FIREd_2015

Recycles dryer sheets

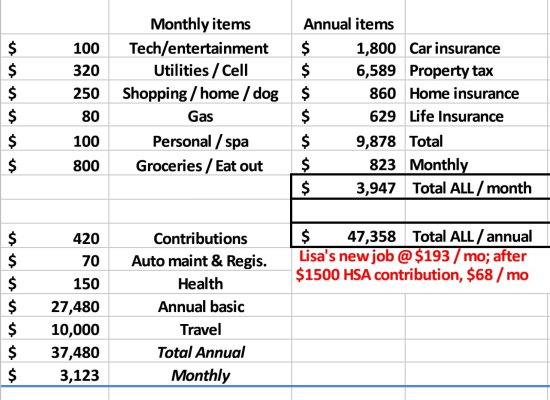

Average total expenses over the past 5 yrs $4500-5000/month

Mortgage: $0

HOA: $200 (Planned Unit Development)

Property Tax: $580

Home Owner Insurance: $109

Electric & Gas: $75

Car Insurance:$90

Internet: $0 (use mobile as hotspot)

Water/sewer/trash: $145

Mobile: $41

Obamacare: $1145 (before subsidy - reconciled when I file taxes)

Rental Property: $990

Total: $3375

Mortgage: $0

HOA: $200 (Planned Unit Development)

Property Tax: $580

Home Owner Insurance: $109

Electric & Gas: $75

Car Insurance:$90

Internet: $0 (use mobile as hotspot)

Water/sewer/trash: $145

Mobile: $41

Obamacare: $1145 (before subsidy - reconciled when I file taxes)

Rental Property: $990

Total: $3375

Last edited:

")