Retch The Grate

Full time employment: Posting here.

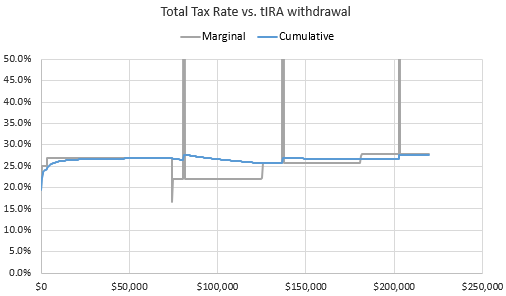

Before I got married I was consistent in adding to my Roth, but post-marriage, my wife and I are way above the cut-off as a couple (my income has gone up, and she was already a cybersecurity engineer at Google when we met). Looking at Roth conversions it seems like our marginal tax rate is way too high to consider doing conversions/backdoor Roth to be worthwhile but maybe I'm looking at it the wrong way? Everybody goes on about how great it is to do backdoor contributions, but as far as I can tell my taxes are likely to be substantially lower in retirement (we don't expect to need our combined current income to support our current lifestyle and we aren't aiming for higher).

Even when I stop working at some point, DW is 9 years younger than me and will keep going for a while most likely as our FI point got raised a lot by buying our house (I miss being FI, but I like our house and love my DW feeling safe and secure and able to put down roots), and it seems like the math is likely to stay in favor of not converting? But again, maybe I'm misunderstanding something about how to figure it out, all the articles I've read over the years act like it is a no-brainer for high income earners, but when I try to estimate it, it doesn't appear to be so...

Even when I stop working at some point, DW is 9 years younger than me and will keep going for a while most likely as our FI point got raised a lot by buying our house (I miss being FI, but I like our house and love my DW feeling safe and secure and able to put down roots), and it seems like the math is likely to stay in favor of not converting? But again, maybe I'm misunderstanding something about how to figure it out, all the articles I've read over the years act like it is a no-brainer for high income earners, but when I try to estimate it, it doesn't appear to be so...

")