GravitySucks

Thinks s/he gets paid by the post

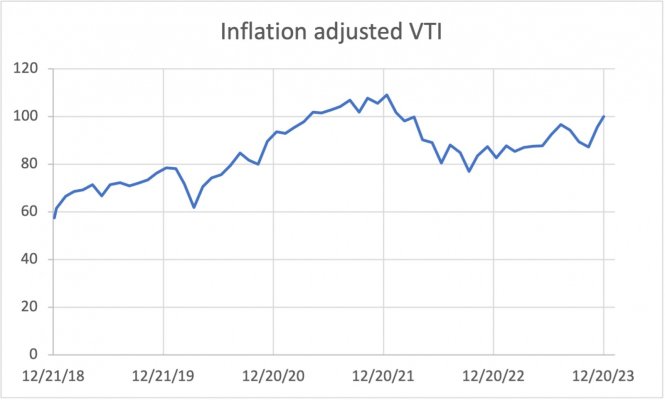

Getting that feeling in my gut again. The S&P just feels to frothy so I’m “Aggressively Rebalancing” and pulling all 2024 spending from equities this week. No math. No expert recommendations. No Technicals. Just gut feeling.

Not really a large enough amount to make any difference really. 62/38 to 58/42 AA

It’s worked out well a few times now.

https://www.early-retirement.org/forums/f28/dirty-market-timer-100610.html

Hope the Santa Rally continues. Might pull 2025 spending too.

Not really a large enough amount to make any difference really. 62/38 to 58/42 AA

It’s worked out well a few times now.

https://www.early-retirement.org/forums/f28/dirty-market-timer-100610.html

Hope the Santa Rally continues. Might pull 2025 spending too.