Sandy & Shirley

Recycles dryer sheets

Sorry for the PG rated title, but I didn’t know how else to arrange the 5 words this post is about. At least I did get your attention.

This post is not a question, I just wanted to pass on the primary issues that Shirley and I are taking into account as we plan for her retirement. Recognizing these issues early helped us to do things like Roth conversions and recharacterizations early so that we will have non-taxable sources of income as needed to avoid the Hump taxes we are about to discuss!

We are posting this because very few of the people that we talk to have any idea that they can be facing marginal federal tax rates as high as 55.5% with gross retirement income levels as low as $50,000. They also believe that all of the marriage penalties in our tax code were eliminated in 2002 and have no idea that they still exist for married couples today who are on Social Security.

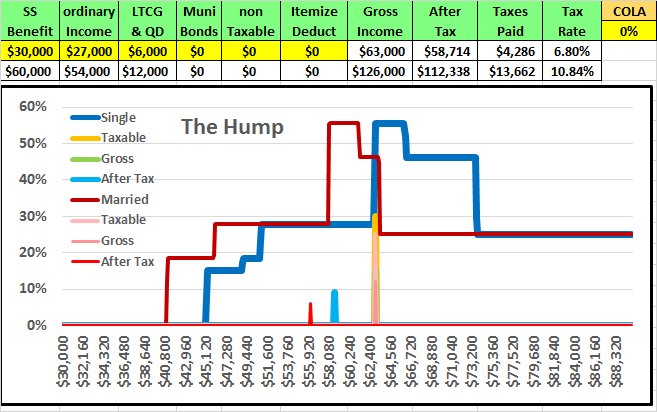

We are all used to the current 10%, 15%, and 25% tax brackets while we are working. The “parallel taxation” of our Social Security benefits can cause our marginal tax brackets to go as high as 55.5% at relatively low income levels, something that, as this picture illustrates, we call The Hump. The fact that the per capita married tax rate line happens before the per capita single tax rate line illustrates the marriage penalty that still exists for retirees, we all pay the same taxes, but married couples pay them earlier!

We are all used to the current 10%, 15%, and 25% tax brackets while we are working. The “parallel taxation” of our Social Security benefits can cause our marginal tax brackets to go as high as 55.5% at relatively low income levels, something that, as this picture illustrates, we call The Hump. The fact that the per capita married tax rate line happens before the per capita single tax rate line illustrates the marriage penalty that still exists for retirees, we all pay the same taxes, but married couples pay them earlier!

P.S. A marginal tax rate bracket comes from the total amount that your federal taxes increase for each additional dollar of income. Your actual Tax Bracket is only one of the reasons you pay more taxes.

Reference: https://taxfoundation.org/us-federa...2013-nominal-and-inflation-adjusted-brackets/

Prior to 2002 the ratio between tax brackets for Single vs. Married was 5 to 3. If the top of a single bracket was $6,000, the top of the same married bracket was only $10,000. The “Economic Growth and Tax Relief Reconciliation Act of 2001” changed that ratio to 2 to 1 so the bracket tops are now $6,000 and $12,000, the tax brackets for two married individuals are now 2 times the size of the same tax bracket for one single individual, as it should be.

Prior to 1983 the Social Security benefits you received during retirement were tax free. After all, the money you gave to Social Security from your paycheck had already been taxed once. The “1983 Amendments to the Social Security Act” recognized that your contribution was also matched by your employer who was able to make the contribution before paying taxes on it, so congress decided that half of your benefits check still needed to be taxable.

Since this was done during the Marriage Penalty years, they came up with a formula for the 50% taxation of your benefits to start at $25,000 for a single person and $32,000 for a married couple, a ratio of only 1.28 to 1! When your income is above these levels, taking an additional $100 withdrawal from a taxable source like your IRA/401K would increase your income for tax purposes by the $100 you withdrew plus another $50 of your SSB. If you were in the 15% bracket your taxes would increase $22.50, 15% of $150, a marginal rate of 22.5%. This double taxation would stop when 50% of your benefits had been taxed.

This changed again in 1993. “The Omnibus Budget Reconciliation Act of 1993” defined a second level of SSB taxability at 85% starting at income levels of $34,000 and $44,000, a 1.29 to 1 ratio, until 85% of your benefits have been taxed. Now if you were in the 15% bracket your taxes would increase $27.75, 15% of $185. This second level of double taxation would stop when 85% of your benefits had been taxed.

The taxation starting points of both of these bills are based on ½ of your SSB plus all of your other taxable income, and these starting points were defined by congress so they would not to tax lower income individuals IN 1983 AND 1993 WHEN THE LAWS WERE WRITTEN! After all, congress was only “taxing the rich”.

All of the other brackets and numbers related to your taxes and Social Security are adjusted each year for inflations or COLA. The $25,000, $32,000, $34,000, and $44,000 starting points for SSB taxation were specifically designed by congress not to be COLA adjusted. They are at the same levels today as they were 34 years ago. These double taxation points are now imposed on middle income and even some lower income retired individuals.

