|

|

12-15-2019, 10:35 PM

12-15-2019, 10:35 PM

|

#301

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote: Quote:

Originally Posted by target2019

This may be of interest for the thread topic, or at least half of the topic.

https://www.doughroller.net/financia...om-mark-zoril/

I did not find a mention of this in the thread. The link came from B-Heads.

The first year cost is a bit higher than $96 now, but still afoordable. But I don't think the service fills the income optimization part of the thread topic.

I thought the discussion revealed some insight about paid FPs. |

I actually signed up for it. Mostly because I was curious about eMoney software and how different is it from Income Strategy. In a nutshell: not very. And the way this service is structured you don't get the access to all the features. It's designed for less financial savvy ppl than most of you guys here.

They basically ask you to fill in all the info and and then they have the video sessions: first, to clarify the details and second - which I haven't had yet - with the planner. You get all the reports after that and and can tweak the inputs later. I don't have a fully formed opinion about it (someone else does: https://www.bogleheads.org/forum/viewtopic.php?t=282215) but I think it will work as a possible replacement of that $125/hr call to Income Strategy guys - which I don't think I need.

What I like about these guys is not just the personal touch but kind of a non-nonsense approach which I subscribe to. They have a short article about the virtues of taking SS early where they remind us that while it might be less money monthly - or even overall, the fun we can have with it at 62 shouldn't be compared to the fun we are able to have at 70 or 80. I strongly believe in that philosophy: so I'm interested in the one-on-one session.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

12-16-2019, 05:53 AM

|

#302

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2007

Posts: 1,214

|

Quote:

Originally Posted by tenant13

They have a short article about the virtues of taking SS early where they remind us that while it might be less money monthly - or even overall, the fun we can have with it at 62 shouldn't be compared to the fun we are able to have at 70 or 80. I strongly believe in that philosophy: so I'm interested in the one-on-one session.

|

Finally! Finally a financial planner that looks at the lifestyle aspects of when to take SS and not just the numbers written on paper without regard to the timing of those numbers.

|

|

|

|

|

12-16-2019, 06:57 AM

|

#303

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2015

Posts: 1,890

|

Quote:

Originally Posted by rayvt

Finally! Finally a financial planner that looks at the lifestyle aspects of when to take SS and not just the numbers written on paper without regard to the timing of those numbers.

|

The only way this works is if you don't need SS to cover your base budget. You could use SS as a big blow that dough budget.

__________________

Consistently sets low goals and fails to achieve them.

|

|

|

|

|

12-16-2019, 07:09 AM

|

#304

|

|

Full time employment: Posting here.

Join Date: Jun 2016

Posts: 889

|

All of this "optimization" discussion is good, but people need to remember: Don't let the tax tail wag the investment dog, and that generally when you have to pay more taxes it means you have been successful. Don't lose site of that while one optimizes their tax situation.

|

|

|

|

|

12-16-2019, 07:24 AM

|

#305

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,227

|

Quote:

Originally Posted by corn18

The only way this works is if you don't need SS to cover your base budget. You could use SS as a big blow that dough budget.

|

Or I can spend down more of my own money and enjoy things just as much at age 62, knowing I'll have a larger SS benefit the longer I wait.

|

|

|

|

|

12-16-2019, 07:34 AM

|

#306

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by rayvt

Finally! Finally a financial planner that looks at the lifestyle aspects of when to take SS and not just the numbers written on paper without regard to the timing of those numbers.

|

I really like this thread and how informative it is but it should be read alongside another one from this forum where people describe their well being and attitude after retirement. And when you read it, you realize that some of the financial optimization we discuss here becomes irrelevant if the money we save ends up having very limited use. One could argue that you might as well use it for paying taxes. That's why, when I look at ROTH conversions and such I use common sense: as long as the projections tell me I'll hit my budgets in my later years, I don't obsess about future taxes. I'd rather spend my savings now on travel and activities that I can enjoy at 56 yrs old rather than paying large tax bills for converting IRAs and sitting on a larger pile of cash at 80. It's not that I am ignoring the numbers - I'll definitely convert some - just not as aggressively as the software alone would have me to.

|

|

|

|

|

12-16-2019, 07:53 AM

|

#307

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,145

|

I think that’s a good point.

__________________

Retired since summer 1999.

|

|

|

|

12-16-2019, 08:02 AM

|

#308

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2008

Location: NC

Posts: 21,303

|

Quote:

Originally Posted by tenant13

I really like this thread and how informative it is but it should be read alongside another one from this forum where people describe their well being and attitude after retirement. And when you read it, you realize that some of the financial optimization we discuss here becomes irrelevant if the money we save ends up having very limited use. One could argue that you might as well use it for paying taxes. That's why, when I look at ROTH conversions and such I use common sense: as long as the projections tell me I'll hit my budgets in my later years, I don't obsess about future taxes. I'd rather spend my savings now on travel and activities that I can enjoy at 56 yrs old rather than paying large tax bills for converting IRAs and sitting on a larger pile of cash at 80. It's not that I am ignoring the numbers - I'll definitely convert some - just not as aggressively as the software alone would have me to.

|

It’s certainly good to keep some perspective, but there is simply no way to know that, especially for the many here who have 20-40 years to go. Also a key consideration. You can only know the probability based on past US history, admittedly better than nothing but no guarantee.

We all have to choose where we think the balance is between quality of life today and how the unknowns will play out over the next 20-40 years. The future could be better than expected, or it could be markedly worse - geopolitics and other factors (AI, who knows?) can completely override past market return-inflation-growth-employment history. Who knows what future tax rates will be. Or you could live much longer than planned...

But I come to the same conclusion a different way. I’m converting to 22%, even though converting to 24% would be less in taxes and a slightly higher ending balance based on what we know today (not much, mostly best guesses).

__________________

No one agrees with other people's opinions; they merely agree with their own opinions -- expressed by somebody else. Sydney Tremayne

Retired Jun 2011 at age 57

Target AA: 50% equity funds / 45% bonds / 5% cash

Target WR: Approx 1.5% Approx 20% SI (secure income, SS only)

|

|

|

|

|

12-16-2019, 08:57 AM

|

#309

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2015

Posts: 1,890

|

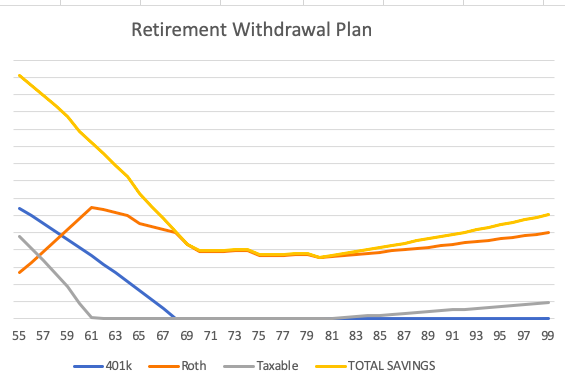

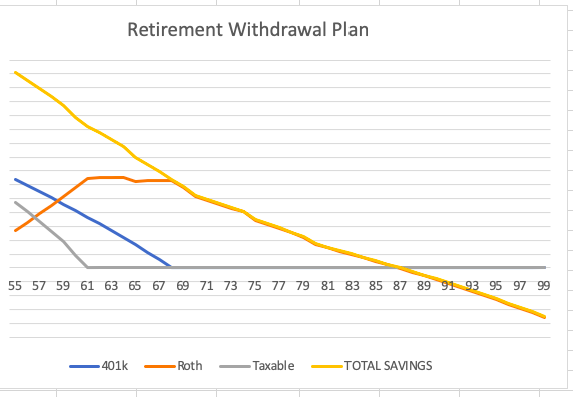

I dunno, just like we plan a lot when we are accumulating, I think it's good to plan the withdrawal phase as well.

I'll take this (ss @ 70):

Over this (SS @ 62 or no Roth conversions):

__________________

Consistently sets low goals and fails to achieve them.

|

|

|

|

|

12-16-2019, 09:47 AM

|

#310

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2006

Location: Denver

Posts: 3,519

|

The thinking and planning is good for keeping your mind sharp  Also, I think a lot of us here like doing this kind of analytical problem solving. If it ends up working for us - all the better.

Tennant13 - Please keep us informed of your journey with Planvision.

|

|

|

|

|

12-16-2019, 11:01 AM

|

#311

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,227

|

Another thing to consider is that you can't directly spend from 401K/tIRA/other tax deferred accounts. You must first convert or withdraw that money. So while you may think that paying more taxes upfront will cut into your spending, it's actually making more money available for you to spend. This takes some advance planning if you are converting to a Roth because of the 59.5 age restriction and 5 year rule so it may not work for everyone, but you really need to go into more depth than just dismissing it because you don't want to pay more taxes now. Think of paying those conversion taxes as unlocking the tax deferred money and making it available to spend.

|

|

|

|

|

12-16-2019, 11:36 AM

|

#312

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2015

Posts: 1,890

|

Quote:

Originally Posted by RunningBum

Another thing to consider is that you can't directly spend from 401K/tIRA/other tax deferred accounts. You must first convert or withdraw that money. So while you may think that paying more taxes upfront will cut into your spending, it's actually making more money available for you to spend. This takes some advance planning if you are converting to a Roth because of the 59.5 age restriction and 5 year rule so it may not work for everyone, but you really need to go into more depth than just dismissing it because you don't want to pay more taxes now. Think of paying those conversion taxes as unlocking the tax deferred money and making it available to spend.

|

In addition to all of that, the growth after conversion is now tax free. Over a 30 year retirement, that can add up to a lot of tax free money.

