seraphim

Thinks s/he gets paid by the post

- Joined

- Mar 6, 2012

- Messages

- 1,555

Nm - figure out what he meant ....

My equation = [(end value - 1/2 * additions) / (begin value + 1/2 * additions)] - 1 * 100

-CC

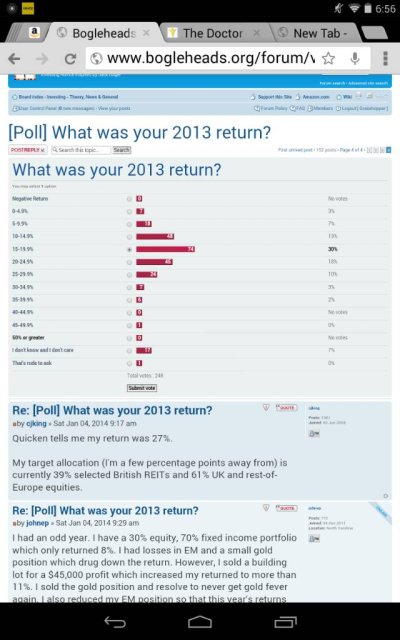

According to the Morningstar portfolio manager, our personal returns on a 60/40 portfolio was 24+ percent. That would be a little low, as it did not consider returns from some of the FI holdings not in bonds, but that's close enough for government work...

16.76% with a 55/45 allocation. I'm very content with it.

Nobody includes additions in that way to calculate their annual return, except for the Beardstown Ladies. I believe the post you referenced included them on both top and bottom as a way of averaging out the effect of investments that were only active part of the year.For the record, my % in the post above does not include additions.

With additions, I would say about 15-20% increase.

....My equation = [(end value - 1/2 * additions) / (begin value + 1/2 * additions)] - 1 * 100

While your equation works, a more typical construct would be return/investment or:

(ending value - beginning value - additions)/(beginning value + 50% * additions)

Age 55 now but won't be withdrawing until 60 or later.

Age 55 now but won't be withdrawing until 60 or later.You must've been really heavy in Selected Value since that's the only one that did better than 40% (and not by much), and the Life Strategy one was in the teens. Are you counting contributions as investment return?40% in the Vanguard 401K.

I'm 90% stocks in S&P 500, Life Strategy Moderate and Growth, PRIMECAP, Windsor II, Selected Value. Just starting contributing more to International Value and Growth funds.

I am astounded! Also worried I should go more conservative now. But what

I don't consider my house an investment, nor my collectibles since they are just small hobbies. The question wasn't the return on all assets. Unrealized gains is no issue with stocks and mutual funds since they had a closing market value on 12/31. 99+% of my investments are with Vanguard so I just used what they tell me my rate was and I assume they are properly accounting for withdrawals. VG gave me one decimal point so that's what I reported.Beats me how some of you can figure this number to one, much less two decimals with all the fudgeries in real estate valuations, collectibles, unrealized gains, etc.