I'll use my example. What I used as a set point to see how much to remove from the tIRA was to analyze what my tax environment would be like post RMD. 12% is the best tax environment. I ran across some data I think at Fidelity that the median tIRA had about 500k meaning 500K is the most common amount. RMD + SS would provide the bulk of my ordinary income and I'm married FJ. 500K RMD's $19K at 72 combined SS is $54K of which 85% is taxable or 46K to net a taxable . If we take standard deduction our ordinary income is around 62K. The top end of standard deduction MFJ income is around 103K so I have about 41K of ordinary income to pay with before crossing into 22%. If SS inflates at 2.5% and I keep my tIRA at 500K my income will be 97K. (.85%*62K) + 34K)) still below the 22% threshold. About age 87 is when I will cross into 22%. So how do you keep the tIRA at 500K? RMD is required minimum, you can take more, so my tIRA is risked at about a 7% return. In good years I can take >RMD. In bad I can take just RMD. RMD is calculated on the total value of the tIRA's at the end of the year. I use

this calculator. I estimate my taxes using this calculator

Tax Plan Calculator by Maxim Lott

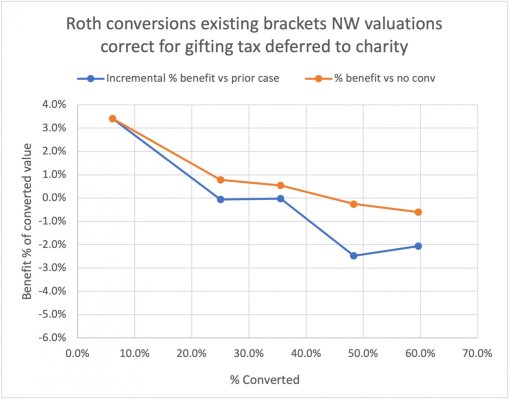

I did an analysis on taxes and in the main soak the rich starts at 22%, so the longer you can avoid 22% the better you are. This strategy keeps you in 22% ordinary income around 15 years.

To fund my Roth, I used some tax loss harvest and cashed in some brokerage stocks for a net 0% tax, basically turning my brokerage into a partial Roth. I live on cash. Therefore my only ordinary income is my Roth conversion. I have converted to the top of the 24% but find it much cheaper to keep conversions < $250K for various cliff and surcharge reasons. This gives you the greatest conversion for the least taxes.

In my case I retired at 65 which gave me 5 years of conversion which has now increased to 7 with CARES passage. The bulk of my conversions will be converted by this year. Next year I commence SS and so my conversion will take that income into account. The way I look at it is the government tends to leave the middle guy alone and soak the rich, so your job is to look like a middle guy. There is plenty of leeway to pull money out of other accounts as needed. My Roth money is most sacred as it provides the basis of self insurance in case someone strokes or needs memory care. tIRA + SS pays for hamburgers and electricity. It has a bonus variable based on how the market does. Other needs, like a new car or travel are provided by brokerage since cap gains are relatively low. After you've been to Europe of Asia a couple times it looses its luster.

The government already owns those taxes in the tIRA and you're going to have to pay. The way the the system is rigged as you age taxes go up and RMD goes up, so each year more for Sam and less for you. Also once I die, my wife will likely kick up only one tax bracket instead of 3.