Ticker

Recycles dryer sheets

Looks like the new rate for I bonds is growing smaller.

The composite rate for the next 6 months is now .26%,

announced today.

The composite rate for the next 6 months is now .26%,

announced today.

Looks like the new rate for I bonds is growing smaller.

The composite rate for the next 6 months is now .26%,

announced today.

I looked at the inflation figures on the US Bureau of Labor Statistics just a few days ago and noticed that the last 6 months seemed to add up to a very small number.Looks like the new rate for I bonds is growing smaller.

The composite rate for the next 6 months is now .26%,

announced today.

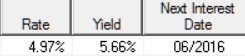

It is explained on treasurydirect.gov that the 0.26% annualized rate is comprised of a fixed rate of 0.1% plus a semi-annual inflation rate of 0.08%.

0.26% = 0.1% + 2 x 0.08%

However, several Web sites say that the year-on-year inflation rate for March 2016 was 0.9%. I have not found the source for the 0.16% inflation rate used in the formula above. Anybody who knows, please explain.

Guaranteed to never go negative. Might get stuck at 0% for a long time though.....I wonder how many people will buy when the rate goes negative?

I wonder how many people will buy when the rate goes negative?

While the inflation component can be negative, the composite rate cannot go below zero.I wonder how many people will buy when the rate goes negative?

Reference: https://www.treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_iratesandterms.htmIf the inflation rate is negative, it can offset some of the fixed rate.

If the inflation rate is so negative that it would take away more than the fixed rate, we don't let that happen. We stop at zero.

The exact change is mentioned below.I get 0.0 must be rounding difference instead of 0.08% (semi-annual rate).

Reference: https://www.treasurydirect.gov/news/pressroom/currentibondratespr.htmThe 0.26% composite rate for I bonds bought from May 2016 through October 2016 applies for the first six months after the issue date. The composite rate combines a 0.10% fixed rate of return with the 0.16% annualized rate of inflation as measured by the Consumer Price Index for all Urban Consumers (CPI-U). The CPI-U increased from 237.945 in September 2015 to 238.132 in March 2016, a six-month change of 0.08%.

I would like to buy a government bond linked to healthcare inflation. The fixed portion could be zero for all I care.

It is explained on treasurydirect.gov that the 0.26% annualized rate is comprised of a fixed rate of 0.1% plus a semi-annual inflation rate of 0.08%.

0.26% = 0.1% + 2 x 0.08%

However, several Web sites say that the year-on-year inflation rate for March 2016 was 0.9%. I have not found the source for the 0.16% inflation rate used in the formula above. Anybody who knows, please explain.

While the inflation component can be negative, the composite rate cannot go below zero.

Reference: https://www.treasurydirect.gov/indiv/research/indepth/ibonds/res_ibonds_iratesandterms.htm

The exact change is mentioned below.

Reference: https://www.treasurydirect.gov/news/pressroom/currentibondratespr.htm

I have been buying I Bonds since year 2000. I have accumulated interest of 145K

")

Only 14 years to go before the first bonds mature and stop earning interest