|

|

11-24-2019, 10:20 AM

11-24-2019, 10:20 AM

|

#241

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote: Quote:

Originally Posted by target2019

Just checked 2 portfolios I set up on M*, so that I could track an actual portfolio set up by friend's FA. At the time (June 2018) I recommended 3 Vanguard funds that came very close to emulating the 9 fund approach of FA (Oppenheimer funds with > 1% e/r).

At 16 months, the INDEX is $8K ahead of the FA, then add the 1% FA fee. Someone could be $14K further along...

|

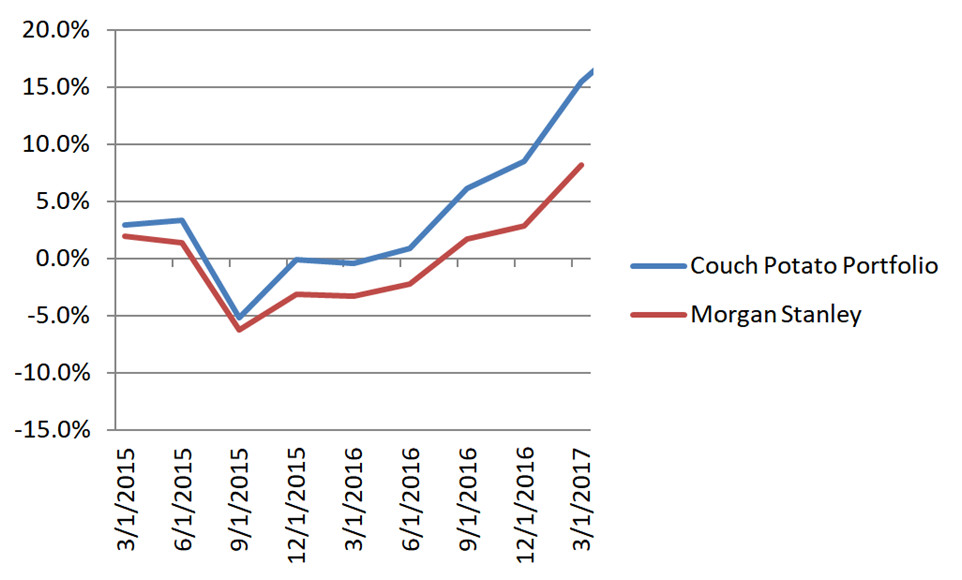

Yeah. Some of these FA portfolios are pretty bad. Here is some actual cumulative return data from a nonprofit I am involved with. The "couch potato" portfolio is $100K of real money, started out 1/1/2015 at 65% total US market and 35% total international, dividends reinvested and no rebalancing. The "Morgan Stanley" portfolio is the equity portion of a total portfolio created by a particularly inept pair of reps.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

11-24-2019, 10:37 AM

|

#242

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by OldShooter

The brutal truth here is that you have given him trivial money, which at a place like Chase is going to get you trivial attention. Your guy's sales manager is almost certainly asking why Chase even has the account. Your guy's answer is probably "Well he has more money and my plan is to capture it."

|

LOL, yes - that was all obvious to me because he tried many times (and failed) to have me move my serious accounts from Schwab. So he's bidding his time waiting for me to be seriously impressed but what he's doing

|

|

|

|

|

11-24-2019, 10:47 AM

|

#243

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by tenant13

LOL, yes - that was all obvious to me because he tried many times (and failed) to have me move my serious accounts from Schwab. So he's bidding his time waiting for me to be seriously impressed but what he's doing

|

Yeah, no surprise. But the rest of the story is that you are not going to learn much about FAs by hanging with some bozo at Chase, Morgan Stanley, RBC, etc.

BTW, have you run a brokercheck on this guy? ( https://brokercheck.finra.org/) It will probably be clean; most are. But I did look up one guy who had 22 customer disputes, many settled for six figures. And another who had lost his licenses for forging customer signatures on forms. Running brokerchecks is very cheap insurance.

|

|

|

|

|

11-24-2019, 11:17 AM

|

#244

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by OldShooter

Yeah, no surprise. But the rest of the story is that you are not going to learn much about FAs by hanging with some bozo at Chase, Morgan Stanley, RBC, etc.

