Question, if your plan offers it, wouldn't a rollover from a Roth 401k make more sense? Iirc, if you have both pre-tax and after tax dollars in your regular 401k, I think the amount you wish to rollover gets pro-rated between your pre-tax and after tax dollars. Roth 401k gets treated as a separate account so you can rollover just after tax dollars (and earnings).

Also, money rolled over from Roth 401k gets treated the same as Roth IRA rollover just without carry over of account age for 5-year vesting in case the Roth 401k is older than the Roth IRA. On the flip side, if you've had the Roth IRA for 6 years and the Roth 401k for just 1 year, the 6 years you've had the Roth IRA satisfies the 5-year requirement for distribution on rolled over Roth 401k funds.

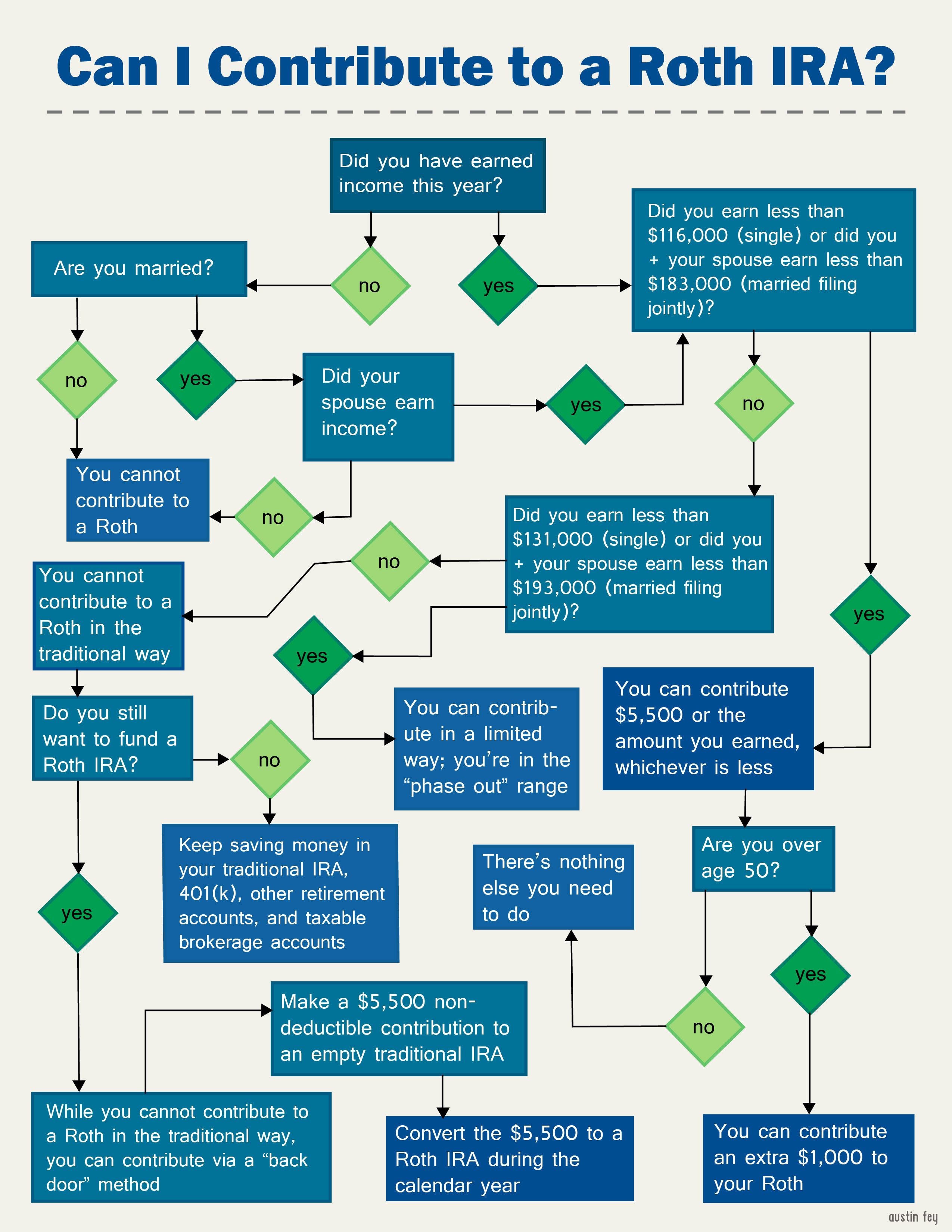

") whenever people mention doing a backdoor ROTH. Given that there are probably more people than usual who might have a number of retirement account-types (for self-employed work or various business ventures), the odds that they might have other accounts that they have to pro-rate their after-tax balances are higher than the population as a whole. And if you have any accounts that require you to pro-rate the amount, the value of doing a backdoor ROTH dwindles quickly.

whenever people mention doing a backdoor ROTH. Given that there are probably more people than usual who might have a number of retirement account-types (for self-employed work or various business ventures), the odds that they might have other accounts that they have to pro-rate their after-tax balances are higher than the population as a whole. And if you have any accounts that require you to pro-rate the amount, the value of doing a backdoor ROTH dwindles quickly.