donheff

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Hello engineers and financial math gurus. I am having a hard time wrapping my head around a Roth conversion optimization analysis and need help. This is a long, confused post, so don't bother with it unless you enjoy sorting out these kinds of issues.

In the past I ignored Roth conversions because I had the vague impression that they were only beneficial if you could take advantage of low tax brackets when you make the conversion and/or higher brackets later when the funds come out. I ran a few TurboTax scenarios using simplistic assumptions of equal tax levels now and later and they came out with it being largely a wash. Intuitively, that makes sense. So I went back to sleep.

Recent posts here by people taking advantage of higher brackets for conversions and the impact of the Secure Act on RMDs of inherited IRAs led me to take a second look. I began to conclude that large conversions might be a good thing. That drew my attention to a change in DC’s estate tax that complicates everything and makes conversions more compelling.

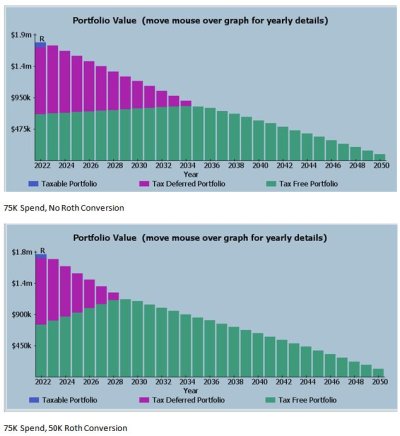

DC recently dropped it’s estate tax limit to levels DW and I are about to bump against. The tax is 16% of assets above the estate limit (so $160K for each $1M over the limit). And, unlike the Federal estate tax, in DC the kids inheriting the IRA pay the full state income tax on the IRA with no deduction for the DC estate tax already paid. Also, the DC exclusion amount is not portable to the surviving spouse like it is at the Federal level. The first to die needs to get their exclusion out of the estate or it is lost. DW and I can deal with that by moving some assets like the house and joint taxable brokerage accounts into a disclaimer trust when the first of us dies. The rest could be excluded by disclaiming sufficient IRAs to reach the DC disclaimer amount and passing them directly to the kids. But that adds to the attractiveness of Roths since conversions drop the size of the estate in general (reducing the amount that exceeds the limit) and our kids are in high tax brackets so inherited Roths would be much better than tIRAs.

I have seen some online calculators that seem to confirm that even large conversions will be ok at long as the tax rates at the end period are close to the rates at conversion. These calculators all assume that the taxes are paid from outside the tIRA but, in our case, I would deduct Fed and State taxes directly from the tIRAs. My taxable funds all have capital gains of about 60% so I don’t want to sell them to pay the tax. And those funds are not sufficient to cover the conversions anyway. Still, the value equivalence seems to roughly hold when paying the tax from the IRA funds. If I have two $1M tIRAs and convert one to a Roth paying $300k in tax, I have a $700K Roth and a $1M tIRA. If I die tomorrow and cash out both, they are worth the same $700k each after tax. If I leave them both in the account to appreciate at the same rate, they will remain equivalent over time, provided the tax rates are the same when they come out. There are lots of things that can happen to change outcomes but the underlying equivalence if the tax rates stay the same seems intuitive.

If the above is fair, it seems that, if I am correct that my heirs’ income tax rates will be the same or higher when the IRAs are inherited, converting as much as possible would make sense, regardless of bracket. The outcome should be a wash or, hopefully, better since the smaller estate size would reduce the DC estate tax. If, in fact, their income tax rates turn out to be significantly lower they could lose out. Does this sound about right, or am I missing something obvious?

.

I don’t want to lay my financials out in detail, but suffice it to say that DW and I are currently right at the beginning of the 24% Federal tax bracket and will remain there for three years at which point large RMDs will kick in. The RMDs will fill the 24% bracket and spill over a bit into the 32% bracket. Over time, with good market growth, the RMDs could eventually kick us right up toward the top. The amounts we are interested in converting far exceed the room available in lower than 37% brackets over the first three years. Assuming we want to wrest the most out of the lower brackets it seems like we should fill them, but what about more? If we need another $2M to help with DC estate tax, should we just bite the bullet and convert a large part of that in year 1 at 37%? Is there a substantial down side to that that I am missing?