BTW, have you run a brokercheck on this guy? ( https://brokercheck.finra.org/) It will probably be clean; most are. But I did look up one guy who had 22 customer disputes, many settled for six figures. And another who had lost his licenses for forging customer signatures on forms. Running brokerchecks is very cheap insurance. |

Clean and sparse record. He has limited experience and only rudimentary exams passed - not a word about being a CFP which is what I would be interested about. So no, I'm not going to learn much - it's ok, I doubt he'll do much damage to my 250k. I'll take a look at links you included. Thank you!

|

|

|

|

|

11-24-2019, 11:31 AM

|

#245

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by tenant13

... not a word about being a CFP which is what I would be interested about. ...

|

An FA having a CFP is, IMO, a good thing but it is (again IMO) seriously oversold.

The CFP is a designation that can be purchased from a private company after meeting their experience and training requirements. College degree? Yes. Mortuary Science? Just fine. 2 years experience. Receptionist an an FA firm? Fine. Then some exams. The guy that runs the CFP Board makes over $1M/year and his income depends on the number of CFPs they sell. So ... moral hazard.

Also importantly, a CFP is not legally a fiduciary. Until this year their code of conduct did not even mention the fiduciary duty of "loyalty" to clients. The revised version, out this fall, is better but in the end the CFP code has no teeth other than revoking a CFP certificate. Also, they say:

the Rules are not designed to be a basis for legal liability to any third party. Specifically their rules for CFPs are not designed to protect clients. So ... what's the point?

|

|

|

|

|

11-24-2019, 11:44 AM

|

#246

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by OldShooter

An FA having a CFP is, IMO, a good thing but it is (again IMO) seriously oversold.

The CFP is a designation that can be purchased from a private company after meeting their experience and training requirements. College degree? Yes. Mortuary Science? Just fine. 2 years experience. Receptionist an an FA firm? Fine. Then some exams. The guy that runs the CFP Board makes over $1M/year and his income depends on the number of CFPs they sell. So ... moral hazard.

Also importantly, a CFP is not legally a fiduciary. Until this year their code of conduct did not even mention the fiduciary duty of "loyalty" to clients. The revised version, out this fall, is better but in the end the CFP code has no teeth other than revoking a CFP certificate. Also, they say:

the Rules are not designed to be a basis for legal liability to any third party. Specifically their rules for CFPs are not designed to protect clients. So ... what's the point?

|

Thank you for all the info. I'm scheduled to meet with these guys: Mariner, Matthew DiQuollo - as per my free Schwab advisor who decided I need more comprehensive approach than what she can offer. It's an exploratory conversation but I already dread hearing all the pitches  I'll go because I'm determined to keep an open mind.

|

|

|

|

|

11-24-2019, 12:15 PM

|

#247

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by tenant13

Thank you for all the info. I'm scheduled to meet with these guys: Mariner, Matthew DiQuollo - as per my free Schwab advisor who decided I need more comprehensive approach than what she can offer. It's an exploratory conversation but I already dread hearing all the pitches I'll go because I'm determined to keep an open mind. |

DiQuollo's their sales guy. Brokercheck is clean. I suggest zeroing in on where your assets would be compared to their average and median. What services do you get beyond investment advice? A true financial advisor is much broader than an investment advisor.

Also read the two "Form ADV" reports linked here: https://www.marinerwealthadvisors.com/legal For any firm, always read the ADV before the meeting.

The ADV indicates that they offer "private funds." Usually a bad idea because you may not be able to easily sell and take your money elsewhere. Ask.

When you zero in on a firm, be sure to interview a couple of candidate advisors who would become "your guy." Philosophical fit and personal chemistry are important. Write down notes on all promises, time and date, especially anything you get from the sales guy.

