|

|

02-13-2020, 09:10 AM

02-13-2020, 09:10 AM

|

#41

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

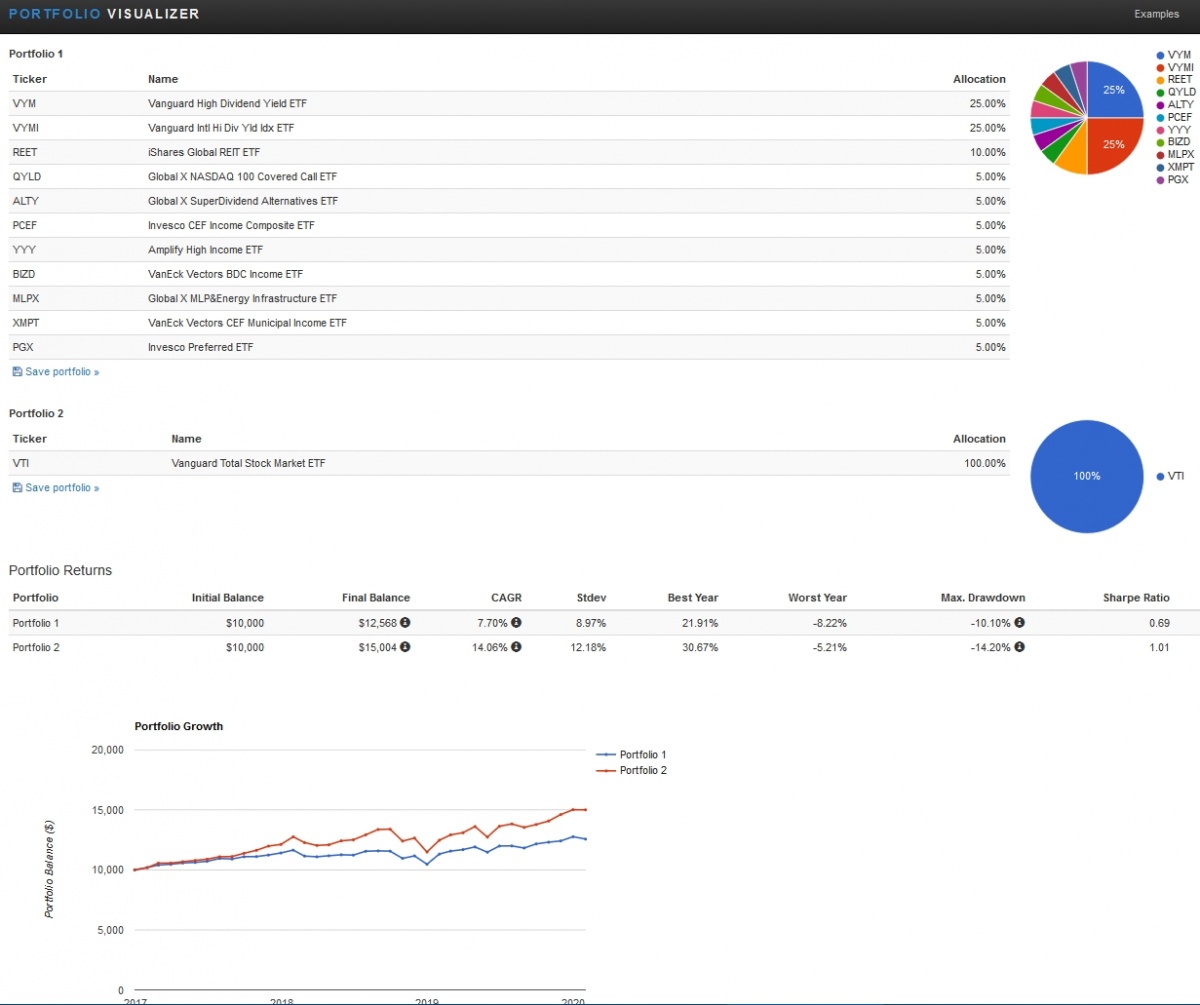

@MarieL, as you obviously know there is an infinity of possible portfolios. The one that @ESRWannabe has posted is simply one of them. There is a nice tool at https://www.portfoliovisualizer.com that allows fairly easy comparison of portfolios. Here is a run* that compares the @ESRWannabe's portfolio to a portfolio that is 100% VTI:

Basically, @ESRWannabe's portfolio reduces relative volatility but provides a significantly lower rate of return (CAGR). There is nothing wrong with this; it is simply a choice. I would submit, though, that it is not a good choice for someone looking for aggressive growth and, in the accumulation phase, relatively unconcerned about volatility.