I can’t quite wrap my head around this. Is it reasonable to think of all conversions as a wash if you and your heirs will be at high brackets? Does that make a conversion into 37% neutral? If so, the potential advantages to offset DC estate taxes make it attractive. But I fear I am missing something that would make those large immediate conversions less than a wash. I will consult with a CPA and maybe an FA before doing anything but I would like to noodle this around first.

First world problem isn't it? Thoughts?

In the past I ignored Roth conversions because I had the vague impression that they were only beneficial if you could take advantage of low tax brackets when you make the conversion and/or higher brackets later when the funds come out. I ran a few TurboTax scenarios using simplistic assumptions of equal tax levels now and later and they came out with it being largely a wash. Intuitively, that makes sense. So I went back to sleep.

Recent posts here by people taking advantage of higher brackets for conversions and the impact of the Secure Act on RMDs of inherited IRAs led me to take a second look. I began to conclude that large conversions might be a good thing. That drew my attention to a change in DC’s estate tax that complicates everything and makes conversions more compelling.

DC recently dropped it’s estate tax limit to levels DW and I are about to bump against. The tax is 16% of assets above the estate limit (so $160K for each $1M over the limit). And, unlike the Federal estate tax, in DC the kids inheriting the IRA pay the full state income tax on the IRA with no deduction for the DC estate tax already paid. Also, the DC exclusion amount is not portable to the surviving spouse like it is at the Federal level. The first to die needs to get their exclusion out of the estate or it is lost. DW and I can deal with that by moving some assets like the house and joint taxable brokerage accounts into a disclaimer trust when the first of us dies. The rest could be excluded by disclaiming sufficient IRAs to reach the DC disclaimer amount and passing them directly to the kids. But that adds to the attractiveness of Roths since conversions drop the size of the estate in general (reducing the amount that exceeds the limit) and our kids are in high tax brackets so inherited Roths would be much better than tIRAs.

I have seen some online calculators that seem to confirm that even large conversions will be ok at long as the tax rates at the end period are close to the rates at conversion. These calculators all assume that the taxes are paid from outside the tIRA but, in our case, I would deduct Fed and State taxes directly from the tIRAs. My taxable funds all have capital gains of about 60% so I don’t want to sell them to pay the tax. And those funds are not sufficient to cover the conversions anyway. Still, the value equivalence seems to roughly hold when paying the tax from the IRA funds. If I have two $1M tIRAs and convert one to a Roth paying $300k in tax, I have a $700K Roth and a $1M tIRA. If I die tomorrow and cash out both, they are worth the same $700k each after tax. If I leave them both in the account to appreciate at the same rate, they will remain equivalent over time, provided the tax rates are the same when they come out. There are lots of things that can happen to change outcomes but the underlying equivalence if the tax rates stay the same seems intuitive.

If the above is fair, it seems that, if I am correct that my heirs’ income tax rates will be the same or higher when the IRAs are inherited, converting as much as possible would make sense, regardless of bracket. The outcome should be a wash or, hopefully, better since the smaller estate size would reduce the DC estate tax. If, in fact, their income tax rates turn out to be significantly lower they could lose out. Does this sound about right, or am I missing something obvious?

.

I don’t want to lay my financials out in detail, but suffice it to say that DW and I are currently right at the beginning of the 24% Federal tax bracket and will remain there for three years at which point large RMDs will kick in. The RMDs will fill the 24% bracket and spill over a bit into the 32% bracket. Over time, with good market growth, the RMDs could eventually kick us right up toward the top. The amounts we are interested in converting far exceed the room available in lower than 37% brackets over the first three years. Assuming we want to wrest the most out of the lower brackets it seems like we should fill them, but what about more? If we need another $2M to help with DC estate tax, should we just bite the bullet and convert a large part of that in year 1 at 37%? Is there a substantial down side to that that I am missing?

I can’t quite wrap my head around this. Is it reasonable to think of all conversions as a wash if you and your heirs will be at high brackets? Does that make a conversion into 37% neutral? If so, the potential advantages to offset DC estate taxes make it attractive. But I fear I am missing something that would make those large immediate conversions less than a wash. I will consult with a CPA and maybe an FA before doing anything but I would like to noodle this around first.

First world problem isn't it? Thoughts?

")