Andre1969

Thinks s/he gets paid by the post

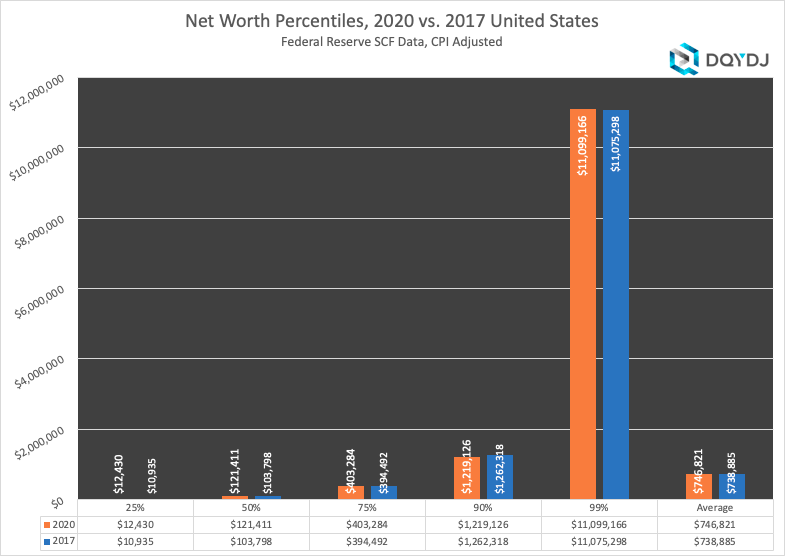

The difference between the 90th and the 99th percentile would be life-altering for me.

If I was at the 90th, ~$1.219M, I would have never had the guts to buy my house. I would be getting excited about the possibility of retiring "in the near future", if the stock market cooperated, but it wouldn't most likely be an extravagant retirement.

But at the 99th, ~$11.099M, I'd be calling my employer and telling them to get their computer out of my house, because I'm done with them. It would probably be a much nicer house than I ended up buying, as well. And I don't think I'd ever worry about anything financial again, as long as I lived. Unless I ran into some really horrible medical bills, or someone sued the hell out of me, I guess. Now I'm not the type to have aspirations of owning a private jet, a yacht, multiple vacation homes in expensive areas, buy expensive cars and trade every few months, etc. So to me, $11M would be a lot of money.

Right now, I'm around the entry point for the 94% threshold. If I was to lose my job, I wouldn't panic. Probably wouldn't look for another one. But, I wouldn't do anything extravagant, at least not at first. I'd still cut my own grass, rather than pay someone to do it. I'd keep driving the same car until something catastrophic happened on it, and then I'd probably go buy something a bit practical, and on a bit of a budget, rather than splurging.

But, put me to the 95% threshold, I'd definitely retire, and open the purse strings considerably. And at the 96%, $3.294M, I think I'd be pretty happy financially.

So in my case, even a 1-2% move in percentile (94 to 95 or 96%) could make what I'd call a life altering difference. It's the difference between "I'm close to retiring, but might have to budget here and there" to "I'm already gone, and not a financial care in the world!"

If I was at the 90th, ~$1.219M, I would have never had the guts to buy my house. I would be getting excited about the possibility of retiring "in the near future", if the stock market cooperated, but it wouldn't most likely be an extravagant retirement.

But at the 99th, ~$11.099M, I'd be calling my employer and telling them to get their computer out of my house, because I'm done with them. It would probably be a much nicer house than I ended up buying, as well. And I don't think I'd ever worry about anything financial again, as long as I lived. Unless I ran into some really horrible medical bills, or someone sued the hell out of me, I guess. Now I'm not the type to have aspirations of owning a private jet, a yacht, multiple vacation homes in expensive areas, buy expensive cars and trade every few months, etc. So to me, $11M would be a lot of money.

Right now, I'm around the entry point for the 94% threshold. If I was to lose my job, I wouldn't panic. Probably wouldn't look for another one. But, I wouldn't do anything extravagant, at least not at first. I'd still cut my own grass, rather than pay someone to do it. I'd keep driving the same car until something catastrophic happened on it, and then I'd probably go buy something a bit practical, and on a bit of a budget, rather than splurging.

But, put me to the 95% threshold, I'd definitely retire, and open the purse strings considerably. And at the 96%, $3.294M, I think I'd be pretty happy financially.

So in my case, even a 1-2% move in percentile (94 to 95 or 96%) could make what I'd call a life altering difference. It's the difference between "I'm close to retiring, but might have to budget here and there" to "I'm already gone, and not a financial care in the world!"

But again, that's me...

But again, that's me...