|

|

12-05-2014, 08:24 AM

12-05-2014, 08:24 AM

|

#21

|

|

Full time employment: Posting here.

Join Date: Feb 2014

Posts: 731

|

Quote: Quote:

Originally Posted by RetireBy90

2 points,:

1) I likewise am using 4% only as a check to verify we have sufficient that 4% will fill the gap between other income and spending. Once we start SS (66 and 70) I don't plan to take any from IRA to cover expenses. Perhaps some to cover other expenses like travel or a new liver  |

Well, don't be surprised that you will be *required* to take distributions from your IRA (assuming it is a tIRA and not a ROTH) at age 70.

In our scenario, even when doing 'top off' Roth conversions up to 70, we still get whammed by RMD, I just hope the DW and I are still up and about to take whirl wind world cruises and skydiving lessons with all the 'extra' money cuz of RMDs at 70!

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

12-05-2014, 08:31 AM

|

#22

|

|

Recycles dryer sheets

Join Date: Oct 2013

Posts: 281

|

Quote:

Originally Posted by athena53

I do something similar. I like the regularity of a "paycheck" so I move money out of the brokerage account $20K at a time and then move it into the spending money on a monthly basis. (I've got the world's most complicated checking account spreadsheet.) I don't intend to increase it for inflation next year. It will come out to a 2.5% withdrawal rate; I'm 61 and will wait for spousal SS till age 67, my own at 70, and a pension at 65 ($12,000/year). Withdrawal rates should decrease when those kick in.

|

athena, am curious what your thoughts are on just staying with a 2.5% withdrawal rate when SS arrives, and instead kicking up the spend?

We likewise have been at between 2.4% and 2.5% since ER'ing, but are thinking there's no reason not to continue doing same even after pensions, SS and Medicare arrive, since all indicators are that we can continue to do so with a 100% success rate probability, and still leave a sizable estate at end of life.

|

|

|

|

|

12-05-2014, 08:33 AM

|

#23

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2009

Location: Cville

Posts: 1,604

|

Quote:

Originally Posted by BBQ-Nut

Well, don't be surprised that you will be *required* to take distributions from your IRA (assuming it is a tIRA and not a ROTH) at age 70.

In our scenario, even when doing 'top off' Roth conversions up to 70, we still get whammed by RMD, I just hope the DW and I are still up and about to take whirl wind world cruises and skydiving lessons with all the 'extra' money cuz of RMDs at 70! |

I understand that, but my plan is to start pulling from the IRA as soon as we retire, even if it is just to put it into another account. This would pull some from the account before RMD kicks in, giving me a lower average income by adding 10 years to the number of years. I've given up on trying to find a tax efficient method, we have about $60K of pension, great to have, but it will keep us in a higher marginal tax bracket in retirement. Add to that 85% of SS and then the RMD and we will be funding Govt phones for years to come.

Just remember George HW Bush did the sky diving well into RMD territory, if he can so can I and so can you!!!

|

|

|

|

|

12-05-2014, 08:43 AM

|

#24

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,370

|

Quote:

Originally Posted by athena53

I do something similar. I like the regularity of a "paycheck" so I move money out of the brokerage account $20K at a time and then move it into the spending money on a monthly basis. (I've got the world's most complicated checking account spreadsheet.) I don't intend to increase it for inflation next year. It will come out to a 2.5% withdrawal rate; I'm 61 and will wait for spousal SS till age 67, my own at 70, and a pension at 65 ($12,000/year). Withdrawal rates should decrease when those kick in.

|

Similar here but I do it monthly. When I rebalance annually I bring my cash in a 0.9% interest online savings account back up to 6% of our total nestegg. The 6% should be sufficient to fund 2-3 years of living expenses once combined with dividends from taxable investments that we take in cash.

I have a monthly "paycheck" that is a transfer from that online savings account to our local checking account which I use to pay our bills. Occasionally if we have special expenditures (for example, we bought a boat last summer, our property taxes for the year are due in November, etc) I make a special transfer from online savings to checking. So I can tell our withdrawals for the year by just adding up the transfers out of the online savings account.

We have been retired for 3 years now and I haven't yet felt the need to give us a "raise" by increasing our monthly transfer from online savings to checking.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-05-2014, 11:03 AM

|

#25

|

|

Thinks s/he gets paid by the post

Join Date: Oct 2012

Location: Colorado Mountains

Posts: 3,165

|

|

|

|

|

|

12-05-2014, 12:37 PM

|

#26

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2009

Location: Cville

Posts: 1,604

|

Quote:

Hermit - no kidding. Don't even get to write it off as a charity

Not trying to get political here: I know some make more from investments than I do, but because I work for a check it is taxed differently? If we had a national sales tax and did away with income tax that may be an option, but then all that ROTH we been shoving in would be taxed again. Another option would be to treat all income as income. Carried interest - Cap Gains - Dividends - SS income - all of them treated the same would bring down the effective rate for me

|

|

|

|

|

12-05-2014, 02:29 PM

|

#27

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,370

|

Perhaps it would be good for you but it would be unfair to many.

