corn18

Thinks s/he gets paid by the post

- Joined

- Aug 30, 2015

- Messages

- 1,890

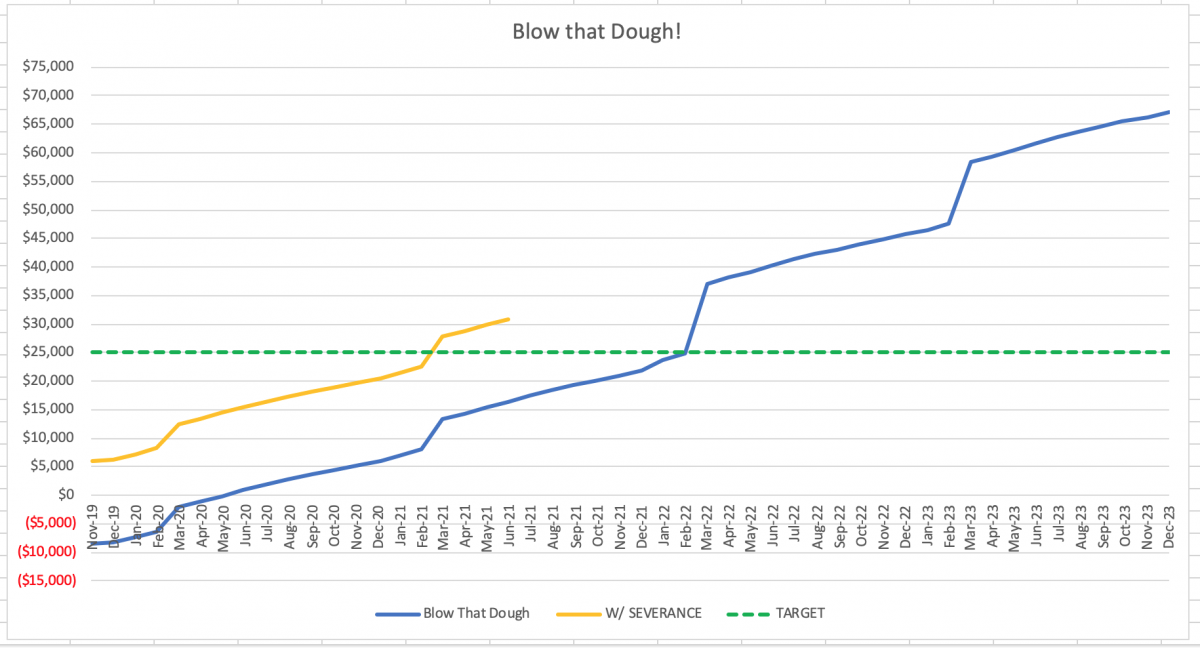

This was an unusual year for us for income due to a merger and change in control clauses (RSU's vesting, bonuses early). We managed to save enough to pay off our mortgage, but let it sit in a MM for a couple of months while we examined our options. After much analysis and then a bit of emotion, we wired $572,838.49 to our mortgage bank today and I just verified with them that it hit the account and our mortgage balance is zero. The PI payment will go into our taxable account and our 60/40 AA.

This is very surreal for us as 6 years ago we we had a net worth of zero and were spending way more than we made. Then we read The Millionaire Next Door and fixed our spending. Now we have $1M in retirement savings and a paid off house. And a good shot at retiring in 2 years @ 56.

Life is good!

Tom

This is very surreal for us as 6 years ago we we had a net worth of zero and were spending way more than we made. Then we read The Millionaire Next Door and fixed our spending. Now we have $1M in retirement savings and a paid off house. And a good shot at retiring in 2 years @ 56.

Life is good!

Tom

") ) and 100% joint survivable. Ergo, our plan is to obtain a loan that this pension will cover. The loan, and the proceeds from selling our current digs will be our means to an end. In all likely hood, we'll both assume room temps while that mortgage is still in amortization. Our equity should more that settle that "affair." If not, tuff sh!t, we're busy being dead.

) and 100% joint survivable. Ergo, our plan is to obtain a loan that this pension will cover. The loan, and the proceeds from selling our current digs will be our means to an end. In all likely hood, we'll both assume room temps while that mortgage is still in amortization. Our equity should more that settle that "affair." If not, tuff sh!t, we're busy being dead.