SecondCor521

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

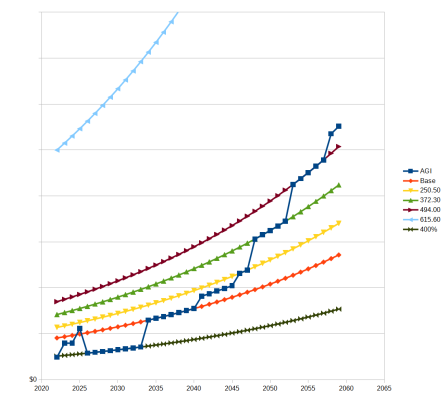

Hi all,

I have a straightforward tax-related math problem in my RMD/conversion/IRMAA spreadsheet that I can't seem to wrap my brain around.

When I am trying to optimize my Roth conversions, I want to convert up to, but not beyond, a marginal rate that I will face later. But I know that at some point I won't be alive later, and it'll be my kids' problem to optimize their tax rates. So my goal is to calculate a weighted average marginal tax rate taking my life expectancy into account.

I have a year-by-year projection of my marginal tax rate between now and age 90. So for example, I might be in the 12% bracket now, the 22% bracket when I am 70, and a 36% bracket when I am 90.

I also have a year-by-year probability that I will be alive (based on SSA tables). So for example, I have a 100% chance of being alive today, about an 80% chance of being alive when I am 70, and about a 20% chance of being alive at age 90.

In both cases, I actually have about 40 rows, not just 3, because I'm 53 now and plan each year through age 90.

What I have done so far is just multiply the rate by the probability that I will be alive for each year, then take the moving average of those results. But that seems to result in a percentage that never makes it above about 16%, which seems intuitively to be too low for my situation. (In the example below, I just use the three data points; in my real full table with 40-ish rows, there are a lot of rows in the 22% bracket which raises the moving average column up to 16%.)

Anyone understand what I'm asking about and what the proper math is?

I have a straightforward tax-related math problem in my RMD/conversion/IRMAA spreadsheet that I can't seem to wrap my brain around.

When I am trying to optimize my Roth conversions, I want to convert up to, but not beyond, a marginal rate that I will face later. But I know that at some point I won't be alive later, and it'll be my kids' problem to optimize their tax rates. So my goal is to calculate a weighted average marginal tax rate taking my life expectancy into account.

I have a year-by-year projection of my marginal tax rate between now and age 90. So for example, I might be in the 12% bracket now, the 22% bracket when I am 70, and a 36% bracket when I am 90.

I also have a year-by-year probability that I will be alive (based on SSA tables). So for example, I have a 100% chance of being alive today, about an 80% chance of being alive when I am 70, and about a 20% chance of being alive at age 90.

In both cases, I actually have about 40 rows, not just 3, because I'm 53 now and plan each year through age 90.

What I have done so far is just multiply the rate by the probability that I will be alive for each year, then take the moving average of those results. But that seems to result in a percentage that never makes it above about 16%, which seems intuitively to be too low for my situation. (In the example below, I just use the three data points; in my real full table with 40-ish rows, there are a lot of rows in the 22% bracket which raises the moving average column up to 16%.)

| Age Tax Life% Product Average |

| 53 12% 100% 12% 12% |

| 70 22% 80% 17.6% 14.8% |

| 90 36% 20% 7.2% 12.27% |

Anyone understand what I'm asking about and what the proper math is?