The 1993 legislation also created something that we personally refer to as the Tax Hump. We already mentioned the 27.75% marginal tax bracket when your actual tax bracket was 15%. The 1983 50% taxability levels rarely push anyone past the 15% standard tax bracket “today”, but the 85% taxability levels imposed in 1993 do! If you are in the 25% bracket your tax due increase would be $46.25, 25% of $185, a marginal tax bracket of 46.25%.

But, this can get even higher if you have personal investments that are earning dividends. Dividends are also tax deferred. They are tax free until they are pushed into the 25% bracket by your other taxable income at which time they are then taxed at a lower 15% dividend tax rate. Read the following multiple times if you don’t follow it the first time!

We try to estimate our year end tax returns quarterly and always pre-do our annual returns on Black Friday, the day after Thanksgiving. Depending on what we see; sometimes we let our bills wait until after the first of the year or pay them with Roth savings instead of IRA withdrawals. Sometimes we take out a little more in December to max out the 27.75% marginal bracket instead of our normal January withdrawals. This just gives us a head start / cushion on our needs for the next year.

To illustrate The Hump, this table is based on the current 2017 tax brackets:

The Start of your Tax Hump and it’s the width are determined by your personal SS benefit level, everyone’s situation is different. Since larger benefit amounts result in more deferred income, your taxes start at higher gross income levels so you save more in taxes than an individual whose entire gross income was not deferred. Since you are saving more in taxes at the start, you have to “Return” more of those savings inside The Hump so that your total savings will be reduced back to the point where only 15% of your benefit was tax free.

Also take note of the marriage penalty. The Domestic Couple income levels are two times the Single Individual levels, but Married Couple income and saving levels are all lower.

It should be noted that at all benefit levels if everyone is paying their full Hump taxes, their total taxes are almost equal and the marriage penalty no longer exists.

The first graph shows the worse case situation where the income levels are Single $63,000 each and Married $126,000 joint. If those numbers were increased to $80,000 and $160,000, everyone would be “Over The Hump”, only 15% of everyone’s SSB were tax free, and the taxes paid would be almost identical. The SSB Marriage Penalty is only that a married couple pays more at lower income levels. This only effects middle income Americans, not the Rich!

Hate to ramble on like this, but we just hope that this post has been informative to those who are planning for their early retirement!

This post is not a question, I just wanted to pass on the primary issues that Shirley and I are taking into account as we plan for her retirement. Recognizing these issues early helped us to do things like Roth conversions and recharacterizations early so that we will have non-taxable sources of income as needed to avoid the Hump taxes we are about to discuss!

We are posting this because very few of the people that we talk to have any idea that they can be facing marginal federal tax rates as high as 55.5% with gross retirement income levels as low as $50,000. They also believe that all of the marriage penalties in our tax code were eliminated in 2002 and have no idea that they still exist for married couples today who are on Social Security.

This is a picture of what we want to talk about.

P.S. A marginal tax rate bracket comes from the total amount that your federal taxes increase for each additional dollar of income. Your actual Tax Bracket is only one of the reasons you pay more taxes.

Reference: https://taxfoundation.org/us-federa...2013-nominal-and-inflation-adjusted-brackets/

Prior to 2002 the ratio between tax brackets for Single vs. Married was 5 to 3. If the top of a single bracket was $6,000, the top of the same married bracket was only $10,000. The “Economic Growth and Tax Relief Reconciliation Act of 2001” changed that ratio to 2 to 1 so the bracket tops are now $6,000 and $12,000, the tax brackets for two married individuals are now 2 times the size of the same tax bracket for one single individual, as it should be.

Prior to 1983 the Social Security benefits you received during retirement were tax free. After all, the money you gave to Social Security from your paycheck had already been taxed once. The “1983 Amendments to the Social Security Act” recognized that your contribution was also matched by your employer who was able to make the contribution before paying taxes on it, so congress decided that half of your benefits check still needed to be taxable.

Since this was done during the Marriage Penalty years, they came up with a formula for the 50% taxation of your benefits to start at $25,000 for a single person and $32,000 for a married couple, a ratio of only 1.28 to 1! When your income is above these levels, taking an additional $100 withdrawal from a taxable source like your IRA/401K would increase your income for tax purposes by the $100 you withdrew plus another $50 of your SSB. If you were in the 15% bracket your taxes would increase $22.50, 15% of $150, a marginal rate of 22.5%. This double taxation would stop when 50% of your benefits had been taxed.

This changed again in 1993. “The Omnibus Budget Reconciliation Act of 1993” defined a second level of SSB taxability at 85% starting at income levels of $34,000 and $44,000, a 1.29 to 1 ratio, until 85% of your benefits have been taxed. Now if you were in the 15% bracket your taxes would increase $27.75, 15% of $185. This second level of double taxation would stop when 85% of your benefits had been taxed.

