Does not say "gone traveling" under his name.

That's funny. It did the other day.

The inner workings of the forum are mysterious.

Does not say "gone traveling" under his name.

Everyone here is wrong, the correct answer is 2.73489% Anything else will just fail utterly.

I miss him. No idea what got him thrown out of here, but his enthusiasm was delightful.

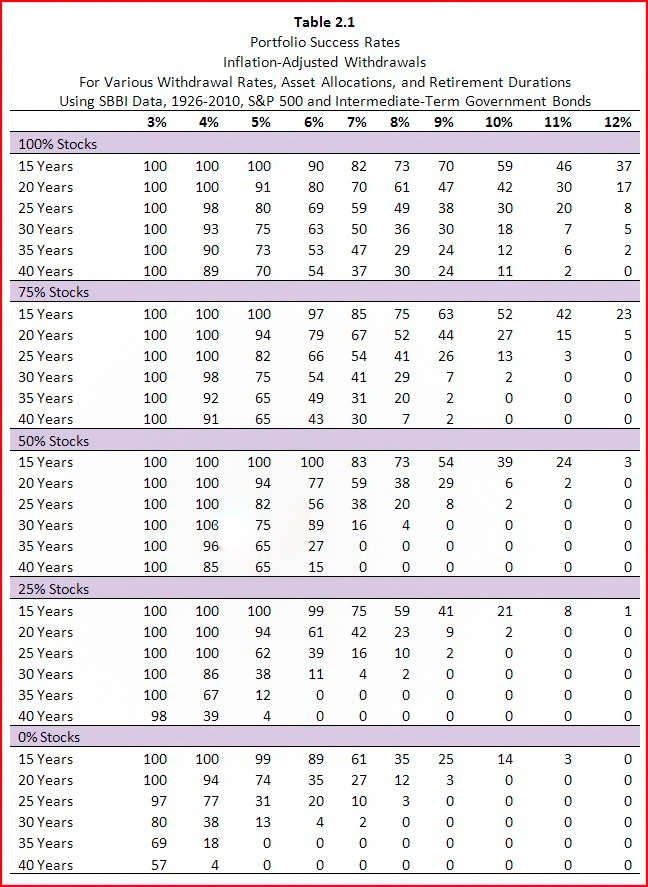

Back on topic, I've always read that 2% is the safe perpetual WR.

I've been averaging about 1.6 in the first three years. On pace for roughly the same this year. Pulled the plug two month shy of my 47th birthday. Will be celebrating 4 years of ER next month.[emoji106]I think the withdrawal rate is affected by the length of retirement. I retired at 46 and withdraw approx 2% per year.

What do you consider a safe withdraw rate without the possibility of running out of money? Assuming a 60/40 AA in a Vanguard 4 fund portfolio and not taking in consideration any other factors? 2.5%, 3%?

Thanks for the comments!

For perpetual, I would think you would have to consider the portfolio amount each year. Take out 2 or 3% of the total value each year. If your portfolio tanked, be prepared to cut back your spending. If it went way up, then you could take out more. You would have to be flexible.

... At what point are the odds of running out of life much higher than running out of money?...

Monetary risk, I can handle by cutting back, and live on just SS if need to. Worst case, I can always load all I can into my 25' motorhome and head off into the woods.

")

Everyone here is wrong, the correct answer is 2.73489% Anything else will just fail utterly.

As easy as pi.Actually, I thought the correct answer was 3.14159. It also helps figuring out things pertaining to circles.

It is an amazing number.

One can even run out of money with a negative withdrawal rate in some crazy scenarios with a very low likelihood. I think we're better off rephrasing the question:

At what point are the odds of running out of life much higher than running out of money?

Maybe I can help. By coincidence, I'm running an experiment right now to see if my withdrawal rate is the best for me. When the experiment is concluded I'll leave instructions to post the details.

... For $200 a month you only need a portfolio of $60,000 but you could get by on a lot less than that if you did $2000 worth of checking account churning.

Maybe I should keep $60,000 in a 1 year CD then I can always run Firecalc with 100% success.

If a guy lives on $200/month by being a bushman, will he have access to the Internet to post about his experience? Can one get a cellphone dataplan with that budget?