NW-Bound

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Jul 3, 2008

- Messages

- 35,712

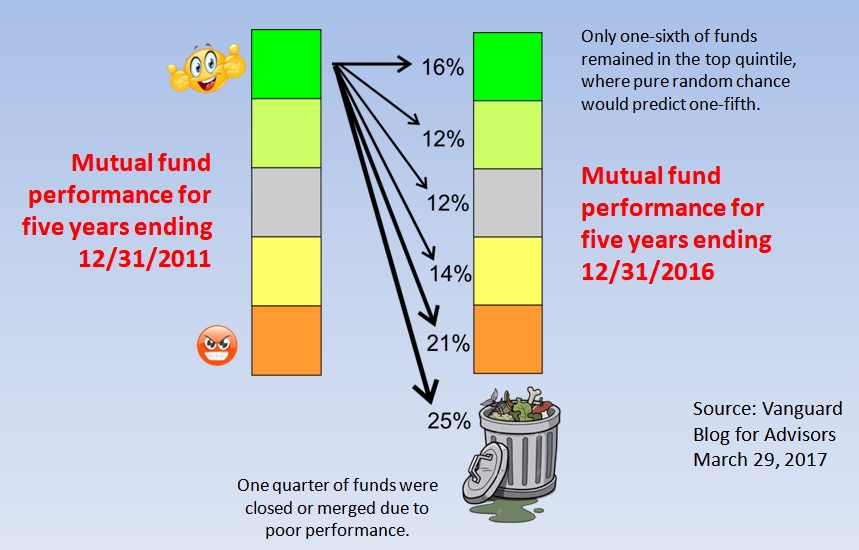

I just saw this article in Yahoo Finance Web site, which said that while the S&P 500 is down -11.31% from 11/01/2021 to 04/12/2023, retail investors are down -27.49%. Wowzah!

Who are these retail investors? Anyway, that's the number quoted from VandaTrack Research.

See article here: https://finance.yahoo.com/news/reta...ses-despite-a-2023-stock-rally-134826847.html

What do these retail investors do to lose so much? Buy high/sell low obviously.

Out of curiosity, I computed my own number for 11/01/2021 to 04/12/2023: -2.474%.

I feel so much better now.

Who are these retail investors? Anyway, that's the number quoted from VandaTrack Research.

See article here: https://finance.yahoo.com/news/reta...ses-despite-a-2023-stock-rally-134826847.html

What do these retail investors do to lose so much? Buy high/sell low obviously.

Out of curiosity, I computed my own number for 11/01/2021 to 04/12/2023: -2.474%.

I feel so much better now.