The question how much financial help to give kids has been discussed before, with many opinions given on the subject. I recently helped my kids but expect 100% to be paid back. It starts with one of my kids and spouse trying to buy an FHA Repo, no problem qualifying, but then problem after problem creating delay after delay, to the point, 6 months had elapsed.

After reading about how MMM made an impulse home purchase, I looked into his method, at about the 4 month time frame, just in case I had to help with the purchase. Following his write up, I did the following.

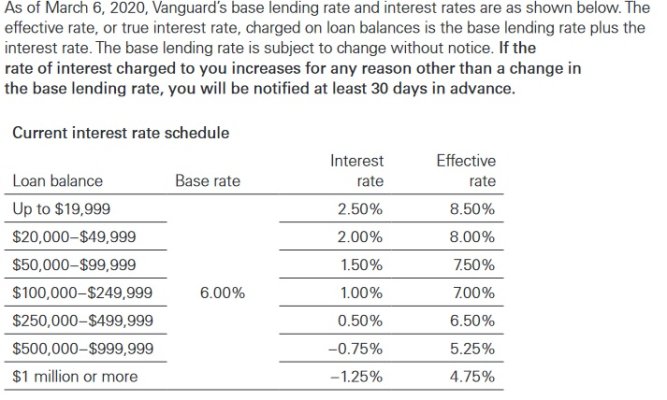

I opened an Interactive Brokers account and moved my Taxable account of Vangaurd mutual funds there. I don't want to sell and incur the tax hit. The account has Margin use available. I can margin up to 50% of my balance. I went 39%. More on that later*. I recently wired their homes purchase price to my bank. Then I had a mortgage written between them and me. I wired the money to the title company. They have the house I have a mortgage. The plan is for them to complete all repairs and make it ready for a traditional mortgage. I expect them to get a new mortgage within one year, I had the contract written for two years just in case. The interest rate for the margin loan is 1.35%. *If the market had a flash crash, causing my margin to go above the 50%, IBKR would sell some of my mutual funds to bring it back to 50%. I don't want that to happen. As a precaution, I opened a home equity loan against my house, I will transfer $100,000 into my IBKR account bringing my margin loan down to about 33%. The Home equity loan is only 0.99% for the first 6 months. I wrote the mortgage at 4% for the first year an 6% for the second, I hope that 6% is a big incentive for them to get the house mortgage ready.

I thought this might help others if they have funds they don't want to sell, but would like to make use of the money. More details on MMM blog.

After reading about how MMM made an impulse home purchase, I looked into his method, at about the 4 month time frame, just in case I had to help with the purchase. Following his write up, I did the following.

I opened an Interactive Brokers account and moved my Taxable account of Vangaurd mutual funds there. I don't want to sell and incur the tax hit. The account has Margin use available. I can margin up to 50% of my balance. I went 39%. More on that later*. I recently wired their homes purchase price to my bank. Then I had a mortgage written between them and me. I wired the money to the title company. They have the house I have a mortgage. The plan is for them to complete all repairs and make it ready for a traditional mortgage. I expect them to get a new mortgage within one year, I had the contract written for two years just in case. The interest rate for the margin loan is 1.35%. *If the market had a flash crash, causing my margin to go above the 50%, IBKR would sell some of my mutual funds to bring it back to 50%. I don't want that to happen. As a precaution, I opened a home equity loan against my house, I will transfer $100,000 into my IBKR account bringing my margin loan down to about 33%. The Home equity loan is only 0.99% for the first 6 months. I wrote the mortgage at 4% for the first year an 6% for the second, I hope that 6% is a big incentive for them to get the house mortgage ready.

I thought this might help others if they have funds they don't want to sell, but would like to make use of the money. More details on MMM blog.