OP

OP

audreyh1

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Are we limited to them only? Can I choose Candice Bergen?

Hmm - Liz Ann Sonders might meet your criteria.

Are we limited to them only? Can I choose Candice Bergen?

This is why I plan to stay with my company that provides a pension for the rest of my career.

The pension may be the only way I can make ER viable given my non-impressive income.

I had a similar plan, but Megaconglomocorp had a different plan...

It also helps that politicians have public pensions, too.I have a public pension. I'd rather that than a private Megacorp pension because i feel it's safer from "changes". At least the unions an myself can lobby the politicians to protect it.

Seems silly I don't know - but I was looking at year end tax stuff and I had never realized that bond funds also pay a dividend. I had thought that was just stocks.

When people talk about lower long term bond yields of 1-2% I'm assuming that includes the dividend? Is that right?

Thanks

Seems silly I don't know - but I was looking at year end tax stuff and I had never realized that bond funds also pay a dividend. I had thought that was just stocks.

When people talk about lower long term bond yields of 1-2% I'm assuming that includes the dividend? Is that right?

Thanks

Audrey,I have been thinking about market valuations recently. CAPE10 is at 27!, and although 10-year treasuries have backed up to 2.25%, they are still about 150bp from median.

It was good to read this again - especially Gone4Good's portfolio discounting model for a withdrawal rate sanity check.

I have been thinking about market valuations recently. CAPE10 is at 27!, and although 10-year treasuries have backed up to 2.25%, they are still about 150bp from median.

It was good to read this again - especially Gone4Good's portfolio discounting model for a withdrawal rate sanity check.

Holding stocks long-term is similar to holding bonds to maturity . . . you earn your current yield.

At a 24x PE, we're getting an earnings yield of about 4%. At 16x we're getting an earnings yield of 6.25%. Therefore, all else being equal, you expect to earn 200bp less from stocks today over the long term than if you bought them at median valuations.

Yes, inflation adjusted. So, a "failure" might just mean that at the end of 30 years the portfolio was just a tiny bit in real value from the starting amount.Is that inflation adjusted as well? If in real terms as you said, yes.

Yes, inflation adjusted. So, a "failure" might just mean that at the end of 30 years the portfolio was just a tiny bit in real value from the starting amount.

And, just to clarify, the "failure" of a "% of remaining portfolio" withdrawal method method only means that the portfolio was below the real starting value at the very end of the period. It's just a snapshot at the end of the run.I remember a few years ago when Midpack discovered this FIRECALC quirk for the % of remaining portfolio method and pointed it out.

To me that means you aren't discovering some safe withdrawal rate for the discounted median case, but rather a rate at which the portfolio would likely be self-perpetuating. Quite a different animal.

If failure was allowed to be something like dropping below 1/2 of the original value in real terms, the supported withdrawal rate would be higher.

Your posted graph was blank for some reason.

Thanks, I'd forgotten about that "feature." Maybe the file below will show up.The link to the graph will not work. You need to capture the graph to a bitmapped graphics file, then post it.

I think it is going to be tough to beat the "fixed dollar amount adjusted for inflation" withdrawal method. Converted to percentage of current portfolio value, it will be low during boom years, and high during lean years. This allows surplus to be built up in good years to be spent in bad years.

The method of "fixed percentage of remaining portfolio" will not run out of money, but that's because it can choke off the withdrawal to a trickle.

On a related topic, there was a link (from poster Charlie) to Gummy-stuff's website yesterday that discussed a withdrawel plan where you took a 3% SWR that was augmented with some percentage of your portfolio gain over the inflation rate (ie. 50%). Basically you only take extra money out when the portfolio exceeds that for a 3% SWR plus inflation. The survival rates were the same as using a 4% SWR.

sensible withdrawals

This approach gives you (on average) a better income stream early in your ER and then it declines with time but never below the 3 % rate. Most ER's could use more cash early rather than later.

Did any of you see this ? What is your reaction ? It looks intriguing to me.

A Traditional 4% SWR on a million dollar portfolio would give you a constant $40k income adjusted for inflation. The Gummy-stuff approach gives you an initial expected income of $62k (inflation adjusted) or so declining to ~$37k (inflation adjusted) as you approach year 40 of ER with the longevity performance the same as the (safe) 4% withdrawal rate.

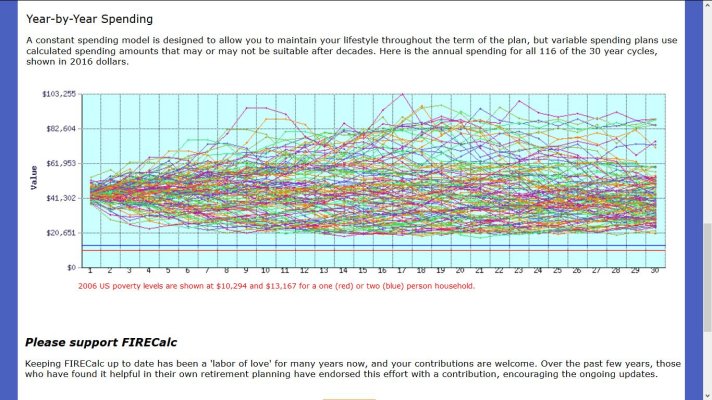

... Below is the run for a $1M starting portfolio, 50% TM/50% 5yr Treas, using a 4.5% end-of-year withdrawal method. To me it looks like the overall trend of the 116 runs is slightly downward, and that there are a small but not insignificant number of case where, at some point, the real withdrawal amount dipped below $22,500 (i.e. 50% of the starting amount). Some folks might be comfortable with this, some might not.

Right, but:Starting with drawing $45K from a $1M portfolio, this graph shows that in the worst cases, you will not be broke but stay hungry for decades living on just $20K.