LuckyDog

Recycles dryer sheets

I am a Schwab client and recently received a notification of an advisory service called Schwab Intelligent Advisor. My question is: has anyone check this out and what do you think of it?

It's worth considering, especially if you are interested in checking out a robo-adviser without paying any fees. The advantages include low-cost diversification, set-it-and-forget-it rebalancing, and some tax-loss harvesting. The controversial element of Schwab Intelligent Advisor is the amount of cash the account holds. Some people see this requirement as a hidden method of financing the accounts. Schwab argues that it makes sense on its own. I find Betterment provides more information and performs approximately the same even though it charges a fee, although those charges go up to 0.5% on June 1.

I am a Schwab client and recently received a notification of an advisory service called Schwab Intelligent Advisor. My question is: has anyone check this out and what do you think of it?

Bingybear,

I thought the same as you. It appears to me (could be wrong) that some of the replies to my original question refer to Schwab Intelligent Portfolios. My original post has been edited to be more clear.

As far as the Intelligent Advisor goes, I cannot see what is offered that is better than my advisor who, I feel does an excellent job.

LuckyDog

Yup. Guilty as charged, sloppy reading. Mitigating circumstances: Probably the IA offering uses the Intelligent Portfolios robot.OP, it looks like most if not all the replies either talked about Intelligent portfolios (IP) or alternatives to them. ...

Of course they have value. To the guys selling them. It's kind of comical, too, how we see hundreds of sector funds suddenly masquerading as "index" funds. The hucksters are clever people.Oops. Never heard of the IA, my bad.

Fundamental ETF's look like another fad to me. Anyone think they have value over pure indexes?

I've avoided this trend regardless of provider.

2) paying the robt to do asset allocation maintenance that can be accomplished for free with simple annual rebalancing. The robot is just cheaper than having a human do it.

I don't know if IA uses the same allocation for all account or not. You can set up different risk levels for each account with IP. But in general I would agree that they don't seem to split assets by type into appropriate accounts.My main problem with the Schwab Intelligent Advisory service is that they have no concept of differing account types and how to manage balances accordingly. For example, let's say that I have a $100,000 balance in my Schwab brokerage account, and $100,000 balance in my Schwab Roth account, and my profile targets a 50/50 stock/bond split. According to the theory of tax-efficient asset allocation, you would ideally want to have the brokerage account fully invested in a good stock fund, while the Roth would be invested in a bond fund. However, with the Schwab Intelligent Advisory service, you'd be 50/50 in each account - generating unnecessary taxable events. Yes - this is an extreme, overly-simplistic example, but it's what I used in a meeting with a Schwab investment person a couple months back to illustrate why I believe this service is not a good fit for me. When they can factor in varying account types, I will re-consider.

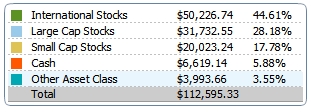

FWIW, here is what the robot has selected:

And here is the fund list:

Two features that strike me are the lack of home country bias -- really underweighting the US -- and the large number of funds used.

I hope this is readable from screen shots. I am too lazy to export and format this data.

no bonds? what risk tolerance did you select? Did you push it for mostly all stock?FWIW, here is what the robot has selected:

And here is the fund list:

Two features that strike me are the lack of home country bias -- really underweighting the US -- and the large number of funds used.

I hope this is readable from screen shots. I am too lazy to export and format this data.

I think one needs to know the inputs. Since there are no bonds you are really looking at US vs international equities effectively. It makes sense to me to increase the international portion as the US has lead for a long time. It is likely smart to overweight international. The number looks high with no bonds in the portfolio.Holly tomato Batman! 44% international. ??

There is a tenable argument that since the US is something like 52 or 54% of the world's investible stocks then that should be the percentage it represents in a portfolio. I also have another $100K test portfolio in a discretionary account with a DFA-affiliated advisor and that account is almost exactly 50% international with a slight tilt towards emerging markets.Holly tomato Batman! 44% international. ??

Yes, I gamed the questionnaire until I got it as close to 100% equities as I could. I am not interested in the robot's opinion of my AA, I just wanted to see what it did with equities.no bonds? what risk tolerance did you select? Did you push it for mostly all stock?