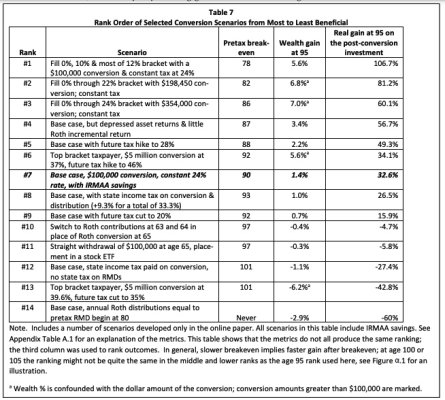

An interesting approach but I'm not too keen on wading through 40 pages of drivel, but it did spark an interesting different take at evaluating Roth conversions for me.

The table below is looking at solely my 2021 Roth conversion in isolation. If I do an $80k conversion in 2021, I'll pay $9,328 in tax (vs $0 if my conversion is zero). To keep things simple, I'll assume 0% growth. Given the RMD tables, I'll start saving taxes beginning at age 72 because my RMDs will be lower because my tax-deferred accounts will be $80,000 lower... and based on the RMD tables I can project how long it will be for my lower RMDs to equal the $80,000 Roth conversion.

I'm very sure that we'll be in the 22% tax bracket when RMDs begin so I calculate the tax benefit as 22% of the lower RMD. The $8,272 of tax savings is the $17,600 tax that I'll surely pay if I don't Roth convert ($80k * 22%) less the $9,328 that I know that I'm paying in 2021. So the Tax column are the differential cash flows from doing the Roth conversion and the IRR of those differential cash flows is 6.81%.

Works for me. YMMV. Part of the reason that it works well for me is that we are trading off paying 11.7% now (a blend of 0%, 10% and 12%) to avoid paying 22% later. So if the 2021 RMD is beneficial, then presumably each year that I can convert at less than 22% is beneficial... I guess I could do a cascade of annual Roth conversions but I'm convinced enough that they are beneficial to me that I'm not going to bother.

And this analysis doesn't even consider things like the likelihood that future tax rates will be higher (25% or more vs 22% based on today's tax brackets), the potential jump in tax rates if one of us dies prematurely, etc. ... so if anything this analysis is probably conservative.

If one is trading 22% for 24% then it probably wouldn't be near as attactive.... if I take the same scenario but assume paying 22% now to avoid paying 24% later then the IRR is only .84%

| Year | Age | RMD factor | 2021 RMD | Tax | Balance |

| | | | | |

| 2021 | 66 | | 80,000 | -9,328 | -9,328 |

| 2022 | 67 | | | | -9,328 |

| 2023 | 68 | | | | -9,328 |

| 2024 | 69 | | | | -9,328 |

| 2025 | 70 | | | | -9,328 |

| 2026 | 71 | | | | -9,328 |

| 2027 | 72 | 25.6 | -3,125 | 688 | -8,641 |

| 2028 | 73 | 24.7 | -3,239 | 713 | -7,928 |

| 2029 | 74 | 23.8 | -3,361 | 739 | -7,188 |

| 2030 | 75 | 22.9 | -3,493 | 769 | -6,420 |

| 2031 | 76 | 22.0 | -3,636 | 800 | -5,620 |

| 2032 | 77 | 21.2 | -3,774 | 830 | -4,790 |

| 2033 | 78 | 20.3 | -3,941 | 867 | -3,923 |

| 2034 | 79 | 19.5 | -4,103 | 903 | -3,020 |

| 2035 | 80 | 18.7 | -4,278 | 941 | -2,079 |

| 2036 | 81 | 17.9 | -4,469 | 983 | -1,096 |

| 2037 | 82 | 17.1 | -4,678 | 1,029 | -66 |

| 2038 | 83 | 16.3 | -4,908 | 1,080 | 1,013 |

| 2039 | 84 | 15.5 | -5,161 | 1,135 | 2,149 |

| 2040 | 85 | 14.8 | -5,405 | 1,189 | 3,338 |

| 2041 | 86 | 14.1 | -5,674 | 1,248 | 4,586 |

| 2042 | 87 | 13.4 | -5,970 | 1,313 | 5,900 |

| 2043 | 88 | 12.7 | -6,299 | 1,386 | 7,285 |

| 2044 | 89 | 12.0 | -4,484 | 987 | 8,272 |

| | | | | |

| Totals | | | 0 | 8,272 | |

| | | | | |

| IRR | | | | 6.81% | |

| | | | | |