You will leave the meeting smarter than you were when you came in. So ... a guaranteed good investment.

|

|

|

|

|

11-24-2019, 12:29 PM

|

#248

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by OldShooter

DiQuollo's their sales guy. Brokercheck is clean. I suggest zeroing in on where your assets would be compared to their average and median. What services do you get beyond investment advice? A true financial advisor is much broader than an investment advisor.

Also read the two "Form ADV" reports linked here: https://www.marinerwealthadvisors.com/legal For any firm, always read the ADV before the meeting.

The ADV indicates that they offer "private funds." Usually a bad idea because you may not be able to easily sell and take your money elsewhere. Ask.

When you zero in on a firm, be sure to interview a couple of candidate advisors who would become "your guy." Philosophical fit and personal chemistry are important. Write down notes on all promises, time and date, especially anything you get from the sales guy.

You will leave the meeting smarter than you were when you came in. So ... a guaranteed good investment. |

I already have a long list of specific questions and am going through their website, page by page - I don't want to waste time for generalities. They offer a lot of interesting services that I'd be interested in. For example trusts in relation to tax planning... I also would like to know if they can manage self-directed IRAs since I was always interested in investing in foreign real estate. Perhaps they could set up a foreign banking and a brokerage account as well... I don't need someone to just purchase a bunch of index funds for me and call it a day.

|

|

|

|

|

11-24-2019, 03:16 PM

|

#249

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2017

Location: Western NC

Posts: 4,633

|

Quote:

Originally Posted by OldShooter

DiQuollo's their sales guy. Brokercheck is clean. I suggest zeroing in on where your assets would be compared to their average and median. What services do you get beyond investment advice? A true financial advisor is much broader than an investment advisor.

Also read the two "Form ADV" reports linked here: https://www.marinerwealthadvisors.com/legal For any firm, always read the ADV before the meeting.

The ADV indicates that they offer "private funds." Usually a bad idea because you may not be able to easily sell and take your money elsewhere. Ask.

When you zero in on a firm, be sure to interview a couple of candidate advisors who would become "your guy." Philosophical fit and personal chemistry are important. Write down notes on all promises, time and date, especially anything you get from the sales guy.

You will leave the meeting smarter than you were when you came in. So ... a guaranteed good investment. |

Yeah, I got suckered into those a few years ago...still trying to get rid of them without taking a 35%+ haircut...

& the broker who sold them to me (collecting ~10% in commissions) has relinquished his license, so no chance of a FINRA claim, though he still operates his "advisory" firm...my advice is to stay far away.

|

|

|

|

|

11-24-2019, 03:23 PM

|

#250

|

|

Dryer sheet aficionado

Join Date: May 2019

Location: Harrison Township

Posts: 36

|

I do now. 10 yrs with a financial advisor hurt my returns. Took me too long to wake up.

Big mistake

|

|

|

|

|

11-24-2019, 05:12 PM

|

#251

|

|

Dryer sheet wannabe

Join Date: Aug 2017

Location: Idaho Falls

Posts: 14

|

I do my own investing and taxes. I did consult with Schwab when moving my 401k from employer's account to IRA with them. I've been pleased so far with the no pressure advice I have received.

|

|

|

|

|

11-25-2019, 06:03 AM

|

#252

|

|

Recycles dryer sheets

Join Date: Apr 2006

Posts: 150

|

Quote:

Originally Posted by Bruceski44

Using index funds makes self-management possible - all you'll really need to do, after determining which funds and your allocation to them, is to re-balance periodically.

I manage all our finances myself, but, importantly, I've also identified a FA my wife could work with after my death, should I die before her. This is a person I trust and who is familiar with my approach.

|

+1

This pretty much sums it up for us as well. We did visit once with a fee based FA to reassure my wife that I had half a clue managing ours. Turns out I did! He couldn't add any value to what I was already doing. But the fee was worth it to put her mind at rest.

__________________

Best!

-AJ

|

|

|

|

|

11-25-2019, 11:48 AM

|

#253

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Apr 2004

Location: South Texas~29N/98W Just West of Woman Hollering Creek

Posts: 6,674

|

Like other wise DIY investors, we have never squandered our stash by hiring a FA and indexing our RI in a few VG accounts. We have ridden it up and ridden down. Riding up is better but, my 45/45/10 AA allows for a smooth ride in any direction. Simplicity still rules in the mickeyd house.

__________________

Part-Owner of Texas

Outside of a dog, a book is man's best friend. Inside of a dog, it's too dark to read. Groucho Marx

In dire need of: faster horses, younger woman, older whiskey, more money.

|

|

|

|

|

11-25-2019, 05:50 PM

|

#254

|

|

Dryer sheet wannabe

Join Date: Sep 2015

Posts: 14

|

Quote:

Originally Posted by dirtbiker

You lost me at "what you may see as a great yearly return is likely what I pull out in a week." Classic internet bravado.

And then recommending whole life as opposed to term to a group of people who are actively planning for retirement? Pfft. Take the money you spend on whole life premiums, subtract the cost of a similar term life policy, invest the difference in an index fund and see where you're at. You're WAY better off with a term policy. If you're properly planning for retirement, the invested savings listed above alone will be worth far more than a whole life policy will be by the time a term life policy is up.

And then recommending an annuity? As a former life, health, and annuity insurance salesman, I'm going to guess you also drank the kool-aid? The only people I've ever known who recommend whole life and an annuity in the same breath are people working on commission to sell these products (like I once was). Oh, and the company I worked for instructed us to identify as 'advisers' or 'planners' instead of salespeople, which we actually were.  |

I had 10+ in the industry with the series 3,31,7,6(redundantly),63,66 & 57 life and health; with a few professional designations that are just feathers in the cap. I started trading the rbob & euro, became a full-service FA then transitioned back to proprietary trading derivatives. After that it was a decision to stay on board and watch my bar raised every year and/or take a head trader position. I'm nowhere near retirement. I made enough in bonuses alone; had experience and knowledge to trade on my own minus stress, politics and freedom to be nimble in the markets. A lot of young traders leave after a few years and travel the world or move onto different business ventures or professions. I've also seen a lot of really bright people realize it isn't what they thought it would be. And a trader takes himself out of the element doesn't mean he's going to do well, there's a learning curve even then. I'm definitely not the smartest person and I owe a lot to my background I believe.

I don't invest per se. You won't ever utilize the markets the way I do. I use currency futures and spot more-so. I rarely leave a position open overnight, my trades usually last a few minutes to hours. I place 1, maybe three round turn a day. Even my tax implications are different. A good week is around five percent. I see double digit in between and I've gone months without a weekly loss. I passed the three digit percentile back in March and I compound. Doesn't go my way all the time and there are independent traders much better than me. I know when to let off the throttle. Wouldn't trade it for the world...unless the world gives me some serious passive income...haha

There's a world of securities that the general investing public does not know about either. I made my fixed income clients' bear market with one product. A guaranteed 10% first year and a return based off a calculation between the 10 and 30TR with a third Libor leg. It was called back at the promised par with a 14% return AND it was FDIC insured...I doubt any of the FA and IAR's here know what it was let alone get this kind of product. You get what you pay for in the securities world.

The above goes for insurance. I don't need to explain all the benefits of whole/permanent life. But if your belief is "buy term and invest the difference" well - usually that's because you don't have enough of the difference. My clients may have been a bit more upstream, that's not to say it's a strategy only for higher brackets. From the statements I've seen disability, permanent life and annuity products alike are for people that have a lot invested in their lives...literally.

There's a fundamental flaw in just relying on the rate of return. Just like to a trader time in the market is money to be made or lost. Once that time goes away it's gone. I really hope for all the good people out there that market cooperates while you draw off your nest.

You read all the financial news and analysts trying to decipher why's and what's of a pull back....what investors aren't aware of is each time this happens, water is being tested. The traders; live, algo, hedgefunds...all of them are primed to start the short waves. It's just the nature of things. Forget the reasons, the cycles, the pricing or even the conspiracy theories. Preventing it is like trying to stop the winter - it just has to happen and it will. You aren't going to know whens and how longs. If it's big enough and you have a discretionary free cash, wait till the world is about to fall apart. Wait for the govt to start bailing out. That itself is the biggest form of manipulation. Then you start buying all the big and valuable names that got smashed somewhere along the line you'll be sitting very pretty - I promise. That's the only trading home investors should be doing.

It's really good to see people here taking a hold of their finances. One thing that interets me is that Wallstreet is finally succeeding in bringing in the millennial money with robo advisors and no fee brokerages. I don't have the numbers exactly, but that money is a big target for panic selling.

Being strictly a life and health salesman just doesn't cut it. I'm sure there's quite a few successful ones, but many were plate lickers.

I've said enough.

|

|

|

|

|

11-25-2019, 08:45 PM

|

#255

|

|

Recycles dryer sheets

Join Date: Aug 2018

Posts: 81

|

A few decades ago I had a full service broker. I will never forget him, good mentor for a younger me. But Since he passed in the mid 80s I have been on my own and done just fine, FIRED at age 56. Today is the golden age of investing and its not as hard as some would have you believe. Look at asset allocation, index funds, have a few stocks on the side if you want, and read Old Shooters recommend books and also read retire happy wild and free. Best of luck!

|

|

|

|

|

11-26-2019, 12:30 AM

|

#256

|

|

Full time employment: Posting here.

Join Date: Apr 2019

Posts: 630

|

Quote:

Originally Posted by allstock

I had 10+ in the industry with the series 3,31,7,6(redundantly),63,66 & 57 life and health; with a few professional designations that are just feathers in the cap. I started trading the rbob & euro, became a full-service FA then transitioned back to proprietary trading derivatives. After that it was a decision to stay on board and watch my bar raised every year and/or take a head trader position. I'm nowhere near retirement. I made enough in bonuses alone; had experience and knowledge to trade on my own minus stress, politics and freedom to be nimble in the markets. A lot of young traders leave after a few years and travel the world or move onto different business ventures or professions. I've also seen a lot of really bright people realize it isn't what they thought it would be. And a trader takes himself out of the element doesn't mean he's going to do well, there's a learning curve even then. I'm definitely not the smartest person and I owe a lot to my background I believe.

I don't invest per se. You won't ever utilize the markets the way I do. I use currency futures and spot more-so. I rarely leave a position open overnight, my trades usually last a few minutes to hours. I place 1, maybe three round turn a day. Even my tax implications are different. A good week is around five percent. I see double digit in between and I've gone months without a weekly loss. I passed the three digit percentile back in March and I compound. Doesn't go my way all the time and there are independent traders much better than me. I know when to let off the throttle. Wouldn't trade it for the world...unless the world gives me some serious passive income...haha

There's a world of securities that the general investing public does not know about either. I made my fixed income clients' bear market with one product. A guaranteed 10% first year and a return based off a calculation between the 10 and 30TR with a third Libor leg. It was called back at the promised par with a 14% return AND it was FDIC insured...I doubt any of the FA and IAR's here know what it was let alone get this kind of product. You get what you pay for in the securities world.

The above goes for insurance. I don't need to explain all the benefits of whole/permanent life. But if your belief is "buy term and invest the difference" well - usually that's because you don't have enough of the difference. My clients may have been a bit more upstream, that's not to say it's a strategy only for higher brackets. From the statements I've seen disability, permanent life and annuity products alike are for people that have a lot invested in their lives...literally.

There's a fundamental flaw in just relying on the rate of return. Just like to a trader time in the market is money to be made or lost. Once that time goes away it's gone. I really hope for all the good people out there that market cooperates while you draw off your nest.

You read all the financial news and analysts trying to decipher why's and what's of a pull back....what investors aren't aware of is each time this happens, water is being tested. The traders; live, algo, hedgefunds...all of them are primed to start the short waves. It's just the nature of things. Forget the reasons, the cycles, the pricing or even the conspiracy theories. Preventing it is like trying to stop the winter - it just has to happen and it will. You aren't going to know whens and how longs. If it's big enough and you have a discretionary free cash, wait till the world is about to fall apart. Wait for the govt to start bailing out. That itself is the biggest form of manipulation. Then you start buying all the big and valuable names that got smashed somewhere along the line you'll be sitting very pretty - I promise. That's the only trading home investors should be doing.

It's really good to see people here taking a hold of their finances. One thing that interets me is that Wallstreet is finally succeeding in bringing in the millennial money with robo advisors and no fee brokerages. I don't have the numbers exactly, but that money is a big target for panic selling.

Being strictly a life and health salesman just doesn't cut it. I'm sure there's quite a few successful ones, but many were plate lickers.

I've said enough.

|

You don't have enough of a difference? My clients are a bit more upstream? Is that your sales pitch to the elitists?

Let's take me for example. I have a 20 year term policy of $3 mil, fairly recently acquired. It costs me $175 per month. Fortunately I'm in excellent health. I just did a quick search for whole life quotes for the same $3 mil. About $3800 per month. That's a difference of $3600 per month. You're correct in that I don't have enough of the difference. In order to pay $3600 additional per month, that would have to come out of my monthly investment/retirement contributions. After 20 years in the market (if assuming the lifetime S&P 500 average return of 10%, which is what the bulk of my money is invested in), I'd have $2.7 million at age 57. At that point, I'd have an extra $175 a month to add to my monthly investments. The actuarial tables tell me I've got an average life expectancy of 78. So if I were to continue to contribute the same amount that the whole life policy costs for a further 21 years, assuming the same rates, I'd have $25 mil... Compared to the, at best, $3 mil on the whole life. And for sake of argument, if we went with a lower return of say 6%, it would give us numbers of $1.66 mil and $7.7 mil.

|

|

|

|

|

11-26-2019, 07:34 AM

|

#257

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by allstock

... I've said enough.

|

Thank you for that.

|

|

|

|

|

11-26-2019, 05:34 PM

|

#258

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2006

Location: Boise

Posts: 7,882

|

Quote:

Originally Posted by allstock

I've said enough.

|

I've heard enough. <plonk!>

__________________

"At times the world can seem an unfriendly and sinister place, but believe us when we say there is much more good in it than bad. All you have to do is look hard enough, and what might seem to be a series of unfortunate events, may in fact be the first steps of a journey." Violet Baudelaire.

|

|

|

|

|

11-30-2019, 11:24 AM

|

#259

|

|

Full time employment: Posting here.

Join Date: Dec 2018

Posts: 966

|

I managed my own portfolio which is now 100% treasury bonds because of the recession risk and I am currently withdrawing to invest into Real Estate. A FA should be consulted because a FA has the training, certification and experience that most people do not have. (Disclosure: My daughter is a FA with Charles Schwab.) A second opinion does not hurt and would only cost you $200 or so for 1 hour of consultation.

However, after you get that FA opinion and you are aware of the pros and cons and the risks and rewards of what you are doing, then it is perfectly fine to DIY after the consultation. What is valuable is that a FA also has access to other resources: Attorneys, Social Security specialists, Tax specialists, Estate planning, etc.

The correct information can be very powerful. There are some people who believe that they "knows it all". Those people may be exposed to some risks without realizing it. IMO, A one hour consultation with a FA on certain issues for a fee of $200 or so may be worth it for "some" people to get a second opinion by a FA who is trained, certified, experienced and regulated by the SEC.

|

|

|

|

|

12-03-2019, 08:28 AM

|

#260

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2017

Location: Champaign

Posts: 4,722

|

Not sure I'd call it "manage" our nest egg. We simply stay the course. A good thing in the longest bull market in history. Dips like today are concerning, but we've been here before.

__________________

"Do not go where the path may lead, go instead where there is no path and leave a trail."

Ralph Waldo Emerson

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|