|

How Is Your Private Sector Pension Doing ?

04-27-2018, 02:37 PM

04-27-2018, 02:37 PM

|

#1

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2013

Posts: 1,561

|

How Is Your Private Sector Pension Doing ?

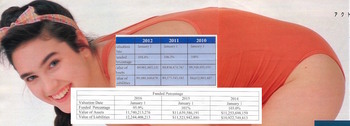

Mine

& One Question.......

Ok, I was bored, so I made the GIF from a you-tube video

Obviously, I don't expect anyone from this forum to answer the question. It was tongue-in-cheek.

But..........I 'was' wondering if anyone else here has seen this trend with their 'private sector' pension ?

__________________

"No beast so fierce but knows some touch of pity, but I know none, therefore am no beast"

Shown @ The End Of The Movie 'Runaway Train'

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

04-27-2018, 02:44 PM

|

#2

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,227

|

I see the same trend, though your numbers are about 5-6% better than mine. Mine were further off in 2016 but not as big of a drop in 2017. Supposed to be a very blue chip company too. Big blue chip. It's not a big part of my retirement plan though.

|

|

|

|

|

04-27-2018, 02:49 PM

|

#3

|

|

Thinks s/he gets paid by the post

Join Date: Oct 2009

Posts: 2,115

|

Its certainly not safe. At least if that guy is your dentist.

__________________

Of all the paths you take in life, make sure a few of them are dirt. John Muir

|

|

|

|

|

04-27-2018, 04:41 PM

|

#4

|

|

gone traveling

Join Date: Oct 2015

Posts: 138

|

Total plan assets @SoY 2017 = $210,640,290

2017, with / without adjusted rates = 107.2% / 87.4%

2016 = 109.2% / 89.8%

2015 = 108.9% / 88.2%

Looks OK to me.

|

|

|

|

|

04-27-2018, 04:49 PM

|

#5

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2009

Posts: 2,985

|

They send me a check for a few hundred every month. It's not worth looking into the details.

__________________

Took SS at 62 and hope I live long enough to regret the decision.

|

|

|

|

|

04-28-2018, 09:48 AM

|

#6

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2011

Posts: 1,288

|

I looked at it yesterday buy already filed. I is consistent with OP. My concern is I retired from a company and then my division was sold. Then, the acquiring company sold 'my' division.

The acquiring company now manages my pension. It is a large public company (I retired from a large private company). The public company appears to be doing OK and they have employees on a defined benefit plan. My consternation is lessen a bit with PBIC but I would simply have felt better if my pension was managed by a company I know and could find my way around if I had questions or issues.

|

|

|

|

|

04-28-2018, 10:44 AM

|

#7

|

|

Thinks s/he gets paid by the post

Join Date: Jan 2017

Posts: 2,657

|

The numbers are very close to the one I received today from one company I worked for. I have no clue if it's good or bad, but I suppose if it stays near 100% that's OK.

|

|

|

|

|

04-28-2018, 10:59 AM

|

#8

|

|

Administrator

Join Date: Jan 2008

Location: Chicagoland

Posts: 40,706

|

The year to year change in pension funding should reflect two things. First, the increase in liability should be completely funded. Second, part of the prior unfunded liability should also be funded.

More data would be needed to see what is happening with the pension in the OP, but at first glance it looks like neither of these things are happening. The rapid increase in total funding shortfall is troubling.

|

|

|

|

04-28-2018, 11:42 AM

|

#9

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2011

Posts: 1,288

|

Quote: Quote:

Originally Posted by davef

I looked at it yesterday buy already filed. I is consistent with OP. My concern is I retired from a company and then my division was sold. Then, the acquiring company sold 'my' division.

The acquiring company now manages my pension. It is a large public company (I retired from a large private company). The public company appears to be doing OK and they have employees on a defined benefit plan. My consternation is lessen a bit with PBIC but I would simply have felt better if my pension was managed by a company I know and could find my way around if I had questions or issues.

|

I decided to not be so lazy and get my stuff out of the file

2015 - 104/86

2016 - 95/80

2017 - 72/87 - funding shortfall is $8mm adjusted and $21mm not adjusted for interest rates. That 72% number is not comforting.

|

|

|

|

|

04-28-2018, 02:46 PM

|

#10

|

|

Moderator

Join Date: Apr 2012

Location: San Diego

Posts: 14,211

|

My pension(s) are in much worse shape than yours... But they are such a small amount and small amount of my retirement spending that I'm not too worried. My percentages were in the low 80's % for percent funded... and the trend is going to smaller/lower percentages YoY.

