Midpack

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

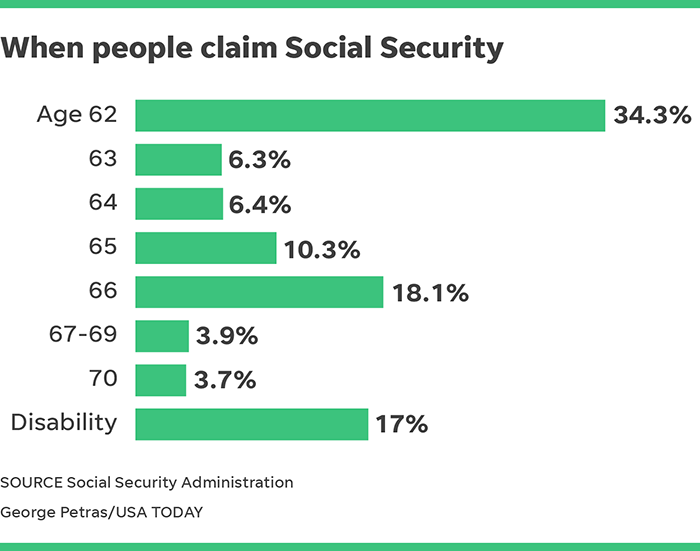

I’m just guessing this group will poll differently than the mainstream, though there are perfectly legit reasons to start early or late regardless. I’m not asking for anyone to explain, just curious how an ER.org poll pans out.

Last edited:

Whining is fun if you don't take yourself too seriously.

Whining is fun if you don't take yourself too seriously.