I'm just turning 61. Both my spouse (60) and I definitely plan on taking SS at 62. I ran the numbers and it makes no sense to wait. The break even point (where SS at 66 catches up) is 81. From a common sense perspective, it doesn't make sense to wait either.

Careful there. Please realize that you are saying that people who are planning to take it late have no common sense. If you study the posts of some of those people, I think you will find they have plenty of sense, common and other-wise.

It amazes me how people think they're immortal, are exceptions to genetics and the laws of nature, and will somehow live to 90-100 or beyond. You even see this silly talk from "financial planners" that by taking SS late, you'll get maximum benefits past 100. Who lives past 100? Ridiculously impractical and unrealistic advice and thinking. The average American life expectancy is 78.2.

I suggest that you study a bit. You are mis-applying 'life expectancy'. First, that is an average number, so by definition, half live longer. Second, you need to look at LE at a specific age.

https://personal.vanguard.com/us/insights/retirement/plan-for-a-long-retirement-tool

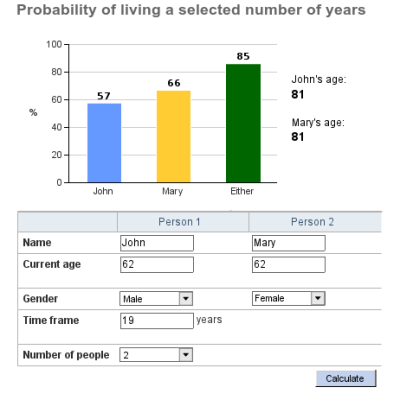

Male. A 65-year-old man has a 41% chance of living to age 85 and a 20% chance of living to age 90.

Female. A 65-year-old woman has a 53% chance of living to age 85 and a 32% chance of living to age 90.

Couple. If the man and woman are married, the chance that at least one of them will live to any given age is increased. There's a 72% chance that one of them will live to age 85 and a 45% chance that one will live to age 90. There's even an 18% chance that one of them will live to age 95, as shown below.

Your 78.2 number does not apply. Careful what you call 'common sense'.

Another aspect is who is going to be physically active enough and can use that extra delayed money starting at age 81?

And when I'm less active, I might need more money, to have people do things for me I can no longer do for myself.

Finally, I'm not a conspiracy theorist, but the government would very much like to see everyone delay the start of their benefits. Like a casino, the odds are in their favor that most of these people will die early and never use their full benefits had they started at 62. If everyone started at 62, the system would go broke.

OK, don't take it personally, but I'm going to be more blunt here. That is an ignorant statement (not stupid, but 'ignorant', as in 'unaware of the facts'). If you do some research, you will find that the SS payouts are pure actuarial calculations. There is no intentional bias there. There are some biases in that they don't use different numbers by gender, but the early/late decision is not 'gamed' by the govt.

Common sense is great, but one needs to be informed to use it.

It's very odd to me that at any time we generally have at least one thread running suggesting taking early SS, and at leaast one other thread espousing purchase of immediate annuities. Some posters don't just say that they want early SS, but that it is the only thing that makes sense, or that anyone who plans to wait must delusionally expect to be Methusalah

Other posters say that annuities are better than bonds and stocks, or at least that you need one, regardless of their high price and non-zero risk. Since there is no cheaper or less risky annuity than the one bought by delaying SS, this is hard to understand.

Can someone explain it?

Ha

Yes, but I would probably put it in a way that would cause the mods to (rightly, to keep the peace), delete my post. So I shall refrain.

")

-ERD50