Quote: Quote:

Originally Posted by ESRwannabe

...There will eventually come a time when investing for capital gains doesn't work for decades (as it had in the past). Once this happens all this total return stuff will be tossed out the window again and people will go back to investing for dividends.

|

This implies that dividend investing and total return investing are mutually exclusive things. They are not. Total return is simply capital gains plus dividends. So if capital gains go away (which I doubt), then dividends will dominate total return calculations. IOW, whether capital gains exist or not, total return is still the sensible measure of an investment.

__________________________________________

* one problem with Portfolio Visualizer is that it can only go back as far as the shortest asset history file. In this case, PFFA had a very short history so I have substituted a similar fund, PGX, in order to get a three-year comparison. At that point, VYMI's history ends. I did not want to substitute for that one because it is 25% of the portfolio. Ideally this type of comparison will cover five or more years. And, of course, it guarantees nothing about the future performance of any portfolio.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

02-13-2020, 11:21 AM

|

#42

|

|

Dryer sheet aficionado

Join Date: Feb 2020

Posts: 28

|

Quote:

Originally Posted by OldShooter

@MarieL, as you obviously know there is an infinity of possible portfolios. The one that @ESRWannabe has posted is simply one of them. There is a nice tool at https://www.portfoliovisualizer.com that allows fairly easy comparison of portfolios. Here is a run* that compares the @ESRWannabe's portfolio to a portfolio that is 100% VTI:

Basically, @ESRWannabe's portfolio reduces relative volatility but provides a significantly lower rate of return (CAGR). There is nothing wrong with this; it is simply a choice. I would submit, though, that it is not a good choice for someone looking for aggressive growth and, in the accumulation phase, relatively unconcerned about volatility.

This implies that dividend investing and total return investing are mutually exclusive things. They are not. Total return is simply capital gains plus dividends. So if capital gains go away (which I doubt), then dividends will dominate total return calculations. IOW, whether capital gains exist or not, total return is still the sensible measure of an investment.

__________________________________________

* one problem with Portfolio Visualizer is that it can only go back as far as the shortest asset history file. In this case, PFFA had a very short history so I have substituted a similar fund, PGX, in order to get a three-year comparison. At that point, VYMI's history ends. I did not want to substitute for that one because it is 25% of the portfolio. Ideally this type of comparison will cover five or more years. And, of course, it guarantees nothing about the future performance of any portfolio. |

Thank you so much for sharing that site! This is pretty awesome! I was playing around with some numbers and allocations, comparing some portfolios.

Portfolio 1 is loosely based off the Core 4 80/20 (with Tesla added and bonds taken out)

Portfolio 2 is my own I put together.

It looks like Portfolio 2 would give the higher return in a faster amount of time if I contributed $100 a month (which I currently do). Or am I reading this incorrectly?

Also I did click the box that said 'inflation adjusted'

What do you think? Would Portfolio 2 be good for me?

|

|

|

|

|

02-13-2020, 11:42 AM

|

#43

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Dec 2008

Location: On a hill in the Pine Barrens

Posts: 9,724

|

VTI

VNQ

TSLA

and call it a day.

|

|

|

|

02-13-2020, 11:47 AM

|

#44

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by MarieL

... What do you think? ...

|

For all intents and purposes those two are identical.

Also be careful with concluding that one or the other of similar portfolios "would be" anything. All you are seeing is what has happened in the past. The future is unknown. Backtesting is great fun and somewhat useful for comparisons but that is the end of the story. The worst form of backtesting is when someone goes back and cherry picks a bunch of winners, then believes that this is the genius portfolio for the future.

