|

|

09-28-2020, 07:02 AM

09-28-2020, 07:02 AM

|

#21

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2014

Location: Syracuse

Posts: 3,502

|

Terrible article.

Quote: Quote:

Originally Posted by NW-Bound

When I started to contemplate ER, I thought about SORR a lot.

I am 64 now, and with 8 years of ER under my belt, I don't think about SORR anymore. I think more about running out of time.

Heh heh heh... Of course, YMMV.

|

62 and 7 years in I think I'm subject to SORR. Not as worried as I'm sure I can adjust and will live well, but I've become accustomed to being in the top 10%

Quote:

Originally Posted by Lsbcal

What is "failure" defined as in the failure rate?

My personal definition is having less then about half of our current portfolio after inflation adjusting.

Many people seem to use near zero as a "failure". That is totally unrealistic.

|

That's one of the great things of this game - each of us can decide what perimeters constitute a win.

Personally, if I hit 70 then start SS, own my home, and have $250k of today dollars stashed I'll consider it game won.

__________________

No, not rich. I am a poor man with money, which is not the same thing"

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

09-28-2020, 07:04 AM

|

#22

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2013

Location: Ventura County

Posts: 1,433

|

Another digression from the SORR discussion here, but the anecdotes about making it to Blythe, CA on a tank of gas remind me of an anecdote from my dim past 40 years ago. While still in college I was driving from Phoenix back to LA at the end of spring break. Being young and foolish the empty desert of western Arizona encouraged me to put my foot down and see how fast my crappy car would go. So I got it up to maybe 120, glanced down and saw the temperature gauge buried in the red. Yikes. Shut down the engine immediately and was able to coast for a couple of miles to the little town of Quartzite, AZ and its one service station. I got a mechanic there to take a look at my car. After doing so he came over to me and said the four most terrifying words in the English language:

"You'll like our town"

|

|

|

|

|

09-28-2020, 08:27 AM

|

#23

|

|

Thinks s/he gets paid by the post

Join Date: Jan 2020

Location: Milwaukee

Posts: 4,053

|

Quote:

Originally Posted by Lsbcal

What is "failure" defined as in the failure rate?

My personal definition is having less then about half of our current portfolio after inflation adjusting.

Many people seem to use near zero as a "failure". That is totally unrealistic.

|

I was dismissive of this work upthread, although this was based solely on the MarketWatch description of it; I have not found the paper.

However, I wanted to point out that I first became familiar with this very author, Javier Estrada, for his work on trying to formulate a better measurement of "failure." As Lsbcal points out, reaching zero = "failure" is a poor metric. Running $10 short in your 30th year is a lot different than running out of money entirely in your 20th year.

Estrada introduces a "coverage ratio" to rank a withdrawal strategy. It takes into account the fraction of planned retirement spending achieved, and also weights it by a given utility function.

The paper can be found here: https://papers.ssrn.com/sol3/papers....act_id=3135125

|

|

|

|

|

09-29-2020, 05:46 AM

|

#24

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2014

Location: Dallas

Posts: 1,155

|

Quote:

Originally Posted by Lsbcal

What is "failure" defined as in the failure rate?

My personal definition is having less then about half of our current portfolio after inflation adjusting.

Many people seem to use near zero as a "failure". That is totally unrealistic.

|

I actually define failure as portfolio value dropping below 100% of inflation adjusted portfolio value! This is due to the fact that I have a special need child and I am planning for his retirement as well. Thankfully I can "run" this scenario using FireCalc. I simply pay attention to the lowest portfolio value in the FireCalc results page and compare that with the starting portfolio value. I am "safe" as long as they are same!

|

|

|

|

|

09-29-2020, 08:05 AM

|

#25

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: May 2006

Location: west coast, hi there!

Posts: 8,809

|

GravitySucks makes the point that each of us can decide what constitutes a good outcome.

We should just make sure the outcome of our strategy would have worked with past data. If a minimum is reached during the years we are retired that would be unacceptable then consider changing your strategy now.