Your wages are arguable a wash from a tax perspective in that while you pay tax on your wage income, your employer gets a tax deduction for what they pay you for wages and pay less taxes than they otherwise would (unless your employer is governmental or not-for-profit or similar entity that doesn't pay taxes). In fact, if you work for a corporation, then incremental tax benefit your employer receives on the wages it pays you (which would typically be 35%) is often more than what the employee pays in taxes on that income.

The corporate income that is the basis for the dividends that I receive has already been taxed once at the corporate level and it is taxed again at my level albeit at lower preferential rates. The corporate income that isn't distributed to me in the form of dividends is retained by the company and increases the company's value and is part of the capital gain when I sell my ownership interests, so part of that gain has already bee taxed as well. Similarly, my contributions to SS were not deductible so to the extent that the SS benefits that I receive are a return of previous contributions then that has already been taxed once as well.

A national sales tax would be very unfair to savers in that they have already paid taxes on the income they generated to build their savings so they shouldn't have to pay taxes on that same principal again when they spend it.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-05-2014, 02:50 PM

|

#28

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2014

Location: Spending the Kids Inheritance and living in Chicago

Posts: 17,094

|

There are many aspects of income tax that are unfair.

The Carried interest is an unfair advantage to all the hedge fund managers, should be counted as income.

|

|

|

|

|

12-05-2014, 02:53 PM

|

#29

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,370

|

+1 on carried interest. One of the more outrageous inequities in the code - widely recognized as such yet Congress lacks the courage to do anything about it.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-05-2014, 04:32 PM

|

#30

|

|

Recycles dryer sheets

Join Date: Jun 2014

Posts: 406

|

Quote:

Originally Posted by RetireBy90

2 points,:

1) I likewise am using 4% only as a check to verify we have sufficient that 4% will fill the gap between other income and spending. Once we start SS (66 and 70) I don't plan to take any from IRA to cover expenses. Perhaps some to cover other expenses like travel or a new liver

2) Completely different tac here, I wonder if anyone has done any research like the author, with a model of say 4% but if market goes down, draw goes down by say 1/2 of the market drop. I expect that if I could expect $1,000 every month, say from SS then for some reason that drops to $800 this year, my spending would also drop. I would think this is more realistic than to assume spending will never change from the time you FIRE. As noted in other replies, some plan to increase and decrease as needs and income change, so shouldn't your projection of needed draw? |

I can't say that I've modelled things like you suggest specificially but using Flexible retirement planner I've done something similar, drop the market by 50% drop spending to what I assume is a minimum...and see how the money works out. I've run those kinds of scenarios to try and see if we could for example handle a say 60% drop in the market followed by a number of years of effectively no growth. At some point in time anything will fail of course but it makes me feel good to know that my spending and savings are in line with surviving all but a doomsday situation. And also that if I'm in serious trouble probably almost everyone else is too ...

__________________

If money is the root of all evil I want to be a bad man

|

|

|

|

|

12-05-2014, 04:46 PM

|

#31

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2012

Location: Seattle

Posts: 6,023

|

We are going to go with 3.5% to 4% (variable) at age 46 and if it fails....well, there is always money in the banana stand.

I am actually *ok* with it failing if we both get a good 20 years or so of retirement. No kids or anyone to worry about so we can always Thelma and Louise it.

Life has so many other unknowns (accidents, murder, cancer) that it seems a bit silly to worry a great deal about failure rates past 85% success.

|

|

|

|

|

12-06-2014, 05:33 AM

|

#32

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,192

|

i happen to like bob clyatts dynamic method alot. as a ballpark we will run at least the first few years with that method.

|

|

|

|

|

12-06-2014, 06:09 AM

|

#33

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2011

Location: The Bay Area

Posts: 2,736

|

Quote:

Originally Posted by Quantum Sufficit

Live and learn,

Looks like you and I will be joining the class of 2015 at the same time! But I have you beat at 2.83% swr |

Well, let's hope that is a 'sufficient quantity.'

__________________

You may be whatever you resolve to be.

100% x 10% > 10% x 100%

Small pensions & SS cover essentials

|

|

|

|

|

12-06-2014, 06:13 AM

|

#34

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2011

Location: The Bay Area

Posts: 2,736

|

Quote:

Originally Posted by RetireBy90

2 points,:

1) I likewise am using 4% only as a check to verify we have sufficient that 4% will fill the gap between other income and spending. Once we start SS (66 and 70) I don't plan to take any from IRA to cover expenses. Perhaps some to cover other expenses like travel or a new liver

2) Completely different tac here, I wonder if anyone has done any research like the author, with a model of say 4% but if market goes down, draw goes down by say 1/2 of the market drop. I expect that if I could expect $1,000 every month, say from SS then for some reason that drops to $800 this year, my spending would also drop. I would think this is more realistic than to assume spending will never change from the time you FIRE. As noted in other replies, some plan to increase and decrease as needs and income change, so shouldn't your projection of needed draw? |

The Guyton-Klinger WD method does something similar (10% WD reduction for a 20% PF reduction), as do some other VWD methods (like Clyatt).

