TromboneAl

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Jun 30, 2006

- Messages

- 12,880

The results are probably depend a lot upon whether one is in the accumulation phase or decumulation phase.

This time I chose to do nothing. Already retired, there was no source of new funds to invest so I would have had to rebalance towards equities to try to take advantage of the dip. I compromised and didn't rebalance but also didn't panic and sell, just held.

")

It should come as no surprise those not yet retired, not living off their nest egg and usually still contribution to the pot are more likely to have recovered than those of us withdrawing from our stash...

The results are probably depend a lot upon whether one is in the accumulation phase or decumulation phase.

My retirement savings are at an all time high, but I think that's because I'm still in the accumulation phase. I'm not sure how to calculate what my return has been over the last several years, because my contributions have varied over that time. Is there a plug-in-the-numbers spreadsheet somewhere that I can use to figure this out?I am almost back to even on my investment return. As of yesterday my 5 year investment return was down -.3%.

Today was a big up day for my portfolio, so I may have a positive return now.

as it was a little over a year ago. That was scary!A hair short of the high but some of it was moved into real estate (paid off a $165K mortgage).

Edit: But we were adding to the pot until this year and still are not all the way back. Bottom line we took a hit!

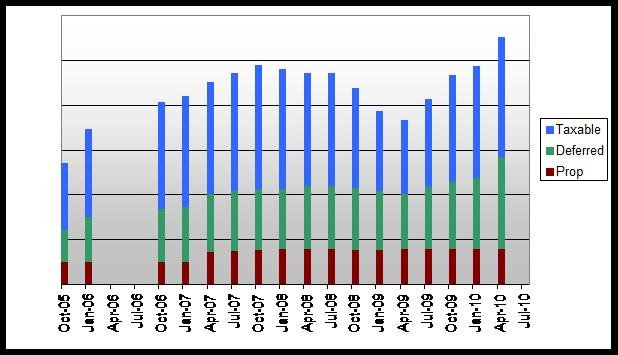

Pre-crisis high: May 2008

Crisis bottom: November 2008 (down almost 18% from the pre-crisis high)

Back to pre-crisis high: May 2009

Currently: all time high, 82% higher than pre-crisis high.

Still working, and still adding money to our portfolio.

Net worth since March 2001:

This makes me wonder how many people on the Board are calculating NW without accounting for liabilities.

I think we are getting a lot of apples, oranges, bananas, and grapefruits reported here. Hard to compare apples to apples.

My numbers above were based on net worth (assets minus liabilities). Assets being anything valuable enough to care about (cars, house, investments, accounts receivable, loans to family), liabilities being anything I owe (college loans, mortgage, credit card debt, an I O U to my daughter's piggy bank for $70).

I think there was a lengthy debate here a couple years ago about what should be included in net worth, and some suggested houses and mortgages have no place. If that were the case though, then I would call it something besides net worth.

I include liabilities (all of which mortgages on revenue properties and therefore good debt). I don't bother with personal property since I drive a 15 year old car and don't have any valuable antiques or artwork.

I agree. The definition of Net Worth is very clear in the accounting textbooks. If we are excluding real estate assets and liabilities, perhaps we could all it "investable assets".

Wow. I'd like to know how you got that last bit of almost vertical slope going!

Ah, the luck of the [-]Irish[/-] French.Ah, the magic of being granted a boat load of stock options near a market bottom...

I wasn't initially considering actual net worth - I was looking at my portfolio and mentally calculating the $165K back in to evaluate how close I was to the previous high. When I look at actual net worth including the current value of two houses I am a little worse off, or so I would guess based on the housing market.If you paid off a $165 liability with $165 of assets, the net effect on your net worth should be zero. This makes me wonder how many people on the Board are calculating NW without accounting for liabilities.

Ah, the luck of the [-]Irish[/-] French.

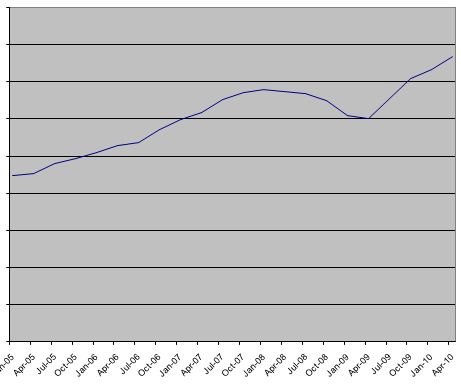

I also missed the part about NW.May 07 - Peak

Mar 09 - Trough

I'm still accumulating and I am too lazy to do the math to subtract the ongoing DCA and reinvested cap gains and dividends.

The good news is I am slowly creeping up on the May 07 peak value...just a little bit more.

I only counted my investment portfolio, i.e assets. No debt, no mortgage...only liabilities are COL expenses and taxes. And I'm a-going to keep it that way.

I only counted my investment portfolio, i.e assets. No debt, no mortgage...only liabilities are COL expenses and taxes. And I'm a-going to keep it that way. Hey, we only work 35 hours a week, give half of our earnings to the government and take 8 weeks of vacation a year. How are we supposed to reach FIRE without a bit of luck?

Sweet!Ah, the magic of being granted a boat load of stock options near a market bottom...

My retirement savings are at an all time high, but I think that's because I'm still in the accumulation phase. I'm not sure how to calculate what my return has been over the last several years, because my contributions have varied over that time. Is there a plug-in-the-numbers spreadsheet somewhere that I can use to figure this out?

Anyway, I'm just glad my balance isn't dropping faster than the contributions come in

Also, this is my retirement accounts only. If I count my house, I might still be going backwards. I'm pretty sure housing prices here haven't recovered anywhere near as much as the market has. There are five brand-new townhouses just down the street from me. They were finished some months ago but last time I checked, only one had sold. It went for about as much as the high appraisal I got on my residence in 2006, but is larger and newer, suggesting that my home would now sell for many thousands of dollars less.