avoid.

Even if it takes me 10 hours to figure out how to avoid our IRMAA, my payback rate is $290+ per hour - tax free!

Yes, going over any IRMAA cliff by $1 is something to avoid....clearing the 2nd to 3rd IRMAA hurdle by $1 would have increased a Medicare premium by $1,460/person for 2022. For a married couple that would be $2900+. In my opinion that is something to avoid.

We perform Roth conversions to fill the gap to the next (expected) IRMAA hurdle. It takes some work to track this, but the hourly wages for the work are good.Yes, going over any IRMAA cliff by $1 is something to avoid.

Whether it is Worth pushing through...IRMAA cliffs (i.e., going well beyond $1 over) is a different question.