Welcome, Errollyn! It sounds like you have a good grip on where you are and where you want to be, that's a great start!

I suggest posting in the "Hi, I am" forum, too, when you get a chance, to introduce yourself to the rest of the board, not just us hoping to be in the class of 2024!

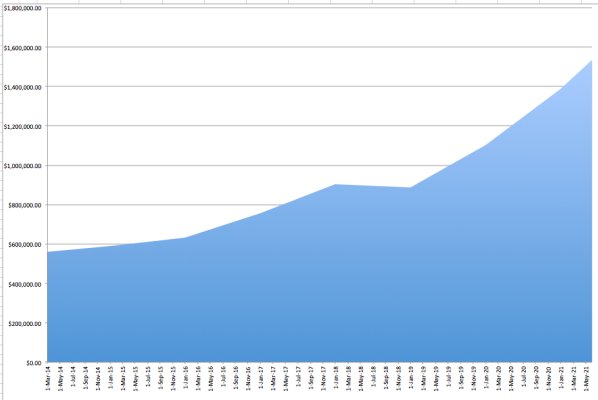

If you're planning for your retirement funds to last you 40 or more years instead of the typical 20, you should aim for either a 3-3.5% withdrawal rate (WR), or make sure you have a lot of fat in your budget that you can cut if there is a recession/depression. However, if your pension pans out you're probably fine, guaranteed income is a wonderful safety net! But I'd plan as if you won't have it for now, until you know that you do. That way you're fine either way.

Great point about the 4% perhaps being too high to safely fund retirement. It's definitely something I've considered, and a lower rate may be in order.

I didn't want to get too into the weeds for fear of boring you guys, but I do have a pension coming to me regardless of whether I take an early retirement offer (unless our society falls apart, that is). It's just a matter of whether I can start drawing it immediately, or if I have to wait until I'm in my late 50s. I also haven't factored SS into my figures, but presumably that would be an additional income available in my early 60s. Given these two factors, my investments really only have to bridge the gap between age 49 through age 60 by themselves--after that, SS and the pension should kick in. That being said, I try not to consider those as guarantees, and want my personal investments to be enough to fund our retirement just in case they don't materialize for some reason.

I also think my expenses in 2020 might've been higher than what I'd spend in retirement. But again, to play it safe I'm considering it a "normal" year.

And, I wish you all a very Happy New Year and Cheers to (fingers crossed) life getting back to normal

And, I wish you all a very Happy New Year and Cheers to (fingers crossed) life getting back to normal

")