I usually look at the 1966 start as that reaches a minimum in 1982 before heading up again. Turns out the stock/bond ratio is not that big a factor for that start date to 1982.

|

|

|

|

|

09-29-2020, 08:51 AM

|

#26

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,147

|

Quote:

Originally Posted by Lsbcal

What is "failure" defined as in the failure rate?

My personal definition is having less then about half of our current portfolio after inflation adjusting.

Many people seem to use near zero as a "failure". That is totally unrealistic.

|

Our %remaining portfolio withdrawal method has a 51% real portfolio remaining worst case after 30 years (and interestingly about same after 40 years) at a 4.35% withdrawal rate. Ive considered that acceptable. On average 100% of the portfolio remaining which is way more than acceptable. Thats for a portfolio of 50% total stock market, 50% 5 year treasuries.

__________________

Retired since summer 1999.

|

|

|

|

09-29-2020, 11:01 AM

|

#27

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: May 2006

Location: west coast, hi there!

Posts: 8,809

|

Quote:

Originally Posted by audreyh1

Our %remaining portfolio withdrawal method has a 51% real portfolio remaining worst case after 30 years (and interestingly about same after 40 years) at a 4.35% withdrawal rate. Ive considered that acceptable. On average 100% of the portfolio remaining which is way more than acceptable. Thats for a portfolio of 50% total stock market, 50% 5 year treasuries.

|

What about at the minima which might occur somewhere in the middle of the sequence? Your numbers do sound very safe indeed.

During this pandemic I notice how little we need to have a comfortable life at far below our normal spending rate. Not saying I want to do this but it can still be pleasant. So a 2% reduction in spending is ok for us but not part of the planning.

|

|

|

|

|

09-29-2020, 11:59 AM

|

#28

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,147

|

Quote:

Originally Posted by Lsbcal

What about at the minima which might occur somewhere in the middle of the sequence? Your numbers do sound very safe indeed.

During this pandemic I notice how little we need to have a comfortable life at far below our normal spending rate. Not saying I want to do this but it can still be pleasant. So a 2% reduction in spending is ok for us but not part of the planning.

|

The 4.35% rate experiences a worst case real income drop of 60% before recovering*. It’s a very slow gradual decline over more than a decade. Ironically, because your initial withdrawal rate is so much higher, the actual $ amount at lowest income is still higher than if you selected a lower withdrawal rate. So you get down to a bit above the same $ amount, but you had much more income received during the early years. With more conservative withdrawal rates you still see a potential large income drop - up to 49% real with a 3% withdrawal rate, for example. The average ending portfolio for the lower withdrawal rates are higher - so that’s the main advantage of a lower withdrawal rate - more remaining.

The main issue with this method - other than deciding how low you want to let your portfolio go - is what strategies to use to handle highly variable annual income and a potential long streak of dropping real income.

*just to be clear this is the same as the max real drawdown of the portfolio since you are taking a fixed % out every year.

__________________

Retired since summer 1999.

|

|

|

|

|

09-29-2020, 02:12 PM

|

#29

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2008

Posts: 35,712

|

Quote:

Originally Posted by pjigar

I actually define failure as portfolio value dropping below 100% of inflation adjusted portfolio value!

|

Below 100% at the 30-year end, or at any point in the 30 years period?

If at any point, then the failure rate would very high, somewhere between 1/3 and 1/2.

One can see this easily by running FIRECalc with a portfolio of 1 million, 0% WR, retirement period of 2 or 3 years.

Quite often, the portfolio immediately drops below 1 million after the 1st year even with no withdrawal. At the end of Year 3, it could be below $700K for a 50/50 portfolio.

__________________

"Old age is the most unexpected of all things that happen to a man" -- Leon Trotsky (1879-1940)

"Those Who Can Make You Believe Absurdities Can Make You Commit Atrocities" - Voltaire (1694-1778)

|

|

|

|

|

09-29-2020, 02:40 PM

|

#30

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

Quote:

Originally Posted by NW-Bound

Below 100% at the 30-year end, or at any point in the 30 years period?

If at any point, then the failure rate would very high, somewhere between 1/3 and 1/2.