Also, I would not include Tesla in any backtesting portfolio because of its anomolous past price behavior. The only thing to know for sure is that Tesla will, in the future, not come anywhere near its past behavior. You have it at tiny percentages so it probably is not distorting your results much but just as a matter of principle I would not include it.

Sorry there is no magic to investing and there are no secret sauces to find.

|

|

|

|

|

02-13-2020, 12:08 PM

|

#45

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2013

Posts: 2,523

|

Quote:

Originally Posted by ESRwannabe

Here is a portfolio for you that will cover a lot of asset classes, be globally diversified, generate a high amount of current income, and provide income growth over time.

25% into etf VYM (Vanguard High Div Yield US)

25% into etf VYMI (Vanguard High Div Yield Foreign)

10% into etf REET (iShares Global REITs)

5% into etf QYLD (GlobalX Nasdaq Covered Calls)

5% into etf ALTY (GlobalX Alternative Assets)

5% into etf PCEF (Invesco CEF Income Composite)

5% into etf YYY (YieldShares CEF High Income)

5% into etf BIZD (VanEck BDC Income)

5% into etf MLPX (GlobalX MLP & Energy Infrastructure)

5% into etf XMPT (VanEck Municipal Bond CEFs)

5% into etf PFFA (Virtus Infracap US Preferred Stock)

|

I don't know why Marie would want a portfolio with high income. At such a young age, I would think it would be the exact opposite. She would want more growth and dividends to be taxed at lower capital gains rates. Income portfolios are for those who need the income to live off of. She is in the accumulation phase and is looking for growth. I also think this is way too many holdings. Two or three at most of broad based index funds is all you need and if she sticks to that logic, she would hopefully not need to deal with fractional shares.

Marie; Take out a copy of "The Four Pillars of Investing" by Bernstein, from the local library and read it. I will give you a broad brush without too much minutia.

__________________

"Luck favors the prepared mind"

Pasteur

|

|

|

|

|

02-13-2020, 12:42 PM

|

#46

|

|

Dryer sheet aficionado

Join Date: Feb 2020

Posts: 28

|

Quote:

Originally Posted by Golden sunsets

I don't know why Marie would want a portfolio with high income. At such a young age, I would think it would be the exact opposite. She would want more growth and dividends to be taxed at lower capital gains rates. Income portfolios are for those who need the income to live off of. She is in the accumulation phase and is looking for growth. I also think this is way too many holdings. Two or three at most of broad based index funds is all you need and if she sticks to that logic, she would hopefully not need to deal with fractional shares.

Marie; Take out a copy of "The Four Pillars of Investing" by Bernstein, from the local library and read it. I will give you a broad brush without too much minutia.

|

Thank you for the book recommendation! I will look for it.

And yes, I am in my late 30s trying to build wealth fast and responsibly so I can reach FIRE before 50.

|

|

|

|

|

02-13-2020, 12:52 PM

|

#47

|

|

Recycles dryer sheets

Join Date: Oct 2016

Posts: 432

|

I wish this Youtube video existed 30 years ago when I started investing, I made a lot of mistakes by picking individual stocks, trying to pick hot mutual fund managers and so on.

Jcollins did a talk at Google where he talks about the simple path to wealth, pick 3 ETFs or index funds, put as much as you can each month into it on autopilot, check back again in 20 years when you are ready to retire.

JL Collins: "The Simple Path to Wealth" | Talks at Google

|

|

|

|

|

02-13-2020, 12:58 PM

|

#48

|

|

Dryer sheet aficionado

Join Date: Feb 2020

Posts: 28

|

Quote:

Originally Posted by OldShooter

For all intents and purposes those two are identical.

Also be careful with concluding that one or the other of similar portfolios "would be" anything. All you are seeing is what has happened in the past. The future is unknown. Backtesting is great fun and somewhat useful for comparisons but that is the end of the story. The worst form of backtesting is when someone goes back and cherry picks a bunch of winners, then believes that this is the genius portfolio for the future.

Also, I would not include Tesla in any backtesting portfolio because of its anomolous past price behavior. The only thing to know for sure is that Tesla will, in the future, not come anywhere near its past behavior. You have it at tiny percentages so it probably is not distorting your results much but just as a matter of principle I would not include it.

Sorry there is no magic to investing and there are no secret sauces to find.

|

Thanks for the tips! I was looking at patterns and just making my own deductions, but I understand what you mean. I am not looking for the magic pill. I just want to build a portfolio that will help me reach FIRE before 50.

|

|

|

|

|

02-13-2020, 01:12 PM

|

#49

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by MarieL

... I just want to build a portfolio that will help me reach FIRE before 50.

|

Pick two or three broad equity funds with total 30-50% international exposure and take a look at the portfolio every year or two. If you hear that the market has taken a dive, stop looking for a couple of years.

One of the things that I learned in my first 30 years of investing is that the more I played with my food, the less food I had.

|

|

|

|

|

02-13-2020, 01:23 PM

|

#50

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,376

|

Quote:

Originally Posted by ESRwannabe

Here is a portfolio for you that will cover a lot of asset classes, be globally diversified, generate a high amount of current income, and provide income growth over time.

25% into etf VYM (Vanguard High Div Yield US)

25% into etf VYMI (Vanguard High Div Yield Foreign)

10% into etf REET (iShares Global REITs)

5% into etf QYLD (GlobalX Nasdaq Covered Calls)

5% into etf ALTY (GlobalX Alternative Assets)

5% into etf PCEF (Invesco CEF Income Composite)

5% into etf YYY (YieldShares CEF High Income)

5% into etf BIZD (VanEck BDC Income)

5% into etf MLPX (GlobalX MLP & Energy Infrastructure)

5% into etf XMPT (VanEck Municipal Bond CEFs)

5% into etf PFFA (Virtus Infracap US Preferred Stock)

|

Too many tickers... too much complexity! Read the OP.... we're talking about less than $1k right now..... why would you recommend 11 tickers for a portfolio less than $10k? Actually, even if it was $1m you don't need that many tickers!

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

02-13-2020, 02:20 PM

|

#51

|

|

Dryer sheet aficionado

Join Date: Feb 2020

Posts: 28

|

Quote:

Originally Posted by Go-NoGo

I wish this Youtube video existed 30 years ago when I started investing, I made a lot of mistakes by picking individual stocks, trying to pick hot mutual fund managers and so on.

Jcollins did a talk at Google where he talks about the simple path to wealth, pick 3 ETFs or index funds, put as much as you can each month into it on autopilot, check back again in 20 years when you are ready to retire.

JL Collins: "The Simple Path to Wealth" | Talks at Google

|

What an awesome video! Watched the whole thing and I am reading articles from his blog.

|

|

|

|

|

02-18-2020, 07:28 PM

|

#52

|

|

Recycles dryer sheets

Join Date: Nov 2017

Posts: 343

|

K.I.S.S.

|

|

|

|

|

02-19-2020, 01:15 AM

|

#53

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2007

Posts: 1,860

|

Quote:

Originally Posted by Golden sunsets

Too many holdings. If it were me I would buy one portion of a US total stock market fund, one portion of an international stock market fund and the final portion of a total bond fund. I would probably do 65/20/15.

|

+1

You are probably paying a lot of hidden fees for that many holdings.

__________________

"Live every day as if it were your last, and one day you'll be right" - unknown

|

|

|

|

|

02-19-2020, 01:19 AM

|

#54

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2007

Posts: 1,860

|

Quote:

Originally Posted by MarieL

Thank you for the book recommendation! I will look for it.

And yes, I am in my late 30s trying to build wealth fast and responsibly so I can reach FIRE before 50.

|

Dont know what your annual spending or lifestyle is, but seems like youre really going to need to save hard to FIRE in 12 years. Push hard if thats your goal!

__________________

"Live every day as if it were your last, and one day you'll be right" - unknown

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode