JohnDevereaux

Confused about dryer sheets

- Joined

- Jan 29, 2020

- Messages

- 8

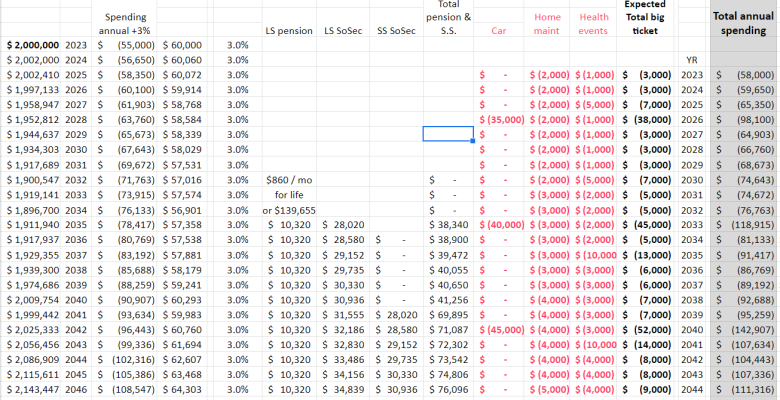

I'm down to the 2 year mark where I hit 59.5 yr old. I want to retire. I worry that I'm not prepared. I'm no financial guru, if someones having a heart attack, a broken bone, or have been shot, I'm game for fixing/aiding that, but finances, pfffft. I'm not clueless, I've done things that retirement advisors have suggested. I'm 100% debt free, own my home and the one next door with 10 acres of land, and 3 vehicles under 2 years old. I currently make about 80-90k yr. I figure in retirement, I'll only need 50-60k yr. So far my wife and I have built 4 traditional 401k's to a total of 1.75m, hoping to have 2m total in 2 more years. It seems like a big number, but I'm always worried if it's adequate. Is this adequate?

")