One can see this easily by running FIRECalc with a portfolio of 1 million, 0% WR, retirement period of 2 or 3 years.

Quite often, the portfolio immediately drops below 1 million after the 1st year even with no withdrawal. At the end of Year 3, it could be below $700K for a 50/50 portfolio.

|

Right, you'd have to retire with more than 100% of what you want as your lowest point.

|

|

|

|

|

09-30-2020, 10:19 AM

|

#31

|

|

Recycles dryer sheets

Join Date: Feb 2014

Location: Austin

Posts: 247

|

Quote:

Originally Posted by RunningBum

My issue with SORR is that it doesn't seem to factor in early retirement. For a 30 year plan of a 65 yo retiree, it might make sense, but not so much for 40 or 50 years of an early retiree.

Take two people, both 45. Person A retires at 45, and sets their AA conservatively due to SORR risk, with a glide path of 10 years. After 10 years of low to moderate gains, they feel they have avoided SORR and go with their planned 50/50 or 60/40 AA.

Person B is now 55 as well, and just starting ER. They have the same amount of investments as Person A, and the same expenses. Since they are just starting, they reduce their equity investment due to SORR.

So both A and B have the same future in front of them, but A thinks they are clear of SORR, while B thinks they are exposed. How does that make sense?

Personally, I don't think it matters to me anymore. I retired nearly 10 years ago, and this has been a great run to give me a lot of buffer. Even though I'm 58 with hopefully plenty of years to go, I'm not worried about SORR. I've got enough non-equities to get me through a few years of a down market, and my VPW plan will throttle me back through the down years. I don't recall SORR being aware of SORR in 2011. I can't say for sure what I would've done.

|

I believe SORR risk is always present, but only for withdrawal rates that are on the edge of being viable. For early retirees, I suspect the withdrawal rates are usually well below nonviable withdrawal rates, as in your case. It might be interesting, though, to see what historical SWRs are for number of retirement years left.

I would like to point out that if one is concerned about SORR, then a glide path is not a good strategy. It exposes one to all the SORR risk up front when the stock percentage is high, but eliminates the possibility of portfolio recovery later by lowering the percent stock in a portfolio as time goes by.

|

|

|

|

|

09-30-2020, 11:07 AM

|

#32

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

Quote:

Originally Posted by Navigator

I would like to point out that if one is concerned about SORR, then a glide path is not a good strategy. It exposes one to all the SORR risk up front when the stock percentage is high, but eliminates the possibility of portfolio recovery later by lowering the percent stock in a portfolio as time goes by.

|

I think I misused the term "glide path". What I meant was someone starting off with a low equity AA, and increasing there AA over the next 10 years to get to their target, trying to avoid SORR in the early years.

|

|

|

|

|

09-30-2020, 02:36 PM

|

#33

|

|

Recycles dryer sheets

Join Date: Jun 2008

Posts: 155

|

Quote:

Originally Posted by RunningBum

I think I misused the term "glide path". What I meant was someone starting off with a low equity AA, and increasing there AA over the next 10 years to get to their target, trying to avoid SORR in the early years.

|

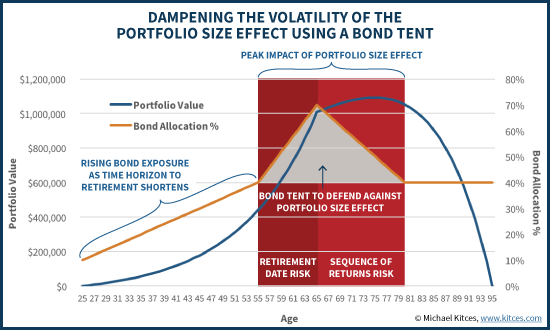

I believe Kitces refers to this as a reverse equity glidepath.

|

|

|

|

|

09-30-2020, 03:01 PM

|

#34

|

|

Thinks s/he gets paid by the post

Join Date: Jan 2020

Location: Milwaukee

Posts: 4,053

|

|

|

|

|

|

09-30-2020, 04:01 PM

|

#35

|

|

Thinks s/he gets paid by the post

Join Date: Nov 2014

Location: Austin

Posts: 1,384

|

Quote:

Originally Posted by audreyh1

The 4.35% rate experiences a worst case real income drop of 60% before recovering*. Its a very slow gradual decline over more than a decade. Ironically, because your initial withdrawal rate is so much higher, the actual $ amount at lowest income is still higher than if you selected a lower withdrawal rate. So you get down to a bit above the same $ amount, but you had much more income received during the early years. With more conservative withdrawal rates you still see a potential large income drop - up to 49% real with a 3% withdrawal rate, for example. The average ending portfolio for the lower withdrawal rates are higher - so thats the main advantage of a lower withdrawal rate - more remaining.

The main issue with this method - other than deciding how low you want to let your portfolio go - is what strategies to use to handle highly variable annual income and a potential long streak of dropping real income.

*just to be clear this is the same as the max real drawdown of the portfolio since you are taking a fixed % out every year.

|

Yep, variable withdrawal methods trade off the concept of running out of money prematurely with the possibility of any single year's withdrawal perhaps not being enough to live on if you experience a bad sequence of returns somewhere along the way. Even then there are ways to help mitigate that as well, the simplest one being that you don't actually have to withdraw and/or spend the extra during windfall years when your portfolio did great. The extra can just be kept in the portfolio to (hopefully) grow over time or it can be banked until needed for a rainy day. Not quite as easy if it happens right at the beginning of your retirement - which is another way of saying "save more" before you pull the plug.

Some methods, like PMT-based methods which include VPW over on bogleheads and similar methods which use rough, updated estimates of future returns can be created to computationally result in having exactly $X after Y years. X can then be determined based on wanting to leave a bequest or can can be designed to be $0 if you like. Up to you. Of course the trajectory that your portfolio takes from year zero to Y years from now is wholly unpredictable going forward, but you can at least get a glimpse of what might have happened in the past with such methods.

Cheers,

Big-Papa

|

|

|

|

|

09-30-2020, 04:16 PM

|

#36

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,147

|

Quote:

Originally Posted by RunningBum

I think I misused the term "glide path". What I meant was someone starting off with a low equity AA, and increasing there AA over the next 10 years to get to their target, trying to avoid SORR in the early years.

|

Glide Path as I am familiar with it starts with low equity exposure - 30% for Kitces optimum example, and increases with age.

__________________

Retired since summer 1999.

|

|

|

|

|

09-30-2020, 05:58 PM

|

#37

|

|

Thinks s/he gets paid by the post

Join Date: Nov 2014

Location: Austin

Posts: 1,384

|

Quote:

Originally Posted by audreyh1

Glide Path as I am familiar with it starts with low equity exposure - 30% for Kitces optimum example, and increases with age.

|

Before the Kitces article came along, the standard definition of a glidepath used by almost all target date funds was to start off with high equity in the early years of accumulation and reduce it over time. There were discussions about whether the glide path continued on into retirement (so-called "through retirement" glide paths) or whether it froze once retirement started (so-called "to retirement" glide paths. Many articles in the last few years suggesting it's not the best idea around. So many ideas like glide paths are built around the idea of a steady income stream in retirement, like the so-called 4% rule. If that's not what you're using many such ideas make no sense.

For more than you ever really wanted to know about standard glidepaths:

https://www.bogleheads.org/wiki/Glide_paths

Cheers,

Big-Papa

|

|

|

|

|

10-03-2020, 08:09 PM

|

#38

|

|

Recycles dryer sheets

Join Date: Nov 2018

Location: Vung tau

Posts: 121

|

I am reading "Nomadland" now and it will really make you appreciate what all/most of us in this forum have and the sense of security and freedom it gives us. SORR is the last thing the people in the book are worried about. They want to make it thru next month, week or even the day.

I do take issue with one thing in the book - the author calls those with finances able to comfortably handle retirement "lucky". Clearly she needs to come and write about the people in this forum because for most of us, I am willing to bet, luck had nothing to do it with it.

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode