DaveLeeNC

Recycles dryer sheets

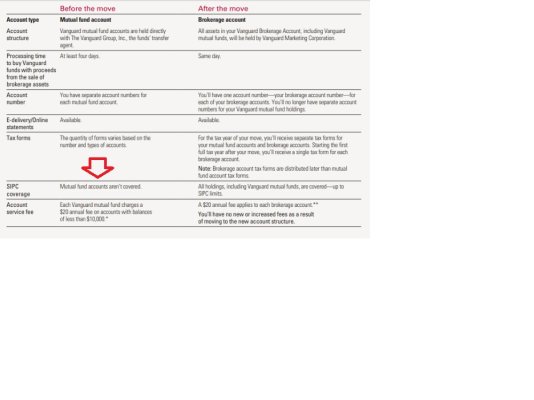

Does anyone worry about the SIPC limit of $500K per account ("separate capacities" as described by the SIPC folks)? I don't recall hearing this discussed but it seems like something to consider.

I am retired and have a tax deferred account with Fidelity that exceeds this limit by a fair amount. Somehow I cannot envision a situationm where SIPC coverage would kick in for the case of Fidelity. But history is full of stuff that is not envisioned.

Comments?

dave

I am retired and have a tax deferred account with Fidelity that exceeds this limit by a fair amount. Somehow I cannot envision a situationm where SIPC coverage would kick in for the case of Fidelity. But history is full of stuff that is not envisioned.

Comments?

dave