Yes, there would need to be deflation to have the principal lowered. But remember

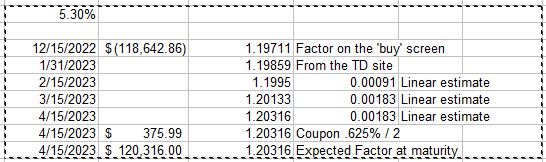

TIPS are inflation adjusted daily, not annually, so you only need short term CPI deflation to have the principal adjusted downward, not annual, year over year deflation. That is the only reason I can think of why the short term real yields are so high right now compared to the 5 year rates. I don't usually buy short maturity TIPS on the secondary market so maybe someone else with more experience in that area can chime in on that.

This is what Wikipedia has to say about deflation - "Throughout the history of the United States, inflation has approached zero and dipped below for short periods of time. This was quite common in the 19th century, and in the 20th century until the permanent abandonment of the gold standard for the

Bretton Woods system in 1948. In the past 60 years, the United States has only experienced deflation two times; in 2009 with the Great Recession and in 2015, when the CPI barely broke below 0% at −0.1%".

Check out what happened to TIPS real yields in 2009 in the chart in this article -

https://seekingalpha.com/article/4083257-real-yields-on-tips-are-key-must-watch-indicator. Last recession TIPS real yields went up significantly on deflation fears because they can lose principal with deflation. We may have another good buying opportunity if history repeats itself.