Woodman53

Confused about dryer sheets

Hi Everyone,

I have been reading the forum for many years and finally joined today. This is a great forum and is always very interesting. Love all the topics that are presented.

Let me tell you about myself. I took a buy out and retired in 2014 at age 61 from a mega corporation and then they called me back in 2016 for a three-month assignment that ended up lasting until December 2022. It was all good as they paid me well and I got to make my own hours. Sometimes I worked from home and sometimes I went in. Worked about 20 hours per week. This allowed me to bridge to Social Security and I will not take it until I reach 70 in October of this year.

My question is about Roth Conversions.

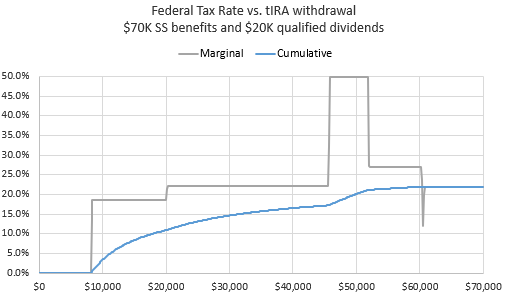

I would like to do about a $750,000 in Roth Conversions. But as I do the math it gets very complicated because of the IRMAA, Federal Tax Brackets and the taxing of Social Security Income. I always thought that 85% of my Social Security income would be taxed. My income is composed of a $60,000 Non-Cola Pension and $73,000 Social Security Income (spouse and myself) for a total of $133,000. I always assumed that 85% would be taxed as my pension income was over $45,000. But I found out this is not actually the case after running it through an online calculator and completing the IRS form found in the 1040 instructions. If these are my only two sources of income, then approximately 69% of my Social Security will be taxed. So that means instead of $62,050 (85%) only $50,370 (69%) will be taxed. A tax savings of ($62,050 - $50,370) * 22% = $2569. So, the faster I can complete the conversions the faster I can start to receive this tax savings because when I am doing the conversions 85% of my Social Security will be taxed.

I originally ran two scenarios;

No.1 - Convert to just below the first IRMAA limit $194,000. This would take 11 years.

No. 2 - Convert to the top of the first IRMAA limit $246,000. This would take 7 years.

I also assumed that the IRMAA limits would increase by 2.5%/year, in Scenario No. 2 some of the income would be taxed at 24% and I would be doing RMDs starting at 72.

Not factoring the impact on taxable Social Security Income Scenario No. 1 was better.

Taking in account how Social Security will be taxed scenario No. 1 and 2 seem to be about equal or No. 2 looks slightly better.

Many of you have run these numbers. Does this sound correct. Any direction you can give me will help.

Why do they make this so complicated. I did not think there would be math in retirement.

Thanks for reading.

I have been reading the forum for many years and finally joined today. This is a great forum and is always very interesting. Love all the topics that are presented.

Let me tell you about myself. I took a buy out and retired in 2014 at age 61 from a mega corporation and then they called me back in 2016 for a three-month assignment that ended up lasting until December 2022. It was all good as they paid me well and I got to make my own hours. Sometimes I worked from home and sometimes I went in. Worked about 20 hours per week. This allowed me to bridge to Social Security and I will not take it until I reach 70 in October of this year.

My question is about Roth Conversions.

I would like to do about a $750,000 in Roth Conversions. But as I do the math it gets very complicated because of the IRMAA, Federal Tax Brackets and the taxing of Social Security Income. I always thought that 85% of my Social Security income would be taxed. My income is composed of a $60,000 Non-Cola Pension and $73,000 Social Security Income (spouse and myself) for a total of $133,000. I always assumed that 85% would be taxed as my pension income was over $45,000. But I found out this is not actually the case after running it through an online calculator and completing the IRS form found in the 1040 instructions. If these are my only two sources of income, then approximately 69% of my Social Security will be taxed. So that means instead of $62,050 (85%) only $50,370 (69%) will be taxed. A tax savings of ($62,050 - $50,370) * 22% = $2569. So, the faster I can complete the conversions the faster I can start to receive this tax savings because when I am doing the conversions 85% of my Social Security will be taxed.

I originally ran two scenarios;

No.1 - Convert to just below the first IRMAA limit $194,000. This would take 11 years.

No. 2 - Convert to the top of the first IRMAA limit $246,000. This would take 7 years.

I also assumed that the IRMAA limits would increase by 2.5%/year, in Scenario No. 2 some of the income would be taxed at 24% and I would be doing RMDs starting at 72.

Not factoring the impact on taxable Social Security Income Scenario No. 1 was better.

Taking in account how Social Security will be taxed scenario No. 1 and 2 seem to be about equal or No. 2 looks slightly better.

Many of you have run these numbers. Does this sound correct. Any direction you can give me will help.

Why do they make this so complicated. I did not think there would be math in retirement.

Thanks for reading.

")