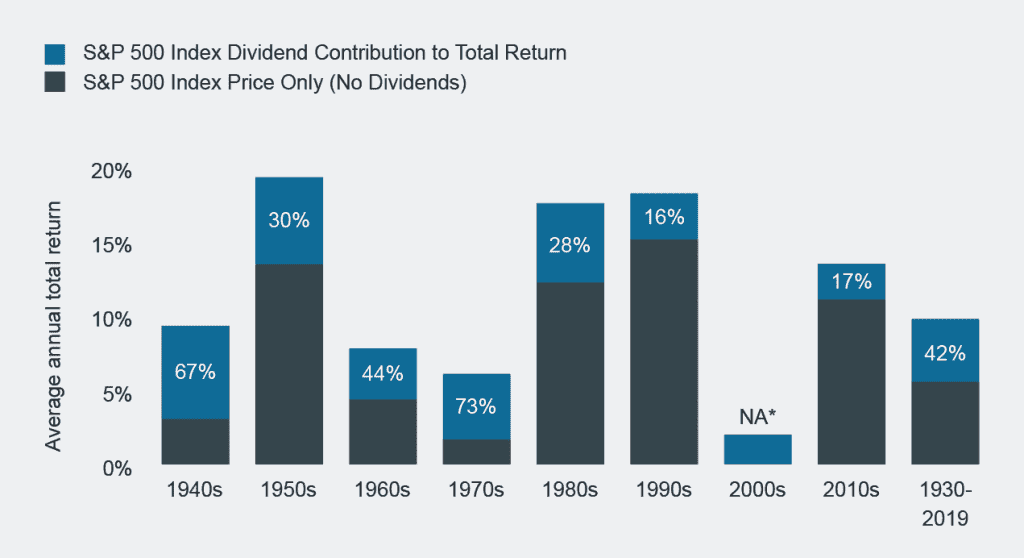

2007 - 2021 was an extended bull market. What else is there to know regarding the timeline? There are other dividend paying funds / etf's to choose from is there not? ...

I didn't choose that time-frame. It was based on looking for div-paying funds/ETFs that had some history. Those were the seven that I found with the longest history, and that dictated the time-frame.

Please find some others for me with an equal or greater history, I'd be interested in adding them to the list.

And I've already pointed out (twice now) what else is there to know regarding the timeline - there were dips, and those div sectors under-performed. The div folks keep telling me that the div sector holds up in dips. How come we don't see it?

...

What I did notice in the thread you copied were ignored counter-points.

I also noticed the post by RxMan that showed dividend payers outpaced in a down decade. ....

Please point out any counter-points I missed. I did see one, but then noticed that someone else responded. They covered it as well/better than I would have, so it was answered, no need for me to replicate it.

And as I mentioned, it appears that it would take a *lot* of effort (and probably taxes from trading) to duplicate that study. If it was easy, why don't these div sector funds show this performance boost? That is where the rubber meets the road.

... What you do get with VTI and other dividend paying funds are more unknown dividend payments. Keep in mind the investing purpose for dividend payments. Regular income. That is not the purpose of VTI, nor of the other funds.

...

I don't see the point. Money is fungible. As long as my portfolio is returning

value, it makes no difference (other than taxes, which favor a non-zero cost basis sale) if it is from divs or a combination of divs and growth (like VTI).

All I need for a steady income from VTI is to look at my divs once a year, and sell off enough to make up any delta between my annual expenses and those divs. Easy-peasy.

Dividend income is no simpler to deal with, and maybe more complex. If you spend less than divs, you need to go re-invest it. If you spend more than divs, you still need to do a sale. Sure, you could let the excess sit in cash until you need it, but that's gonna be a drag on performance. Seems highly unlikely that one's personal spending habits match exactly the div payouts, unless you want to let someone else dictate what you spend. No thanks.

... Want me to pick a good 12 year period to show 15%/25%/60% portfolio outperforming VTI where I can "only" choose certain time frames?

Take that same link and change the start year to 2009. You can create what ever answer you want. ....

Not interested in cherry-picked time frames. I could easily counter with cherry-picked times showing the opposite. No value to it. No thanks. Again, find some high-div sector funds with a longer history, I might have missed some. I'll be glad to take a look.

... I personally don't think Bonds or the NASDAQ are going to perform nearly as well over then next 10 years as they have over the last 10 years.

But I don't think I'm taking a big risk either way.

Could very well be. But I see no reason to think that the div sector would do better than the equivalent risk Total-Market/Bond portfolio. Do you?

I never said you are taking a

big risk. I demonstrated with data that these div paying sector funds do not deliver what the fans of them claim. They under-perform over the long run, they don't hold up better in the dips in their history, and they are less tax efficient.

But there certainly is risk to having $500,000 less in your portfolio that started with $1M in 2007, and that's where the div-sector investor would be. An extra 1/2 Million covers a lot of any future relative under-performance (if that even happens)

-ERD50