You can find threads on them here and at BH.

__________________

You may be whatever you resolve to be.

100% x 10% > 10% x 100%

Small pensions & SS cover essentials

|

|

|

|

|

12-06-2014, 10:54 AM

|

#35

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2009

Location: Cville

Posts: 1,604

|

Quote:

Originally Posted by Huston55

The Guyton-Klinger WD method does something similar (10% WD reduction for a 20% PF reduction), as do some other VWD methods (like Clyatt).

You can find threads on them here and at BH.

|

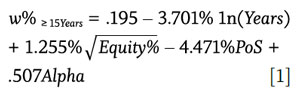

checked onepfa.org, seems the link has been moved by a rework of the site

Here is what I get for a dynamic withdrawal rate:

Mabye I need to stick to the 4% rule

|

|

|

|

|

12-06-2014, 11:35 AM

|

#36

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Apr 2004

Location: South Texas~29N/98W Just West of Woman Hollering Creek

Posts: 6,674

|

The "4% rule" is not a rule. It should be referred to as the 4% guide, just as the "age in bonds" is really a guide , not a rule.

But, of course, most of us already are aware of this.

__________________

Part-Owner of Texas

Outside of a dog, a book is man's best friend. Inside of a dog, it's too dark to read. Groucho Marx

In dire need of: faster horses, younger woman, older whiskey, more money.

|

|

|

|

|

12-06-2014, 11:42 AM

|

#37

|

|

Thinks s/he gets paid by the post

Join Date: Nov 2009

Location: SF East Bay

Posts: 4,342

|

Quote:

Originally Posted by Fermion

We are going to go with 3.5% to 4% (variable) at age 46 and if it fails....well, there is always money in the banana stand.

I am actually *ok* with it failing if we both get a good 20 years or so of retirement. No kids or anyone to worry about so we can always Thelma and Louise it.

Life has so many other unknowns (accidents, murder, cancer) that it seems a bit silly to worry a great deal about failure rates past 85% success.

|

20 years would take you to age 66. What would you do if your portfolio failed at age 66?

__________________

Contentedly ER, with 3 furry friends (now, sadly, 1).

Planning my escape to the wide open spaces in my campervan (with my remaining kitty, of course!)

On a mission to become the world's second most boring man.

|

|

|

|

12-06-2014, 12:10 PM

|

#38

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2003

Location: Kansas City

Posts: 7,968

|

Quote:

Originally Posted by BBQ-Nut

Well, don't be surprised that you will be *required* to take distributions from your IRA (assuming it is a tIRA and not a ROTH) at age 70.

In our scenario, even when doing 'top off' Roth conversions up to 70, we still get whammed by RMD, I just hope the DW and I are still up and about to take whirl wind world cruises and skydiving lessons with all the 'extra' money cuz of RMDs at 70! |

No surprise here - after 21 years of ER at age 71 me and the IRS are just the best of new found pals.

Now - I suspect in my being a 'cheap SOB' in early years of ER anticipating 'the shoe to drop any time' and wanting to be ready 'just in case' I was not alone. It might be like the OMY syndrome and very common.

Hindsight says I kinda enjoyed getting down with my bad frugal and varying withdrawals. Knock on wood - health has held up so I have no regrets on not spending earlier on hiking, skiing, travel, etc., etc.

heh heh heh - so all in all 2-6% plus variable withdrawal range and some Mr Market dipsy doodles 1993 -2014 I'm happy and my new found pals at the IRS are ecstatic.

|

|

|

|

|

12-06-2014, 01:28 PM

|

#39

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Oct 2006

Posts: 7,733

|

Quote:

Originally Posted by explanade

|

I must compliment Vanguard on presenting a good balanced article on the limitations and caveats on the 4% rule... I especially like this comment "In reality, very few retirees actually stick with such a strict policy".

I have yet to meet an actual retiree IRL or a forum who faithful follows the 4%, and I think that is a good thing.

|

|

|

|

|

12-06-2014, 02:00 PM

|

#40

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2007

Posts: 1,085

|

Quote:

Originally Posted by audreyh1

I use a % remaining portfolio withdrawal method. If my portfolio doesn't keep up with inflation, neither does my income.

If it runs ahead of inflation - PARTAY!

|

I'm curious what you do if your portfolio goes down by 10% in a year. Do you reduce spending by 10% the next year?

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode