COcheesehead

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

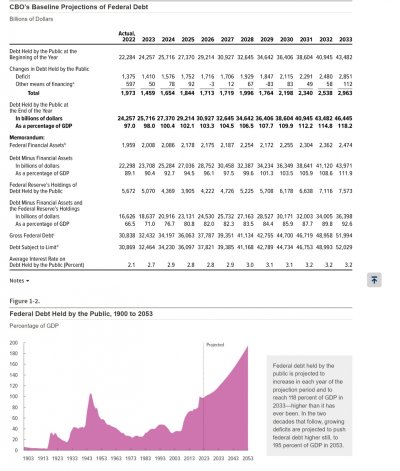

Has there been a curve this steep before?

Why not look at the 10 year performance of these funds? That should give you a total picture of the "loss sharing" absorbed by many passive index funds.

I have. BND, for example, matches its benchmark to within a smidge:

Month-end 3-Month total YTD 1-yr 3-yr 5-yr 10-yr Since inception (04/03/2007)

BND (Market price)

2.69% 3.28% 3.28% -4.70% -2.71% 0.94% 1.33% 2.99%

BND (NAV)

2.61% 3.18% 3.18% -4.73% -2.79% 0.93% 1.33% 2.99%

Bloomberg US Aggregate Bond Index

2.60% 3.01% 3.01% -4.72% -2.73% 0.95% 1.39% 3.05%

This was the point Audrey made upthread. If pb4's contention that buying and selling due to turnovers affects fund performance, then that under- (or over-) performance should show up relative to its benchmark. (The benchmark has no turnover-induced buying/selling.)

This point is distinct from the main one found in the many "bond funds are not bonds" threads. I have already agreed that the buying and selling that is necessary to maintain duration, etc., may be deleterious (or salubrious) to the fund, depending on the rate environment. But this thread is about bond funds.

The current yield curve is not steep, rather inverted.

I realize Wellington is only about 40% bonds, but it seems like it will never recover its highs.

Has there been a curve this steep before?

The yield curve has not been this inverted since the early 1980s when the Fed was last furiously battling inflation. It was even more inverted back then.Bad choice of words on my part. Inverted.

The yield curve has not been this inverted since the early 1980s when the Fed was last furiously battling inflation. It was even more inverted back then.

Hit MAX for range on the graph here: https://fred.stlouisfed.org/series/T10Y2Y

I realize Wellington is only about 40% bonds, but it seems like it will never recover its highs.

I have. BND, for example, matches its benchmark to within a smidge:

Month-end 3-Month total YTD 1-yr 3-yr 5-yr 10-yr Since inception (04/03/2007)

BND (Market price)

2.69% 3.28% 3.28% -4.70% -2.71% 0.94% 1.33% 2.99%

BND (NAV)

2.61% 3.18% 3.18% -4.73% -2.79% 0.93% 1.33% 2.99%

Bloomberg US Aggregate Bond Index

2.60% 3.01% 3.01% -4.72% -2.73% 0.95% 1.39% 3.05%

This was the point Audrey made upthread. If pb4's contention that buying and selling due to turnovers affects fund performance, then that under- (or over-) performance should show up relative to its benchmark. (The benchmark has no turnover-induced buying/selling.)

This point is distinct from the main one found in the many "bond funds are not bonds" threads. I have already agreed that the buying and selling that is necessary to maintain duration, etc., may be deleterious (or salubrious) to the fund, depending on the rate environment. But this thread is about bond funds.

Passive bond and equity funds are designed to take advantage of easy money policies.

Oh? Any authorities you can cite on this?

That's how I have access... I'm a subscriber and did a gift link. I also subscribe to NYT. Had WSJ but it went up over $20/month and I wasn't using it enough. Might do Barrons trial though. Perhaps I shouldn't be so [-]cheap[/-]frugal.

Aren't we supposed to set out asset allocations and ignore the noise?