Quote:

Quote:

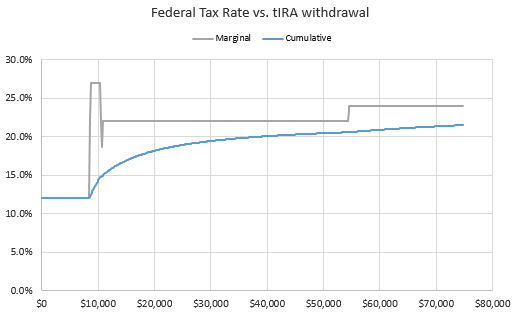

Originally Posted by Gotadimple

5. What will your retiree health plans cover after age 65? How does that cost compare to the cost of Medicare Part B? Part B + Medicare Supplement/Medicare Advantage Plan

6. What is the IRMAA limit for you as respects your Medicare Part B premium?

- Rita

|

IRMAA is pretty straight forward, for Married filing jointly it is based on your MAGI from federal taxes. Expressed below is extracted from a SSA letter after enrolling DW about 2 months ago. IRMAA is a monthly figure.

MAGI - PART B IRMAA - Part D IRMAA

Less than $170K - 0 - 0

$170K to 214K- $53.50 - $13.00

$214K to $267K - $133.90 - $33.60

$267K to $320K - $214.30 - $54.20

Over $320K - $294.00 - $74.80

Another poster can address the Modified part of Adjusted Gross Income. SSA referred to numbers on line 37 of my 1040, bottom of first page before any deductions.

Linear Mode

Linear Mode