We're on the wrong side of the asset allocation equation compared to everyone here. The only thing that helps is having a large enough nest egg to where it may not matter. DW (67) SS plus my (61) pension is almost enough to cover all expenses. WR is less than 0.5% and may become even less (or 0%) when I start SS for myself (combination of more income plus lower medical premiums @65 - my under 65 medical plan is costly).

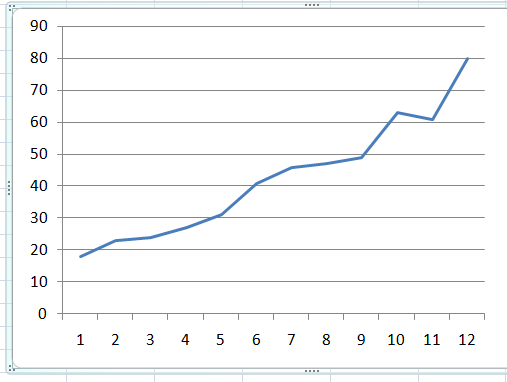

Below is a plot of my RMD's

Below is a plot of my RMD's