The taxation starting points of both of these bills are based on ½ of your SSB plus all of your other taxable income, and these starting points were defined by congress so they would not to tax lower income individuals IN 1983 AND 1993 WHEN THE LAWS WERE WRITTEN! After all, congress was only “taxing the rich”.

All of the other brackets and numbers related to your taxes and Social Security are adjusted each year for inflations or COLA. The $25,000, $32,000, $34,000, and $44,000 starting points for SSB taxation were specifically designed by congress not to be COLA adjusted. They are at the same levels today as they were 34 years ago. These double taxation points are now imposed on middle income and even some lower income retired individuals.

The 1993 legislation also created something that we personally refer to as the Tax Hump. We already mentioned the 27.75% marginal tax bracket when your actual tax bracket was 15%. The 1983 50% taxability levels rarely push anyone past the 15% standard tax bracket “today”, but the 85% taxability levels imposed in 1993 do! If you are in the 25% bracket your tax due increase would be $46.25, 25% of $185, a marginal tax bracket of 46.25%.

But, this can get even higher if you have personal investments that are earning dividends. Dividends are also tax deferred. They are tax free until they are pushed into the 25% bracket by your other taxable income at which time they are then taxed at a lower 15% dividend tax rate. Read the following multiple times if you don’t follow it the first time!

- · You take $100 out of your IRA.

- · This causes $85 of your SSB to become taxable income.

- · Your taxes due will increase by $27.75 which is 15% of $185.

- · This additional $185 of taxable income also pushes an additional $185 of your dividends across the 25% boundary.

- · Your taxes due on this additional dividend income will also be $27.75, 15% of $185.

- · Your total taxes due will be $27.75 on the income plus SSB and another $27.75 on the dividends.

- · This is a total tax increase of $55.50 on a $100 withdrawal from your IRA/401K, a marginal federal tax rate of 55.5%!

- · The 25% Federal Brackets for 2017 are scheduled to start at $37,950 for individuals and $75,900 for married couples. At these income level your marginal tax rates could be 46.25% or 55.5%.

- · If your taxable income is over $418,400 your marginal tax rate will only be 39.6%!

We try to estimate our year end tax returns quarterly and always pre-do our annual returns on Black Friday, the day after Thanksgiving. Depending on what we see; sometimes we let our bills wait until after the first of the year or pay them with Roth savings instead of IRA withdrawals. Sometimes we take out a little more in December to max out the 27.75% marginal bracket instead of our normal January withdrawals. This just gives us a head start / cushion on our needs for the next year.

To illustrate The Hump, this table is based on the current 2017 tax brackets:

| Benefit | Start Tax | Save | Start Hump | Width | Return |

| Single Individual | |||||

| $20,000 | $31,954 | $2,534 | $55,567 | $3,139 | $1,784 |

| $25,000 | $36,954 | $3,284 | $59,419 | $6,787 | $2,347 |

| $30,000 | $41,303 | $3,937 | $63,270 | $10,436 | $2,812 |

| $35,000 | $45,467 | $4,561 | $67,121 | $14,085 | $3,249 |

| Domestic Couple | |||||

| $40,000 | $63,908 | $5,069 | $111,134 | $6,278 | $3,569 |

| $50,000 | $73,908 | $6,569 | $118,838 | $13,574 | $4,694 |

| $60,000 | $82,606 | $7,873 | $126,540 | $20,872 | $5,623 |

| $70,000 | $90,934 | $9,123 | $134,242 | $28,170 | $6,498 |

| Married Couple | |||||

| $40,000 | $56,597 | $4,062 | N/A | N/A | $3,162 |

| $50,000 | $64,299 | $5,217 | N/A | N/A | $3,642 |

| $60,000 | $72,002 | $6,373 | $113,027 | $5,679 | $4,123 |

| $70,000 | $79,704 | $7,528 | $120,730 | $12,976 | $4,903 |

Also take note of the marriage penalty. The Domestic Couple income levels are two times the Single Individual levels, but Married Couple income and saving levels are all lower.

It should be noted that at all benefit levels if everyone is paying their full Hump taxes, their total taxes are almost equal and the marriage penalty no longer exists.

The first graph shows the worse case situation where the income levels are Single $63,000 each and Married $126,000 joint. If those numbers were increased to $80,000 and $160,000, everyone would be “Over The Hump”, only 15% of everyone’s SSB were tax free, and the taxes paid would be almost identical. The SSB Marriage Penalty is only that a married couple pays more at lower income levels. This only effects middle income Americans, not the Rich!

Hate to ramble on like this, but we just hope that this post has been informative to those who are planning for their early retirement!

, I might be wrong, I believe someone poster on this a while ago, but its a well laid out post, thank you, when I have more time Im going to study this at length.

, I might be wrong, I believe someone poster on this a while ago, but its a well laid out post, thank you, when I have more time Im going to study this at length.