I went through your post and deleted everything except the part that applies to the couple in the OP. They are not grandfathered into anything, they are operating with the new law.

So, they are just left with this paragraph. Maybe I missed something that is relevant to them. If so, please add it.

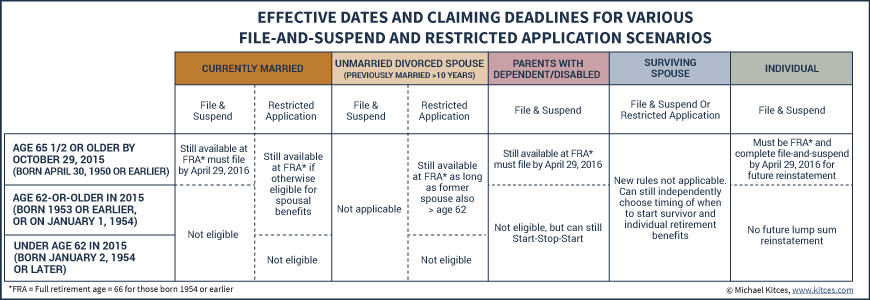

This is an earlier post that bothered me:

In the OP case, the husband is six years younger than the wife, and has an fra of 67.

I don't see how he can wait till age 67 to start a spousal benefit. She will have to start when she is 70 and he is 64. At that time, he will be "deemed" to be applying for both benefits. If any spousal is available, he will have to start then.

Maybe you can explain otherwise.

-------

I think we should also look at the numbers for this case. It seems to me that his PIA is more than half her PIA. So, in their case, spousal is off the table regardless of ages. Do you agree with that?

All this discussion of spousal benefits assumes that his PIA is lower than the OP states - you used $1,000 in post #11. I've been going with to try to sort this out in general.

to funny , i did use 1k in my example and now working on my desktop i see it was 1500 . on my nook it looked like 1000 to my eyes at first glance and i didn't realize it .

so in this case the base adder would be 1365 minus 1500 , in which case there will never be spousal so you were correct about that part .

but just for the education lets assume it was the 1k i thought it was .

so the scenario would shake out that assuming his was 1k and not 1500 , the spousal base amount would be 1365-minus 1000 which leaves a spousal benefit of 365 left . but that 365 will be reduced if he takes it earlier than fra .

the earliest he could file would be 62 which makes her 68 . at 62 if he filed first he would get only his benefit at first . there is no 2nd componenant until she files .

so actually she could wait 2 years until he is 64 to file and the 365 will not be reduced as much as at 62 .

so the closest he could get to fra is 64 and her 70 .

so he would become eligible for spousal at 64 but it is not an automatic process . he has to fill out an application to start getting spousal or he does not get a thing additional . .

the ss office told us that once i file my wife has to complete the process by filing a spousal application or no change will happen to her amount even though she is eligible . . it would be silly though not to grab it as soon as you are eligible .

so in this hypothetical example the wife would get her 70 benefit . he would get his early 64 benefit as one component , the adder of 365 is reduced 25/36 of one percent for each month before 67, up to 36 months. If the number of months exceeds 36, then the benefit is further reduced 5/12 of one percent per month.

if it was a more typical closer age situation and he was able to hit fra before taking spousal the calculation is much more simple .

it is just 1/2 the primary amount less the primary amount of the lower spouse . any difference is added to his own benefit .

what makes deciding when to co-ordinate the filing is there are two moving targets .

while me filing gets my wife her spousal adder faster , the fact i get reduced more taking it sooner can offset the spousal gain .

so we will balance it out with me taking ss at 65 . i am concerned about medicare increasing a lot more for me if i don't file .

we could get the biggest bang for the buck with me filing restricted application and waiting until 70 but since we are pretty good financially i see no point running until 70 before taking mine and her getting spousal .

i intentionally picked 65 because i still like doing consulting work 1 day a week and occasionally helping out on some big projects . the year before you are fra special rules apply and you can earn like 2x what you can in earlier years if collecting before having to give back money