Over three decades, health care costs in the US rose from 7% of GDP to 17%. A clearer trend could not exist. The rate of increase appears to have slowed, probably because it reached the level of general unaffordability.

Health care reform is not about cost and is best described by the concept of "Triple Aim", which is The PPACA is one step in that direction, not yet fully implemented, and probably too early to measure the impact.

The upward trend in US HC costs has not been a straight line, but has had periods of slowing followed by reinflation (e.g. 61-65, 72-73, 96-98).

IMHO- It's too early to call recent lull in HC inflation a change in the overall upward trend, although I sure hope it is.

FWIW- US gov't's historical HC inflation data is available here (searchable by various annual periods)-

Bureau of Labor Statistics Data

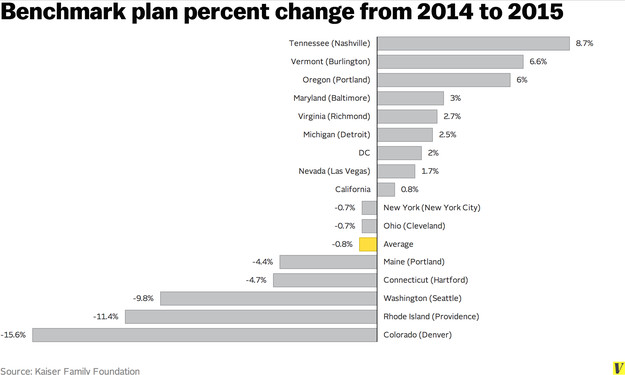

I agree that cost is not the only aim of HC reform, but it is a major one. It was touted as such from the beginnings of the ACA debate. Ultimately cost containment is critical to the sustainability of any HC system (private insurance, single-payer, or socialized). It is axiomatic that if costs rise beyond point of "unaffordability", population health & experience will be adversely affected by the decline in real access to HC services. Only time will tell if ACA was indeed a meaningful step in cost containment. I personally doubt it. Most major CC features of ACA have already been implemented. I discount FY 2014 data as a blip as all parties absorbed the complex roll-out of the new system. But IMHO FY 2015 should have brought a meaningful decline in HI premiums across the US. The prelim data suggests this is not the case. I hope history proves me wrong, but I feel unsubsidized FIRE's should be prepared for a resumption of significant rate hikes in 2016 and beyond.