But my pensions only provide about 6% of my total spending needs.... so I should survive, even if the pensions don't.

And the pensions are from two different fortune 500 companies - one was acquired by the other and that pension froze. The 2nd was spun off and the pension frozen in the mid '00s .. The corporation that owns and manages both pensions is still around and doing ok.

__________________

Retired June 2014. No longer an enginerd - now I'm just a nerd.

micro pensions 6%, rental income 20%

|

|

|

|

|

04-28-2018, 02:46 PM

|

#11

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2013

Posts: 1,561

|

OP Correction: The info I've included up to this point, is for a very small pension I wont be eligible for until age 60.

This is the big one that Ive been collecting since July 2015.

I upgraded the background to apologize for the error

__________________

"No beast so fierce but knows some touch of pity, but I know none, therefore am no beast"

Shown @ The End Of The Movie 'Runaway Train'

|

|

|

|

|

04-28-2018, 07:36 PM

|

#12

|

|

Full time employment: Posting here.

Join Date: May 2013

Posts: 756

|

Have a private company ($25B market cap) pension. Pension was frozen and not available for any new employees after 2004. Fund managed by high-end financial corp now.

2015 - Assets: 2.536B, Liabilities: 1.782B, "Funding Target Attainment Percentage": 139.48%

2016 - Assets: 2.367B, Liabilities: 1.826B, "Funding Target Attainment Percentage": 126.91%

2017 - Assets: 2.402B, Liabilities: 1.852B, "Funding Target Attainment Percentage": 126.84%

Will start taking early this year at age 58. Monthly payment (non-COLA) will be ~15% of monthly budget. Increase by waiting is less than 3%/yr, so taking early makes most sense.

__________________

Believe me, my young friend, there is nothing - absolutely nothing - half so much worth doing as simply messing about in boats. ― Kenneth Grahame, The Wind in the Willows

|

|

|

|

|

04-28-2018, 07:48 PM

|

#13

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2012

Posts: 11,702

|

Quote:

Originally Posted by RunningBum

I see the same trend, though your numbers are about 5-6% better than mine. Mine were further off in 2016 but not as big of a drop in 2017. Supposed to be a very blue chip company too. Big blue chip. It's not a big part of my retirement plan though.

|

A company of that stature wouldn't hose employees or retirees, right? I'm sure the executive suite would take a cut first and make sure the plan is funded.

</sarc>

* Full disclosure: I supposedly have "dinner for two per month" coming to me in about 10 years from same company. Dinner may consist of hamburger and fries.

|

|

|

|

|

04-28-2018, 09:03 PM

|

#14

|

|

Full time employment: Posting here.

Join Date: Sep 2016

Location: Way up North

Posts: 561

|

Reading this thread got me interested in checking up on the pension status at

my current mega-corp. The audit results from Jan 1, 2018 haven't been updated

yet. The boilerplate from my current employer's pension site:

The actuary for the XXX pension plans has completed the actuarial valuation for the XXX

Retirement Accumulation Plan as of January 1, 2017. For purposes of determining the

application of benefit restrictions under the 2006 Pension Protection Act, the funded

ratio of the plan as of January 1, 2017 is over 100%. This means there are no benefit

restrictions, including restrictions on the availability of lump sums, through September

1,2018. This is an annual process, and next years actuarial valuation will determine

whether benefit restrictions will apply after September 1, 2018.

Actuarial Value of Assets (as of January 1, 2017): $7,318 million

Funding Target (as of January 1, 2017): $5.806 million

Funding Ratio (as of January 1, 2017): 126.05%

I have worked my entire career for various evil big-oil megacorps. I was

bounced around a lot by plant closures, asset sales and getting personally p-o'ed.

I have vested in 4 different mega-corp pensions. I have lumped summed out

of 3 of them from previous employers. A couple of years ago there were rule

changes that incentivized pension buy-outs. I took 3 I was offered.

My current employer's pension is still active and is structured the best of any

I have been vested in. It is a cash balance plan rather than a defined benefit

plan. Plan rules say I can take a lump sum pay-out anytime after severance

up to age 70.5, as long as the funding ratio is greater than 80%. I'll retire in

2020, but intend to leave the pension balance in. It grows at the greater of

5% or the 30 year treasury rate. Should the annual audit fail the 80%

funded test, the lump sum option remains open for 8 months. If I select to

annuitize it, it will happen at whatever the prevailing rates are at the time of

the request. The balance is part of my estate until withdrawn or annuitized.

Pretty sweet deal in an era of greedy mega-corps

|

|

|

|

|

04-29-2018, 12:16 PM

|

#15

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2013

Posts: 1,561

|

Quote:

Originally Posted by FIREmenow

Have a private company ($25B market cap) pension. Pension was frozen and not available for any new employees after 2004. Fund managed by high-end financial corp now.

2015 - Assets: 2.536B, Liabilities: 1.782B, "Funding Target Attainment Percentage": 139.48%

2016 - Assets: 2.367B, Liabilities: 1.826B, "Funding Target Attainment Percentage": 126.91%

2017 - Assets: 2.402B, Liabilities: 1.852B, "Funding Target Attainment Percentage": 126.84%

Will start taking early this year at age 58. Monthly payment (non-COLA) will be ~15% of monthly budget. Increase by waiting is less than 3%/yr, so taking early makes most sense.

|

Looks like you're set!

__________________

"No beast so fierce but knows some touch of pity, but I know none, therefore am no beast"

Shown @ The End Of The Movie 'Runaway Train'

|

|

|

|

|

04-29-2018, 12:22 PM

|

#16

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2013

Posts: 1,561

|

Quote:

Originally Posted by JoeWras

A company of that stature wouldn't hose employees or retirees, right? I'm sure the executive suite would take a cut first and make sure the plan is funded.

|

Of course not. If they did that, they wouldn't be able to fund the outrageously lavish golden parachutes given to execs when they fail

__________________

"No beast so fierce but knows some touch of pity, but I know none, therefore am no beast"

Shown @ The End Of The Movie 'Runaway Train'

|

|

|

|

|

04-29-2018, 12:22 PM

|

#17

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2013

Posts: 1,561

|

Quote:

Originally Posted by bada bing

Reading this thread got me interested in checking up on the pension status at

my current mega-corp. The audit results from Jan 1, 2018 haven't been updated

yet. The boilerplate from my current employer's pension site:

The actuary for the XXX pension plans has completed the actuarial valuation for the XXX

Retirement Accumulation Plan as of January 1, 2017. For purposes of determining the

application of benefit restrictions under the 2006 Pension Protection Act, the funded

ratio of the plan as of January 1, 2017 is over 100%. This means there are no benefit

restrictions, including restrictions on the availability of lump sums, through September

1,2018. This is an annual process, and next years actuarial valuation will determine

whether benefit restrictions will apply after September 1, 2018.

Actuarial Value of Assets (as of January 1, 2017): $7,318 million

Funding Target (as of January 1, 2017): $5.806 million

Funding Ratio (as of January 1, 2017): 126.05%

I have worked my entire career for various evil big-oil megacorps. I was

bounced around a lot by plant closures, asset sales and getting personally p-o'ed.

I have vested in 4 different mega-corp pensions. I have lumped summed out

of 3 of them from previous employers. A couple of years ago there were rule

changes that incentivized pension buy-outs. I took 3 I was offered.

My current employer's pension is still active and is structured the best of any

I have been vested in. It is a cash balance plan rather than a defined benefit

plan. Plan rules say I can take a lump sum pay-out anytime after severance

up to age 70.5, as long as the funding ratio is greater than 80%. I'll retire in

2020, but intend to leave the pension balance in. It grows at the greater of

5% or the 30 year treasury rate. Should the annual audit fail the 80%

funded test, the lump sum option remains open for 8 months. If I select to

annuitize it, it will happen at whatever the prevailing rates are at the time of

the request. The balance is part of my estate until withdrawn or annuitized.

Pretty sweet deal in an era of greedy mega-corps |

Very interesting

__________________

"No beast so fierce but knows some touch of pity, but I know none, therefore am no beast"

Shown @ The End Of The Movie 'Runaway Train'

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|