googily

Full time employment: Posting here.

- Joined

- Jul 6, 2013

- Messages

- 792

Midpack, what does your modeling show in terms of conversions if you become single on the near future? Would you continue conversions?

Good suggestion. I’ll run a couple scenarios with one of us becoming single with and without a Roth conversions.Midpack, what does your modeling show in terms of conversions if you become single on the near future? Would you continue conversions?

If you’re asking me, there are 5-6 tax options including 2017 inflation adjusted, TCJA then 2017 rates starting in 2026, rising rates, worst case and a couple others. I’ve been using TCJA>2017 even though I don’t think it’s realistic, rates will get worse. I just started studying the others last night. But as far as I can see, the user can’t makeup their own custom future tax scheme.Does the modeling advance the tax brackets by some adjustable amount, or is the assumption that all future dollars will be compensated for equally so everything is in todays dollars?

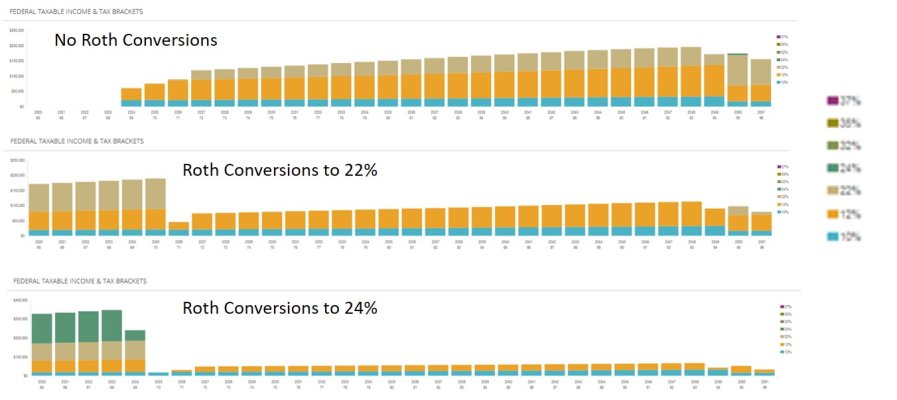

I didn’t delve into exactly why but 32% was trivially worse than 24%. The software doesn’t seem to optimize, it just brute force fills to the top of the bracket each year until your fully converted. So it converted faster than necessary when I specified 32%. Not ideal? But you can somewhat optimize by trying each bracket given the years to 70, as I did. In practice if I proceed I’ll convert to complete at age 70, the equivalent of a few months slower than the software shows for 24%, the best brute force option for our situation.Midpack, you said "I modeled converting to 12%, 22%, 24% and 32%, each was progressively better than no conversions. But there was no additional in 32%...". Was converting to fill 32% bracket any worse than filling 24% or just no additional benefit ? I had an adviser recommend total conversion in one year no matter how high the tax bracket, as long as paying tax from non IRA account. I would love to be totally out from the tax overhang by converting past the 24% bracket, but right capital software modeling stops at the 24% bracket.

")

I may not have explained it well, but while 24% is the numeric optimum for me, I will probably convert to 22%. Though total lifetime taxes are significantly lower, they're just too high to stomach while I am converting, and the portfolio total value (the overriding objective) difference is almost trivial. YMMVMidpack, thank you for taking the time to give such a detailed response on the 1 hour session you had. The more I read the more I feel it best to fill the 24% bracket at a minimum. I believe fed tax rates have nowhere to go but up after 2025, and I like preventing the widow's tax trap if something were to happen to me. I say this with the usual caveat that each person's situation is different, and I am speculating on future tax rates.

Thanks for asking. I wasn't sure (and my earlier guess was wrong) so I went back and added Roth conversions to 22% (vs 24%). To my surprise the lifetime savings were only 9% vs 31%, and the "breakeven" age was about the same. Doesn't make our decision any easier. It appears we either convert aggressively or not at all, not quite what I was guessing - but I have my consult later this week, so we'll see if I'm missing something. If nothing else, it appears I've gotten more than our money's worth on our $20 one month subscription. Who knows, I may continue it for more than a month, or even try their $50 premier version.

And like RunningBum, the tax situation we leave heirs isn't a top priority for us, though it's probably a very legit consideration for many households.

I see this kind of statement now and then on this board, and I never understand that attitude. I understand you'll be grateful if you live past 85. But won't you be even more grateful if you make it past 85, AND took easy steps in your finances now to live a little more comfortably later?But I can't get excited about saving 3% per year after I turn 85. H@ll, I"ll be grateful I lived that long.

If you think of the taxes voluntarily paid early as an investment, it will make more sense I think.I see this kind of statement now and then on this board, and I never understand that attitude. I understand you'll be grateful if you live past 85. But won't you be even more grateful if you make it past 85, AND took easy steps in your finances now to live a little more comfortably later?

Now we back to debating whether the conversion breakeven point is a meaningful thing, and I don't want to go there again.If you think of the taxes voluntarily paid early as an investment, it will make more sense I think.

Stated differently, would you buy the investment called "taxes paid in advance" or TPIA that will take most or all of your remaining life to generate a return, if at all? ?Or would you find other investments to be more lucrative?

I am not trying to convince you one way or the other, (I do not fully know the answer for me) I just think the long time horizon involved does materially impact the decision.

I see this kind of statement now and then on this board, and I never understand that attitude. I understand you'll be grateful if you live past 85. But won't you be even more grateful if you make it past 85, AND took easy steps in your finances now to live a little more comfortably later?

It was just an offhand observation. Not terribly meaningful and never intended to start in a discussion. FWIWI know you don't want to discuss the break-even point, but for OP, with no concern about heirs, isn't it the ONLY thing to look at?