__________________

Consistently sets low goals and fails to achieve them.

|

|

|

|

|

12-16-2019, 12:40 PM

|

#313

|

|

Full time employment: Posting here.

Join Date: Oct 2007

Posts: 621

|

eg

Quote:

Originally Posted by walkinwood

The thinking and planning is good for keeping your mind sharp Also, I think a lot of us here like doing this kind of analytical problem solving. If it ends up working for us - all the better.

Tennant13 - Please keep us informed of your journey with Planvision. |

I just got out of PlanVision after a year of use, when I found he was of no help in projecting my income & taxes. He found it strange that I would pay money up front to Roth convert hoping for a larger pile of tax free money later.

Your miles may vary, maybe my case was different but I did not find the software much help to me. Emoney software I use, is from the Fidelity Retirement Planner which anyone can get to free of cost with a guest registration.

Rightcapital ($150 one time) is OK but I have not been able to figure out where it is getting its figures of taxable income in its tax projections. I am still learning it by seeing its videos on Youtube.

Not all but some of these software (even paid ) eg New Reirement share your money info & you keep getting bombarded by Credit Card offers & such solicitations. So buyer be aware.

Good Luck

|

|

|

|

|

12-16-2019, 10:45 PM

|

#314

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by RunningBum

Another thing to consider is that you can't directly spend from 401K/tIRA/other tax deferred accounts. You must first convert or withdraw that money. So while you may think that paying more taxes upfront will cut into your spending, it's actually making more money available for you to spend. This takes some advance planning if you are converting to a Roth because of the 59.5 age restriction and 5 year rule so it may not work for everyone, but you really need to go into more depth than just dismissing it because you don't want to pay more taxes now. Think of paying those conversion taxes as unlocking the tax deferred money and making it available to spend.

|

I'm taking all this into consideration and will absolutely do some conversions (or at least capital gain harvesting in my brokerage) - but I feel that a lot decisions I'll make in retirement cannot be pre-planned and they might be influenced by non-financial factors. If I get diagnosed with some some unpleasant disease between now and 62, there won't be much point in waiting until 70 for SS, right? It's all just a big guessing game that we play by own rules.

|

|

|

|

|

12-16-2019, 10:57 PM

|

#315

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by rkser

eg

I just got out of PlanVision after a year of use, when I found he was of no help in projecting my income & taxes. He found it strange that I would pay money up front to Roth convert hoping for a larger pile of tax free money later.

Rightcapital ($150 one time) is OK but I have not been able to figure out where it is getting its figures of taxable income in its tax projections. I am still learning it by seeing its videos on Youtube.

Good Luck

|

So far the best and most helpful source of information for income optimization is this thread and a few posts on bogleheads. My personal experiences with financial advisors are quite bad so I don't expect miracles from PlanVision but I'd be fine with hearing someone else's point of view on how to plan my financial future. Even if I disagree. Income Strategy is quite great and worth $20/month to me - at least for a while - although as everyone mentioned interface could be a bit better. I think that I'll go ahead and get on the Right Capital bandwagon eventually but for now I'm still trying to figure out broad strokes.

|

|

|

|

|

12-17-2019, 06:28 AM

|

#316

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2007

Posts: 1,214

|

I think this is mostly an exercise in futility. No matter how clever your software is, it won't be able to come up with a strategy to put 10 pounds of potatoes into a 5 pound bag. The best it can do is help you put 4.9999 pounds instead of 4.95.

The IRS has a claim on X% of the money in your IRA/401K. And the richer you are, the stronger their claim and the larger X is going to be.

The deeper I get in retirement, the more I realize that all that I was doing was just shuffling money around, and changing the timing of *when* I paid the taxes.

The biggest tax-related thing is when one spouse of a married couple dies and the survivor gets shifted to the Single Filing Status. That shifts the start of the 22% rate from $79K to $40K, thus exposing up to $39K that will be taxed at 22% instead of 12%. That's another $3900 in tax.

That's the main reason to do Roth conversions. And none of the clever software in the world can do anything about that.

The main benefit of these software products is to advise you not to do stupid stuff. Okay. But you can figure that out for free.

|

|

|

|

|

12-17-2019, 06:35 AM

|

#317

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,227

|

Quote:

Originally Posted by tenant13

I'm taking all this into consideration and will absolutely do some conversions (or at least capital gain harvesting in my brokerage) - but I feel that a lot decisions I'll make in retirement cannot be pre-planned and they might be influenced by non-financial factors. If I get diagnosed with some some unpleasant disease between now and 62, there won't be much point in waiting until 70 for SS, right? It's all just a big guessing game that we play by own rules.

|

Of course you'd take SS early if you have some life-shortening illness. (That's a financial decision, by the way). But if you don't have such a disease, are you still going to take SS early, just in case? Why? And wouldn't that be pre-planning?

I have a different take on the unknown future. First, I'm going to spend money in my early years just the same as I would if I took SS early and didn't pay any conversion taxes. If I die early, not taking SS and paying out those taxes are going to be the least of my regrets on my death bed. But what if I outlive my life expectancy? That's where waiting on a larger SS benefit and optimizing my tax situation wrt Roth conversions and minimizing/avoiding RMDs will be appreciated every day of my long life.

|

|

|

|

|

12-17-2019, 06:51 AM

|

#318

|

|

Full time employment: Posting here.

Join Date: Nov 2019

Location: Jersey City

Posts: 522

|

Quote:

Originally Posted by RunningBum

Of course you'd take SS early if you have some life-shortening illness. (That's a financial decision, by the way). But if you don't have such a disease, are you still going to take SS early, just in case? Why? And wouldn't that be pre-planning?

I have a different take on the unknown future. First, I'm going to spend money in my early years just the same as I would if I took SS early and didn't pay any conversion taxes. If I die early, not taking SS and paying out those taxes are going to be the least of my regrets on my death bed. But what if I outlive my life expectancy? That's where waiting on a larger SS benefit and optimizing my tax situation wrt Roth conversions and minimizing/avoiding RMDs will be appreciated every day of my long life.

|

I actually think pretty much along the same lines: if I live comfortably and within my budget without taking SS, then - provided that health is not a factor - I may wait until 70. I'll think of it as a supplemental health/LTC insurance policy. But I'm ready to change my mind if for example I decide to become a resident of Panama at 62 and need a proof of steady monthly income.

|

|

|

|

|

12-17-2019, 07:00 AM

|

#319

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,370

|

Quote:

Originally Posted by tenant13

.... What I like about these guys is not just the personal touch but kind of a non-nonsense approach which I subscribe to. They have a short article about the virtues of taking SS early where they remind us that while it might be less money monthly - or even overall, the fun we can have with it at 62 shouldn't be compared to the fun we are able to have at 70 or 80. I strongly believe in that philosophy: so I'm interested in the one-on-one session.

|

Unfortunately, that's a false narrative if done right. Spending can be the same taking at 62 or at 70, it's just a matter of the sources of the funding... remember, money is fungible.

Quote:

Originally Posted by RunningBum

Or I can spend down more of my own money and enjoy things just as much at age 62, knowing I'll have a larger SS benefit the longer I wait.

|

Exactly.... why is this simple concept so hard for people to understand?

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-17-2019, 07:25 AM

|

#320

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,370

|

Quote:

Originally Posted by corn18

In addition to all of that, the growth after conversion is now tax free. Over a 30 year retirement, that can add up to a lot of tax free money.

|

Another false narrative or common misconception.... it is all about tax rates if you pay for taxes from the tIRA with a minor benefit if you pay taxes with after-tax funds.

Example: $10k in tIRA, $2k in taxable funds, 20% tax rate, 7% return, 30 years

Do nothing: $10k tIRA grows to $76,123, $2k grows to $10,255 after 30 years... withdraw $76,123 and pay $15,225 in taxes... leaving $71,153 to spend.

Roth conversion and pay taxes from Roth: $8k in Roth grows to $60,898 and taxable account grows to $10,255... leaving $71,153 to spend

Roth conversion and pay taxes from taxable account: $10k in tIRA grows to $76,123

So at most, the benefit of conversion if tax rates are the same is not having to pay tax on the taxable funds for 30 years... benefit is $76,123 - $71,153 or $4,970 (7%)..... the difference between the growth of $2k with no taxes ($2,000*(1+7%)^30) and the growth of $2k with taxes ($2,000*(1+(7%*(1-20%)))^30).

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode