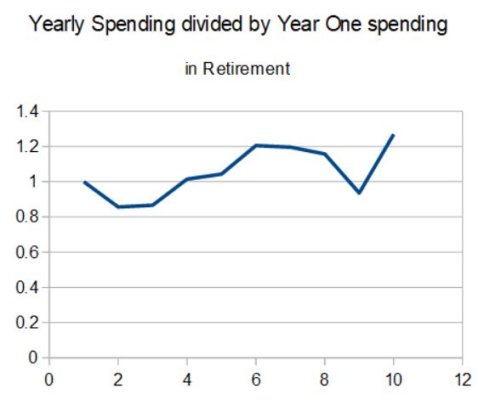

In our first year of semi-retirement (DH is still w*rking pt) and I’m finding we are spending a ton on ‘one time’ stuff for the house and future lifestyle. Some of it was planned for and money was allocated, and some is covid related, but I’m also finding with all of this extra free time I’m noticing more things that need fixed on the house, more little things that would streamline our life and make things easier, more hobby related stuff, etc...

Did anyone else go through a ‘first year’ money spend? Did it end

We’re still within budget due to the planned for expenses and lower covid expenses, and I’ve found lots of ways to cut our spend that I never had time to focus on before, but I’m surprised how many extras we’re wanting!

Did anyone else go through a ‘first year’ money spend? Did it end

We’re still within budget due to the planned for expenses and lower covid expenses, and I’ve found lots of ways to cut our spend that I never had time to focus on before, but I’m surprised how many extras we’re wanting!

So we tacked up a large towel over the bathroom window the first day or two we were there. Fortunately the bedroom windows faced the woods and I figured the deer and squirrels wouldn't care what we looked like naked. DW wasn't so sure.

So we tacked up a large towel over the bathroom window the first day or two we were there. Fortunately the bedroom windows faced the woods and I figured the deer and squirrels wouldn't care what we looked like naked. DW wasn't so sure.