I'm 66 , she is 62.

Say we have $2M in the stock market, allocated as below.

$1.2M tIRA

$240k Roth

$600k Taxable

We are spending about $45k per year.

When I'm 70 we will get $45k of SS

My RMDs start at 72 on about $600k. (grown to about $1M in 6 years)

Hers start 4 years later on the other $600k. ($1M in 6 years)

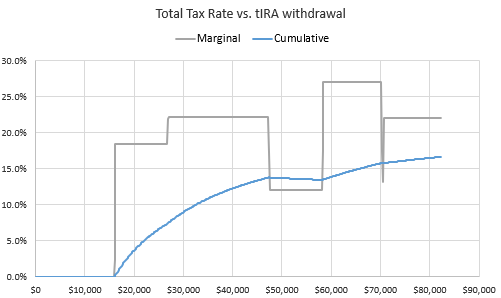

The first year I Roth converted $75k and stayed in the 12% tax bracket.

But the tIRA fund grew faster than the conversion.

I'm questioning whether I should max out the 22% bracket.

I can see $88k of forced income when I get my first RMD.

Running $12k dividends, $45k SS, and $32,850 RMDs through Dinkytown tax calculator, https://www.dinkytown.net/java/1040-tax-calculator.html

It leaves me well within the 12% tax bracket, I could add another $35k before going into the 22% bracket. So, 4 years later adding my wife's RMDs, we will just hit the 22% tax bracket.

After doing the above Dinkytown calculations, I now think max to the top of the 12% bracket. (I didn't know I waffled so easily)

Anyone have feedback, other than "ya, but tax rates will go up". Then I have to wonder, will the income level rise with the tax bracket percentage increase. ie I doubt the 12% bracket will increase as high as 22% and the income level will probably be higher. Suggesting I should not go into the 22% bracket with Roth Conversions.

Say we have $2M in the stock market, allocated as below.

$1.2M tIRA

$240k Roth

$600k Taxable

We are spending about $45k per year.

When I'm 70 we will get $45k of SS

My RMDs start at 72 on about $600k. (grown to about $1M in 6 years)

Hers start 4 years later on the other $600k. ($1M in 6 years)

The first year I Roth converted $75k and stayed in the 12% tax bracket.

But the tIRA fund grew faster than the conversion.

I'm questioning whether I should max out the 22% bracket.

I can see $88k of forced income when I get my first RMD.

Running $12k dividends, $45k SS, and $32,850 RMDs through Dinkytown tax calculator, https://www.dinkytown.net/java/1040-tax-calculator.html

It leaves me well within the 12% tax bracket, I could add another $35k before going into the 22% bracket. So, 4 years later adding my wife's RMDs, we will just hit the 22% tax bracket.

After doing the above Dinkytown calculations, I now think max to the top of the 12% bracket. (I didn't know I waffled so easily)

Anyone have feedback, other than "ya, but tax rates will go up". Then I have to wonder, will the income level rise with the tax bracket percentage increase. ie I doubt the 12% bracket will increase as high as 22% and the income level will probably be higher. Suggesting I should not go into the 22% bracket with Roth Conversions.

Last edited: