That’s a reasonable assessment. It’s the same ballpark, but better seats. I’m simply repeating what I’ve read many times. Here’s an example excerpt albeit’s 6 yrs old.....

So how do MYGs and bank CDs stack up against each other? To start, let's acknowledge the conventional wisdom holding that MYGs are generally the better choice because they offer higher rates and certain tax advantages. But is that the final verdict?

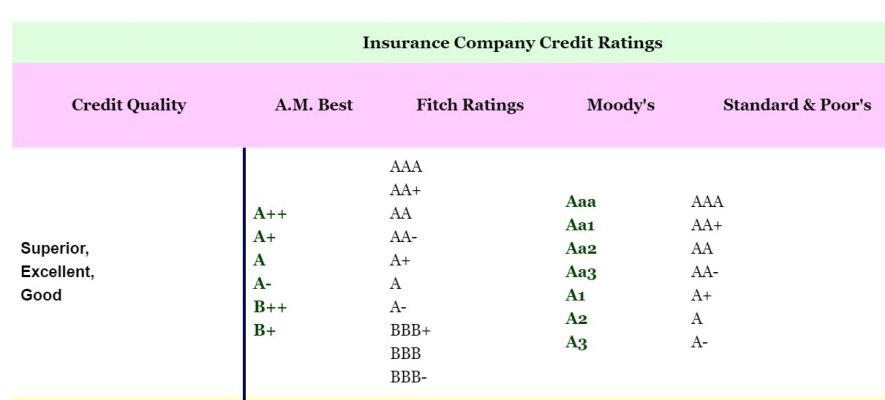

The entire article which favors CDs due to simplicity of the product is below. It discusses the MYGA tax deferral which seems significant to me but I’m not sure I trust their analysis....

https://www.marketwatch.com/story/comparing-cds-and-annuities-for-savers-2014-03-28

")