Not exactly. It's completely possible for more than half of the data to be above or below "average."

10 people live on an island. 9 die at 100 yo and 1 dies at 10 yo. The average age of death = 910/10 or 91 years old. So, 9 died "above average" and 1 died "below average."

This from my 12 year old grandson who I asked about it. Is he correct or do I need to straighten him out on this? He also mentioned he hopes Papa lives to an "above average" age. What a nice young man!

Good for him. I'll guess that most 12 year olds have seen the difference between "mean" and "median" in school, but very few can apply it like this outside of school.

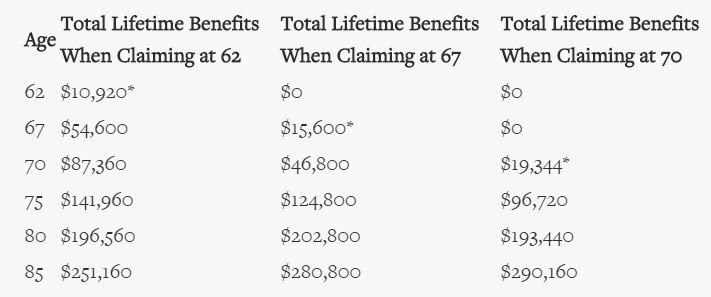

For this mortality table*, the median (age at which 50% have died) and the mean (the sum of the total years of life above age x, divided by the number alive at x) differ by about one year. The median is a little higher.

The life expectancy (aka expectation of life) at age 62 is

20.49 for males

23.28 for females

If we look at 1,000 males attaining age 62

512 reach 83 (21 years)

475 reach 84 (22 years)

So the 500th death must be around 21.3 years

Similarly, for 1,000 females attaining age 62

518 reach 86 (24 years)

478 reach 87 (25 years)

So the 500th death must be around 24.4 years

* The table is the Social Security Actuaries' Cohort Table for the entire population born in 1960.

https://www.ssa.gov/oact/NOTES/as120/LifeTables_Tbl_7_1960.html

A "cohort" table projects a continuation of falling mortality rates. I think it's a better choice than a "period" table.

OTOH, the entire population includes people in hospices, people in nursing homes, people who have been told by their doctors they only have __ months to live, etc. If I'm making plans for myself, I'd prefer a table that's based on people in "normal good health".